The EU can manage without Russian liquified natural gas

How can the European Union achieve its target of eliminating all Russian fossil-fuel imports by 2027?

Executive summary

The European Union has committed to eliminate all Russian fossil-fuel imports by 2027. Progress has been made, with sanctions on oil and coal already introduced. The glaring exception is natural gas, on which the EU has so far refrained from imposing limitations, owing to greater dependence on Russia. Nevertheless, pipeline gas imports have fallen by four-fifths following Russia’s weaponisation of gas supplies.

However, Russia’s exports of liquified natural gas (LNG) to the EU have increased since the invasion of Ukraine. The EU needs a coherent strategy for these LNG imports.

Our analysis shows that the EU can manage without Russian LNG. Anticipated impacts are not comparable to those felt in 2022 as Russian pipeline gas dried up. The regional impact would be most significant for the Iberian Peninsula, which has the highest share of Russian LNG in total gas supply. Meanwhile, the global LNG market is tight, and we anticipate that Russia would find new buyers for cargos that no longer enter Europe.

We discuss the options available to the EU. Wait-and-see implies delaying any action until 2027, while soft sanctions would discourage additional purchases but not break long-term contracts. We argue instead for an EU embargo on Russian LNG, to reduce exposure to an unreliable and adversarial entity, and to limit the extent to which EU consumers fund the Russian state. The embargo may be designed to allow purchases only if they are coordinated via the EU’s Energy Platform, with limited volumes and below market prices. This could be accompanied by the implementation of a price cap on Russian LNG cargos that use EU or G7 trans-shipment, insurance or shipping services.

1 Introduction

The European Union has a target of eliminating all Russian fossil-fuel imports by 2027. Swift progress has been made, aided by Russia’s own decision to decrease natural gas pipeline exports to the EU. However, the EU’s liquefied natural gas imports from Russia have remained remarkably stable. Discussions are ongoing about adding Russian LNG to the list of products banned from import to the EU (Table 1).

Throughout 2022, Russia cut natural gas pipeline exports to the EU steadily, but did not reduce exports of LNG 1 Liquefied natural gas is natural gas that has been cooled down to liquid form, for transport in dedicated ships. , which had been much smaller in volume. In the year after Russia’s invasion of Ukraine, LNG exports to the EU were valued at €12 billion. Unless there is decisive change from the current situation, the EU could pay up to another €9 billion to Russia in the second year of the war (Demertzis and McWilliams, 2023).

Table 1: EU imports of Russian energy (GWh)

|

|

Context |

March 2022 imports |

March 2023 imports |

|

Crude oil |

EU embargo from 5 December 2022 |

105,000 |

12,000 |

|

Diesel |

EU embargo from 5 February 2023 |

23,100 |

290 |

|

Pipeline natural gas |

Russia cut exports; certain EU countries refused to pay in rubles; Nord Stream I pipeline blown up |

113,000 |

24,000 |

|

LNG |

No action |

19,400 |

14,500 |

|

Coal |

EU embargo from 10 August 2022 |

31,000 |

0 |

Source: Bruegel based on Eurostat, Bruegel Natural Gas Import Tracker, Eurostat Comext.

Accordingly, in March 2023, the European Union said it had started to develop a mechanism to allow member states to block Russian LNG imports 2 Ewa Krukowska and John Ainger, ‘EU Aims to Give Members Option to Block Russian LNG Imports’, Bloomberg, 28 March 2023, https://www.bloomberg.com/news/articles/2023-03-28/eu-aims-to-give-memb…. . This would be done by granting permission to EU countries to block Russian companies from booking LNG import infrastructure 3 As part of the revision of the EU Gas Regulation, ongoing at time of writing; see https://www.europarl.europa.eu/legislative-train/theme-a-european-green…. . This is a similar approach to when Russian companies were prevented from booking gas-storage capacity in the EU that they were then intentionally leaving empty 4 See summary information about sanctions at https://eu-solidarity-ukraine.ec.europa.eu/eu-sanctions-against-russia-…. . At time of writing, this proposal is not finalised, and it is unclear how it would affect non-Russian companies that wish to book import capacity for the purpose of importing Russian-origin LNG 5 At national level, the Dutch and Spanish governments have announced plans to wind down contractual Russian LNG imports, and have asked importers not to sign additional contracts for Russian LNG. See Cagan Koc and Diederik Baazil, ‘Netherlands Plans to End Russian LNG Imports, Minister Says’, Bloomberg, 12 April 2023, https://www.bloomberg.com/news/articles/2023-04-12/netherlands-plans-to…, and Stephen Stapczynski, Thomas Gualtieri and Anna Shiryaevskaya, ‘Spain Urges LNG Importers to Diversify Away From Russian Supply’, Bloomberg, 24 March 2023, https://www.bloomberg.com/news/articles/2023-03-24/spain-urges-lng-impo…. .

In this context, we outline four different options available to the EU. In the first, ‘wait-and-see’, the EU would continue to import Russian LNG and would wait to introduce sanctions until the second half of this decade, when LNG markets are less tight. The second approach, ‘soft sanctions’, would entail a partial effort to reduce imports of Russian LNG without dramatically impacting long-term contracts that form the basis of much EU-Russia LNG trade. Under a full ‘EU embargo’ scenario, sanctions on Russian LNG would force companies to declare force majeure on long-term contracts and no Russian LNG would enter the EU.

A fourth approach, ‘EU embargo with EU Energy Platform offer’, would see the bloc tear up the existing trade structure and return to the table as one entity to negotiate. This could be done through the new EU Energy Platform for joint purchasing of gas 6 See https://energy.ec.europa.eu/topics/energy-security/eu-energy-platform_en. , which might make offers to purchase limited volumes of Russian LNG, which would be phased out over time, depending on the situation in Ukraine. This approach could be complemented by the introduction of a price cap on Russian LNG imports that rely on EU or G7 services, including trans-shipments, vessels and shipping insurance.

To assess the options, we begin by providing an overview of the growing role LNG (including from Russia) plays in Europe’s gas mix. We assess the impacts on the EU of an end to Russian LNG imports, by evaluating quantitatively the impact on gas balances and storage, to identify whether the EU would manage without Russian LNG. In investigating the impacts on Russia, we discuss the nature of LNG exports from Russia to the EU, which are characterised by long-term contracts and the multi-nationally owned Yamal liquefication plant. Finally, we discuss the impacts of the options available to the EU on global LNG markets and Russia.

2 The growing importance of LNG

Increased LNG imports, alongside domestic demand reduction, prevented the European Union from running out of natural gas during the peak of the energy crisis in 2022. Together, these measures enabled a remarkably smooth transition away from the EU’s historically largest supplier – Russia. Russian pipeline exports made up about 40 percent of the EU’s total gas supply prior to the invasion of Ukraine, but today account for less than 10 percent. In the year from 1 April 2022 to 31 March 2023, the EU imported 950 terawatt hours (TWh) less of Russian pipeline gas than in the previous 12-month period. The EU made up for the shortfall by boosting imports from other sources and reducing demand (Figure 1).

In 2022, the EU’s imports of LNG increased 66 percent year-on-year. The largest proportion of this growth came from the United States, while Russia is currently the second largest provider of LNG to the EU, though far behind the US. In the first quarter of 2023, Russian LNG exports to the EU were 51 TWh, accounting for 16 percent of LNG supply and 7 percent of total natural gas imports.

The largest share of Russian LNG is imported through Spanish ports, while Belgian, Dutch and French ports account for most of the remaining volumes. We consider the Iberian Peninsula separately from the rest of the EU for our subsequent analysis because of the region’s relatively high dependence on LNG and because of the limited connections between the Peninsula and the wider European gas market. In the first quarter of 2023, the Iberian Peninsula imported 17 TWh of Russian LNG, or one quarter of total LNG supply and 20 percent of total natural gas imports to Spain and Portugal. Figure 2 plots EU LNG imports by supplier. The left panel shows the EU without Spain and Portugal and the right panel shows the Iberian Peninsula separately.

The nature of LNG imports means they pass through ports before distribution throughout the wider European gas grid. A country’s LNG imports do not necessarily remain there but may transit on to neighbouring countries. Contractual information on these flows is not publicly available, but we have estimated the relative importance of Russian LNG by country. Figure 3 shows these results for winter 2022-2023. According to our accounting basis, Russian LNG made up 18 percent of Spanish gas supply, 15 percent of French supply and 10 percent of Belgian supply.

Figure 3: Estimated shares of total gas supply to Russian LNG, winter 2022-23

3 EU gas balances without Russian LNG

In the EU embargo scenario, all Russian LNG would stop flowing to the EU. This might also be the case in the EU Energy Platform offer scenario, and might happen irrespective of EU decisions if Russia chooses to block exports. We therefore assess the impact of an immediate halt to Russian LNG supplies by modelling the evolution of EU gas balances and storage, performing a separate analysis for the Iberian Peninsula and the rest of the EU (EU25). Scenarios begin with actual gas storage of 746 TWh in the EU25 and 36 TWh on the Iberian Peninsula as of 1 June 2023. We make assumptions about natural gas imports, with and without Russian LNG, based on the most recent flows (see Annex 2).

In our baseline scenario, demand reduction would continue to be 15 percent below the five-year average. This is in line with the March 2023 Council of the EU agreement to maintain a 15 percent demand reduction target until March 2024 7 See Council of the EU press release of 28 March 2023, https://www.consilium.europa.eu/en/press/press-releases/2023/03/28/memb…. , and recent observations of actual demand reductions (McWilliams and Zachmann, 2023). Figures 4 and 5 show our results.

Figure 4 shows that the EU25 will be well able to fill storage facilities over the summer months without any Russian LNG, with the only consequence being a slight postponement of the moment when storage reaches full capacity. While stored volumes will deplete at a marginally faster rate, the EU25 will also not face a substantial additional challenge to manage the winter of 2023-24.

It is notable that under both scenarios, storage would reach maximum capacity before winter months start to see draws on storage. The EU would be able to prepare better for winter 2023-24 if it had greater storage capacity. One area for exploration in this respect is the extent to which gas storage sites in western Ukraine could be used for storing excess gas that would benefit both the EU (largely eastern regions) and Ukraine.

For the Iberian Peninsula we assess three scenarios. Again, all scenarios assume that the 15 percent demand reduction target is met. In scenario A, all imports remain the same as they have in the past months (including Russian LNG), and the draining of gas storage facilities over the winter would be at typical levels, with the Peninsula comfortably managing. In scenario B, all Russian LNG flows would be halted and not replaced at all. In this scenario, storage facilities would run out by January.

We do not think scenario B is a serious possibility but include it for illustrative purposes only. In reality, Spain would replace lost Russian LNG cargos by purchasing on the global market. In scenario C, we show that this replacement rate would need to be 50 percent for the Peninsula to maintain reserves above 20 percent throughout winter, ie Spain should find alternative supply for one out of every two lost Russian cargos. We note also the possibility of increased pipeline imports from Algeria, although we do not include this in our scenarios because of ongoing diplomatic tensions.

Therefore, while the EU25 would manage comfortably without Russian LNG, the situation on the Iberian Peninsula would depend on the ability to find alternative LNG supplies. As they are traded by sea, LNG cargos are somewhat fungible. If Russian LNG stops flowing to the EU, Russia will look to sell this LNG elsewhere at the same time as EU buyers look for alternative supply. In theory, the global market should rebalance with an additional layer of friction caused by less efficient trade routes. This would be similar to the impact of the EU’s Russian crude oil embargo (McWilliams et al, 2022).

One limitation less present in the oil market is the volume of LNG, which is contracted under long-term contracts with fixed destination clauses, limiting the ability of markets to rebalance. However, the EU’s experience over the winter of 2022-23 suggests there is substantial flexibility in the market. Higher prices in Europe were well able to bring in additional cargos.

The return of the Freeport liquefication terminal in the US also provides a boost 8 Scott Disavino, ‘Freeport LNG seeks to restart commercial operations at Texas export plant’, Reuters, 13 February 2023, https://www.reuters.com/business/energy/natgas-flows-freeport-lngs-texa…. . A fire in June 2022 stopped operations at the terminal, which had accounted for 20 percent of the US LNG export capacity. The plant’s capacity of 200 TWh per year matches Russia’s total 2022 LNG to the EU. In May 2022, the last month before the fire, the plant shipped over half (10 TWh per month) of its cargo to the EU. We consider that the EU is likely to be able to find cargos to replace Russian ones.

4 Russian LNG exports without the EU

In any scenario in which Russian LNG stops flowing to the EU, the impacts on global markets and Russian revenues will depend on Russia’s ability to redirect cargos. If Russia is not able to redirect cargos, the extra demand from the EU in the market will have the effect of pushing up global LNG prices in a competition for a temporarily tighter supplies of global LNG.

In 2022, Russian LNG exports to the EU amounted to 197 TWh, or 44 percent of Russia’s total LNG exports. Exports to China accounted for a further 20 percent, and the rest of the world 36 percent. Figure 6 shows the evolution of these shares over the past three years.

Tight LNG markets mean that there is likely to be demand for Russian LNG, especially if it can be contracted at a discount to global prices. The experience of the EU’s crude oil embargo shows that Russia was able to find new buyers without difficulty as demand from the EU and G7 was withdrawn.

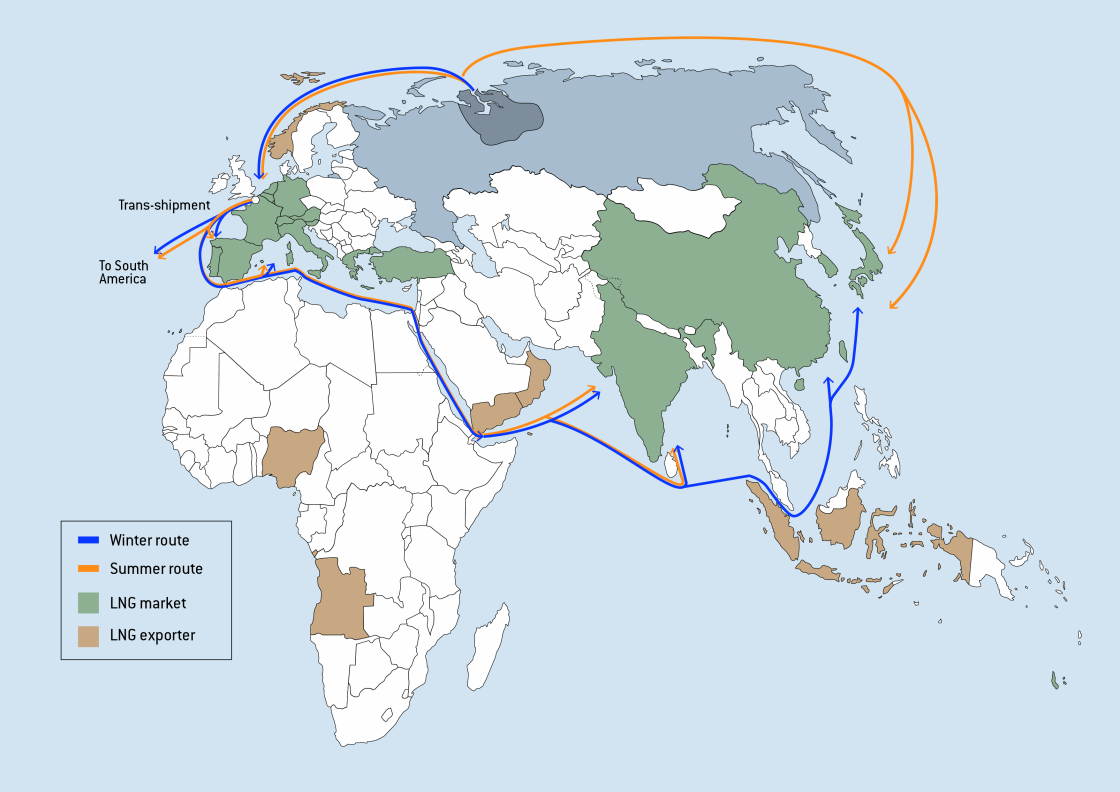

One peculiarity is the trade route a Russian LNG carrier must take. Much of the European LNG demand is served by LNG plants on the Yamal peninsula on the northwest Siberian coast. In summer months’ ships travel east to Asian markets where demand may be found for cargos no longer flowing to the EU 9 Outside of Asia, there would be relatively scarce and geographically close demand for Russian LNG. Turkey is already well supplied by pipeline, while demand in Africa is very low. . However, during the northern hemisphere winter – when LNG demand is typically higher – passing through the Arctic Circle is typically not possible. LNG carriers would have to embark on a substantially longer route via the Suez Canal, with higher costs 10 John Conrad, ‘Russian LNG Ship Concludes Northern Sea Route Voyage’, gCaptain, 27 June 2022, https://gcaptain.com/russian-lng-ship-northern-sea-route/. .

This route also involves trans-shipment via terminals in the EU, most notably Zeebrugge in Belgium (Figure 7) and the French terminal Montoir-de-Bretagne. Ships departing from Yamal unload LNG at Zeebrugge into storage or directly into different ships, in which it is then transported to Asian or other global markets. This trade is critical for smoothing year-round export from Yamal to Asian markets. Total volumes are significant, accounting for 12 percent of Yamal LNG exports in March 2022, and 38 percent of exports that were destined for Asian, Middle Eastern or South American markets 11 The Institute for Energy Economics & Financial Analysis LNG tracker shows volumes of Russian LNG trans-shipped via European ports. See https://ieefa.org/european-lng-tracker. . The trade is governed by a long-term contract that began in December 2019, allowing for up to 110 TWh per annum.

The additional cost for Russia to re-direct cargos would depend on whether these services were still feasible in a scenario in which direct Russian LNG trade with the EU ends. Russia is also developing its own abilities for trans-shipment via domestic ports, including Murmansk.

Figure 7: Transportation of LNG from Yamal terminal to buyers

Source: Bruegel based on Natural Gas World, ‘Project Spotlight: ARC7 LNG Carriers [LNG Condensed]’, 13 January 2021, https://www.naturalgasworld.com/project-spotlight-arc7-lng-carriers-lng-condensed-83812.

BOX 1: Status of EU-Russian LNG trade

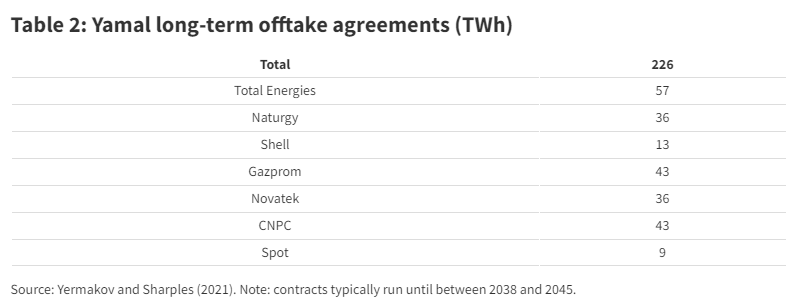

Exports to the EU from Russia mainly depart from the Yamal LNG terminal. The terminal has an export capacity of 16.5 million tonnes LNG per annum (235 TWh). The ownership of the terminal is a joint venture between Novatek (50.1 percent), Total Energies (20 percent) 12 France’s Total has said it will continue its Russian LNG activities as long as no sanctions are applied. See Reuters, ‘TotalEnergies to continue shipping Russian LNG as long as no EU sanctions -CEO’, 5 October 2022, https://www.reuters.com/business/energy/totalenergies-continue-shipping…. , China National Petroleum Cooperation (20 percent) and the Silk Road Fund (9.9 percent). Over 90 percent of the exports from the Yamal terminal are covered by long-term contracts (Table 2). To attract this foreign investment into the Yamal LNG terminal, the Russian government provided a temporary exemption for exports from export duty and mineral extraction taxes. Firms that export from the terminal do pay a 34 percent tax on profits (Corbeau, 2023).)

The terms of these contracts are not publicly available, and therefore we do not have information on the prices paid for these LNG cargos. Typically, contracts will contain a weighted lag of regional or global natural gas pricing indicators. The exact terms of the contract are relevant for assessing the impact of sanctions, as they will determine the lost export revenues when compared to the ability of Russia or Novatek to resell unwanted cargos on the spot LNG market.

5 Options for the EU

The EU’s target of phasing out Russian fossil-fuel imports by 2027 implies that long-term contracts will be interrupted before their end dates. Until they are interrupted, Russian LNG cargos cannot be considered a reliable component of the EU’s security of gas supply and the EU should work under the precautionary assumption that these flows might stop at any time.

In the first scenario, wait-and-see, the EU would continue to turn a blind eye to Russian LNG imports. Global natural gas markets should be better balanced in the second half of the decade as a new wave of liquefication projects come online. As the EU approaches its 2027 deadline for ending Russian fossil-fuel imports, an embargo could be discussed. This option is a cautious one and refrains from testing tight global LNG markets. However, it implies that EU consumers continue to send billions of euros to Russia for LNG.

A soft sanctions scenario, meanwhile, would discourage and ultimately prevent imports of spot LNG from Russia. It would also stop the renewal of expiring contracts and the signing of any new LNG contracts with Russia. At the same time, companies do have some flexibility over the volume of gas they import under long-term contracts, and could be encouraged to keep these volumes as low as possible. However, the scenario would not break the existing long-term contracts. Consequently, the EU would continue to import significant volumes of Russian LNG, while disruptions to the global market would be limited. This scenario is closest to our interpretation of the proposal that, at time of writing, has been put forward to the European Parliament, and which would prevent Russian companies from booking LNG-import capacities.

A more significant move would be for the EU to explicitly sanction the import of Russian origin LNG (our EU embargo scenario). This would force importing companies to declare force majeure and exit existing long-term contracts. Consequently, the EU would cease to import Russian LNG and our analysis shows that the bloc would manage such a disruption. There would, however, be an impact on global LNG markets. The export of Russian LNG to the EU accounted in 2022 for a little over 3 percent of the total market, which would be the maximum supply shock. Any temporary increase in global prices would be determined largely by the ability of Russia to redirect cargos eastwards.

An alternative approach, EU embargo with Energy Platform offer, might be facilitated by the EU’s new Energy Platform. The platform was initiated in April 2022 as a joint purchasing mechanism for the EU. In the first tender, 63 companies submitted requests for a total volume of 120 TWh of natural gas. The platform would be suitable as an EU vehicle to coordinate purchases of Russian LNG. After terminating existing long-term contracts with Yamal LNG, the EU as a bloc could then offer to purchase Russian LNG at a lower than market price, which may be revised, depending on the evolution of the situation in Ukraine.

Table 3: Russian LNG, EU options

|

|

Wait-and-see |

Soft sanctions |

EU embargo |

Embargo & offer to purchase via Energy Platform |

|

EU continues to pay Russia |

Yes |

Yes |

No |

Partly |

|

Risk of significantly tightening global LNG market |

No |

No |

Yes |

Partly |

|

Requires unanimity among EU countries |

No |

No |

Yes |

Yes |

Source: Bruegel.

This coordination mechanism would provide a pathway for the termination of long-term contracts that run post-2027, while smoothing any bumps to the gas market caused by the gradual phase-out of Russian LNG. It would also allow the platform mechanism to distribute volumes to areas of greatest need. There is no guarantee that Russia would wish to engage with such a strategy, and Russia might prefer to refuse any LNG exports to the EU. Russia’s compliance with the oil price cap, following an earlier declaration that it would be ignored, does however suggest cooperation may be forthcoming. Based on economic logic alone, geographical proximity implies that Russia should be willing to accept a discount on exports to the EU market. In any case, pursuing this fourth option must only be done on the basis that the EU is ready for a full termination.

Beyond imports, the EU also faces a decision on the future of Russian LNG trans-shipment via EU ports. These trans-shipments are important for Yamal LNG to reach global markets, especially during winter months. Limiting these trans-shipments would be an even more aggressive step. It would increase the difficulty for Russia to re-route LNG cargos, but likely exacerbate global LNG tensions. The EU might consider a temporary tax or price limit on cargos using such trans-shipment facilities. In recent years, construction has been underway on two new terminals to facilitate trans-shipment in Russia. While trans-shipments are already taking place at the port of Murmansk in Russia, the exact capacity of the terminals and whether they are already able to replace all the volumes passing through Zeebrugge is not clear. It is possible that technology sanctions may have had an impact by delaying projects.

Such a strategy could be expanded into a full price cap on Russian LNG traded with third countries. In similar fashion to the trade in crude oil, EU and G7 members have significant control over the ownership and insurance of the ships used to transport Russian LNG. Between January and May 2023, all ships were insured by, and over 90 percent were owned by, companies resident in the EU or G7 13 Authors analysis of the CREA Russia Fossil Fuel Tracker API; see https://www.russiafossiltracker.com/. . One complication with imposing a price cap on LNG trade is that it is typically governed by long-term contracts with prices determined by a fixed formula. The price-cap mechanism therefore may not be appropriate for all Russian LNG exports but could be applied to exports from Yamal that may be sold on the spot market in a scenario in which an EU embargo puts an end to existing long-term contracts.

At the same time, the EU is yet to introduce sanctions on Russian pipeline gas imports and continues to import Russian gas by pipeline at roughly comparable volumes to LNG. These pipeline imports could be negotiated through the Energy Platform. Such a strategy would provide a European tool for exerting pressure on Russia, in the context of the EU’s ambition to develop strategic autonomy capabilities. The strategy has a clear aim of reducing dependency on an adversary and of phase this risk out gradually over time, while approaching the situation from a position of relative strength.

6 Conclusions

LNG has become a crucial element of Europe’s security of energy supply. Flows from Russia have formed an important part of this for the past 18 months. However, the EU must now seriously assess whether this trade has a future. The possibility that Russia unilaterally blocks exports of LNG to the EU remains, and the EU must be prepared for such a risk. Moreover, the EU should consider sanctioning Russian LNG. Continuing the trade implies that European consumers will continue to send money directly to Russia and will remain dependent on an unreliable entity.

Our analysis has shown that the EU would manage without Russian LNG. Impacts over the summer months should be very limited, while winter months may see marginal price increases. The extent of these price increases depends on the overall tightness of the global LNG market, which determines the premium EU markets must pay to attract flexible LNG cargos. The impact of an end to Russian LNG would not be comparable to the shocks caused by the drop in Russian pipeline gas flows in 2022.

Meanwhile, Russia is likely to be able to re-route a large share of its LNG cargos. In the short run, there may be frictions in finding new buyers, especially during winter months, depending on the situation regarding trans-shipments in Europe. Ultimately, new buyers will step in for LNG cargos, as shown by the shift in Russia’s oil trade. The introduction of a price cap for access to EU or G7 controlled trans-shipment facilities, vessels and shipping insurance would increase the difficulties for Russia in re-routing. Nonetheless, the volume of the trade implies that sanctions will not have the same impact as the oil embargo and price cap in terms of reduced revenues for Russia.

Given that the EU will be able to manage the shock, and that a scenario of inaction or limited sanctions implies that EU consumers will continue to fund the Russian state, and by extension the Russian war effort, we argue that the EU should bring forward a full embargo on Russian LNG. An embargo would also reduce exposure to an unreliable and adversarial entity. The embargo may be designed to allow purchases only if they are coordinated via the EU Energy Platform. Dealing as a bloc with Russian LNG would maintain the EU’s strategic position, allowing it to wind down imports in line with the 2027 target. Moreover, offers could be made to purchase Russian LNG at below market prices, with the accompanying threat or actual introduction of a price cap.

Demertzis, M. and B. McWilliams (2023) ‘How much will the EU pay Russia for fossil fuels over the next 12 months’, Analysis, 23 March, Bruegel, available at https://www.bruegel.org/analysis/how-much-will-eu-pay-russia-fossil-fuels-over-next-12-months

McWilliams, B. and G. Zachmann (2023) ‘European natural gas demand’, Bruegel Datasets, available at https://www.bruegel.org/dataset/european-natural-gas-demand-tracker

McWilliams, B., G. Sgaravatti and G. Zachmann (2023) ‘European natural gas imports’, Bruegel Datasets, available at https://www.bruegel.org/dataset/european-natural-gas-imports

McWilliams, B., S. Tagliapietra and G. Zachmann (2022) ‘Will the European Union price cap on Russian oil work?’, Bruegel Blog, 7 December, available at https://www.bruegel.org/blog-post/will-european-union-price-cap-russian-oil-work

Corbeau, Anne-Sophie (2023) ‘Implications of EU Restricting Russian LNG’, Energy Explained Blog, Center on Global Energy Policy, 5 April, available at https://www.energypolicy.columbia.edu/implications-of-eu-restricting-russian-lng/

Yermakov, V. and J. Sharples (2021) ‘A Phantom Menace: Is Russian LNG a Threat to Russia’s Pipeline Gas in Europe’, OIES Paper NG 171, Oxford Institute for Energy Studies, available at https://www.oxfordenergy.org/wpcms/wp-content/uploads/2021/07/Is-Russian-LNG-a-Threat-to-Russias-Pipeline-Gas-in-Europe-NG-171.pdf

The European gas market is complex and heavily interconnected. Foreign gas enters the market through pipelines or LNG terminals. This gas then continues its journey through European pipelines, often crossing multiple international borders, before being dispersed into city centres and industrial clusters. With gas crossing multiple borders, tracking the true origin is complicated. We include all gas flows into and across Europe and apply Wassily Leontief’s Nobel prize winning input-output matrix, using the average share of gas in each country to attribute proportions to origin countries. In this way we split gas imports by Russia (Nord Stream, Yamal, Ukraine Transit, Turkstream, Other), Norway, Azerbaijan, North Africa, domestic production in the United Kingdom, the Netherlands, or elsewhere and LNG according to source country.

The main dataset used is the ENTSO-G transparency platform. We queried all points both within and entering the EU’s gas market. Manual validation was necessary to remove redundant points due to duplication of direction (ie when both imports and exports of the same gas are reported), duplicates by operator (ie where the same gas is reported by multiple operators and aggregators), duplicates by point (ie when points are duplicated). We compared the resulting dataset to a range of sources including the International Energy Agency, Eurostat and the Agency for the Cooperation of Energy Regulators. Our data is broadly consistent across these sources – although discrepancies among the range of sources are noted.

We take LNG data from the Bloomberg terminal. Bloomberg’s ship tracking shows the origin of ships which arrive in LNG ports. We combine this monthly proportionally with the LNG send-out recorded from each terminal on the ENTSO-G platform.

We computed average daily imports between 1 September 2022 and 30 May 2023, which we took as the most relevant period for assessing the EU import potential following the substantial cuts to Russian pipeline flows. On average imports to the EU25 were 244 TWh/month and 26 TWh/month to the Iberian Peninsula. This includes the average net trade between France and Spain from 2017 to 2021. We then subtracted actual Russian LNG monthly imports from 2022 to calculate an average import rate net of Russian LNG. This provides an assumption of monthly imports to the EU25 of 232 TWh and to the Iberian Peninsula of 21 TWh, in a scenario of no Russian LNG.

[1] Liquefied natural gas is natural gas that has been cooled down to liquid form, for transport in dedicated ships.

[2] Ewa Krukowska and John Ainger, ‘EU Aims to Give Members Option to Block Russian LNG Imports’, Bloomberg, 28 March 2023, https://www.bloomberg.com/news/articles/2023-03-28/eu-aims-to-give-members-option-to-block-russian-lng-imports.

[3] As part of the revision of the EU Gas Regulation, ongoing at time of writing; see https://www.europarl.europa.eu/legislative-train/theme-a-european-green-deal/file-revised-regulatory-framework-for-competitive-decarbonised-gas-markets-2.

[4] See summary information about sanctions at https://eu-solidarity-ukraine.ec.europa.eu/eu-sanctions-against-russia-following-invasion-ukraine_en.

[5] At national level, the Dutch and Spanish governments have announced plans to wind down contractual Russian LNG imports, and have asked importers not to sign additional contracts for Russian LNG. See Cagan Koc and Diederik Baazil, ‘Netherlands Plans to End Russian LNG Imports, Minister Says’, Bloomberg, 12 April 2023, https://www.bloomberg.com/news/articles/2023-04-12/netherlands-plans-to-end-lng-imports-from-russia-minister-says, and Stephen Stapczynski, Thomas Gualtieri and Anna Shiryaevskaya, ‘Spain Urges LNG Importers to Diversify Away From Russian Supply’, Bloomberg, 24 March 2023, https://www.bloomberg.com/news/articles/2023-03-24/spain-urges-lng-importers-to-diversify-away-from-russian-supply.

[7] See Council of the EU press release of 28 March 2023, https://www.consilium.europa.eu/en/press/press-releases/2023/03/28/member-states-agree-to-extend-voluntary-15-gas-demand-reduction-target/.

[8] Scott Disavino, ‘Freeport LNG seeks to restart commercial operations at Texas export plant’, Reuters, 13February 2023, https://www.reuters.com/business/energy/natgas-flows-freeport-lngs-texas-export-plant-jump-refinitiv-data-shows-2023-02-13/.

[9] Outside of Asia, there would be relatively scarce and geographically close demand for Russian LNG. Turkey is already well supplied by pipeline, while demand in Africa is very low.

[10] John Conrad, ‘Russian LNG Ship Concludes Northern Sea Route Voyage’, gCaptain, 27 June 2022, https://gcaptain.com/russian-lng-ship-northern-sea-route/.

[11] The Institute for Energy Economics & Financial Analysis LNG tracker shows volumes of Russian LNG trans-shipped via European ports. See https://ieefa.org/european-lng-tracker.

[12] France’s Total has said it will continue its Russian LNG activities as long as no sanctions are applied. See Reuters, ‘TotalEnergies to continue shipping Russian LNG as long as no EU sanctions -CEO’, 5 October 2022, https://www.reuters.com/business/energy/totalenergies-continue-shipping-russian-lng-long-no-eu-sanctions-ceo-2022-10-05/.

[13] Authors analysis of the CREA Russia Fossil Fuel Tracker API; see https://www.russiafossiltracker.com/.

About the authors

Related content

The European Union-Russia energy divorce: state of play

EU-Russia energy trade has fallen hugely since Russia’s invasion of Ukraine, but the EU could still do more to reduce dependence

European natural gas imports

This dataset aggregates daily data on European natural gas import flows and storage levels.

The Letta report: an assessment of the energy proposals

The report has the potential to substantially impact the European Union's strategic agenda from 2024-29