The European Union should sanction Sberbank and other Russian banks

EU should extend harsh sanctions to most or all of the largest Russian banks, including the largest that plays a central role in its financial system.

The swift early European Union response to Vladimir Putin’s aggression in Ukraine was designed to disrupt Russia’s financial system and economy. Ending EU imports of Russian hydrocarbons would be a most powerful next step, and is an absolute priority. But other actions can and should be taken while an oil and gas ban is being debated. Specifically, the EU should extend harsh sanctions to most or all of the largest Russian banks, including the largest that plays a central role in its financial system, Sberbank. There is no good reason for the EU not to do so immediately.

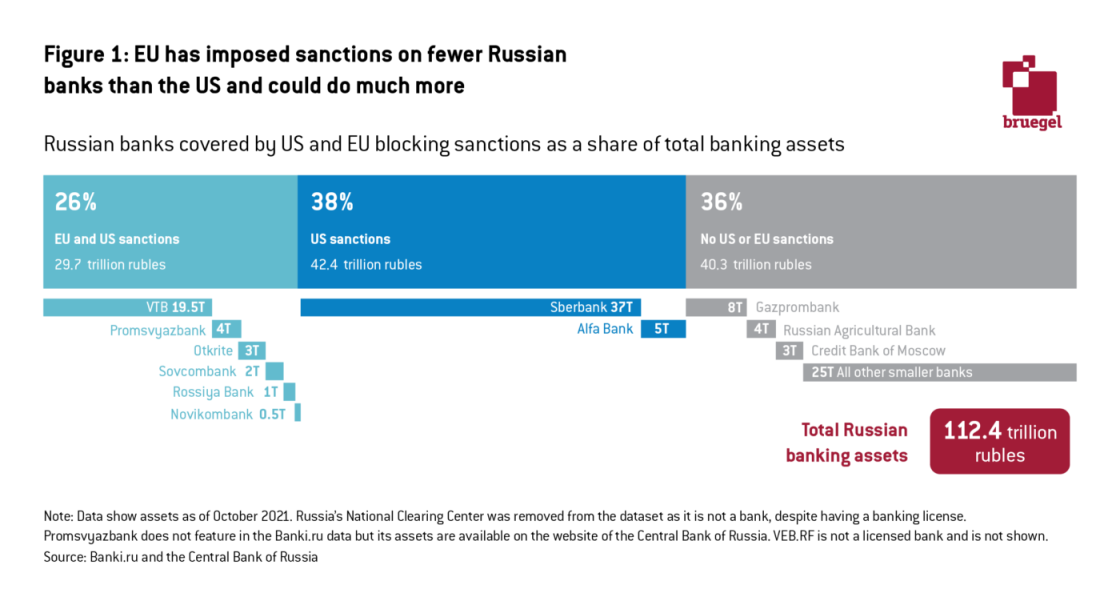

On 6 April 2022, the United States Treasury announced full “blocking” sanctions on Sberbank and on Alfa-Bank, Russia’s fourth-largest bank, meaning US entities cannot conduct any transactions with them and their US assets are frozen. Together with previous actions announced on 22 February and 24 February, this leaves six out of Russia’s top 10 banks, representing more than 60 percent of total Russian banking assets, largely or completely prevented from any transactions subject to US jurisdiction. While the United States could do more, this is much more than equivalent EU action. Of those same top 10 banks (leaving aside the central bank), the EU has only blocked four that do not include Sberbank, adding up to only a quarter of total Russian banking assets.

The notion of European timidity on banking sanctions may sound awkward, given how the EU has been rightly praised for its bold actions on the financial front, just two days after Russia’s invasion of Ukraine on 24 February. The sanctions on the Central Bank of Russia (CBR), applied by the EU together with the United States, the United Kingdom, Canada, Japan and other jurisdictions have shattered the myth of a financial ‘fortress Russia’ and forced the CBR to raise policy rates and introduce capital controls, with severe negative impact for Russian credit and growth prospects, notwithstanding Russia’s single-minded effort to shore up the ruble.

When it comes to individual banks, however, the EU so far has concentrated its financial fire on only seven Russian financial institutions: VTB (Russia’s second-largest bank by assets as of October 2021), Promsvyazbank (#6), Otkritie (#8), Sovcombank (#9), Rossiya Bank (#16), Novikombank (#24) and the investment company VEB.RF - which is not licensed as a bank, but has assets that would place it in the top 10 if it were. Three of these were the targets of blocking sanctions on 23 February, the day before the invasion. Then on 1 March, the EU excluded all seven from access to SWIFT, the Belgium-based global payment messaging system (three Belarusian banks were added a week later). Finally, on 7 April, the remaining four also came under full blocking sanctions, which puts an end to a rather senseless loophole that allowed for the continuation of correspondent banking services without using SWIFT. These sanctions cover the entire European Economic Area, not just the euro area. But they leave the vast majority of Russia’s banking system untouched.

Why has the EU been so cautious? The initial round of sanctions on the CBR was without precedent for a country of that size and systemic importance. It may have been appropriate for the EU not to add further financial stress at the same time out of financial stability concerns. That motivation for prudence, however, no longer applies. The European Central Bank, in its role as euro area banking supervisor, has carefully monitored possible contagion channels and suggested, in a letter to European parliamentarians on 6 April, that there is currently no reason for alarm from euro area bank exposures to Russia. EU banks with large Russian operations have either signalled their forthcoming exit from the country, or in the case of Société Générale, announced it. All this considered, it does not appear that intensifying EU sanctions on individual Russian banks would materially threaten European financial stability.

The current EU stance of maintaining significant purchases of Russian oil and gas is not a reason to delay such intensification either. Put succinctly, EU buyers of Russian hydrocarbons don’t need Sberbank to purchase the stuff. They can operate through a much narrower banking channel, either one Russian bank (large or small) that is left unsanctioned for that purpose, or even through a sanctioned bank using an authorised facility carved out of sanctions to allow oil and gas transactions. That bank may be Gazprombank (and/or its cousin the Russian Regional Development Bank, an affiliate of Rosneft), or another institution as may be deemed fit. Even assuming that some ongoing oil or gas supply contracts are currently serviced through Sberbank (or Alfa or another bank that has not yet been on the EU sanctions list), that banking relationship can presumably be switched to another institution without that constituting a breach of contract. Funnelling all energy sales through one approved banking facility (or a small number thereof) will have the added benefit of making monitoring of volumes easier across the EU, increasing the likelihood that EU countries will agree and adhere to reductions, if not the elimination of imports in the near future.

If the Russian authorities take that as a pretext to stop deliveries, so be it — but that risk exists no matter what, even though the late-March test of will over the separate issue of payment in rubles suggests it is rather low. In order to prevent humanitarian damage from the sanctions on banks, and to preempt Russian propaganda blaming the EU for imaginary such impact, the sanctions regime should include ‘humanitarian channels’ — approved facilities set up to facilitate the sale of medicine, medical devices, and food- and agricultural-related goods from the EU to Russia. Additional channels could be provided for entities from non-EU countries to keep buying from Russia, even if the Russian bank involved in the transaction has been cut off from SWIFT: in that case, they would only need to use a different, presumably less efficient messaging system.

Imposing blocking sanctions on Sberbank and the other large Russian banks currently left untouched by EU sanctions — namely Alfa-Bank, Russian Agricultural Bank, Credit Bank of Moscow, Bank Saint Petersburg, Tinkoff Bank and more — may not dramatically change the environment of Russia’s economy and would definitely be a less momentous decision than stopping EU oil and gas purchases. Even so, it would create pervasive impediments to hitherto unsanctioned international business for a wide range of economic actors in Russia and would also make it incrementally more difficult for Russian entities to circumvent some of the other sanctions already in place. Importantly, it can be done without delay and at no major cost to the EU or like-minded countries. Given the atrocities committed by Russia and its disruption of Europe’s fundamental security norms, there is much more risk in doing too little than in doing too much.

Recommended citation:

Kirschenbaum, J. and N. Véron (2022) ‘The European Union should sanction Sberbank and other Russian banks’, Bruegel Blog, 15 April

Help from Egor Gornostay, Nia Kitchin and Oliver Ward at the Peterson Institute is gratefully acknowledged.

About the authors

Related content

The European Union should do better than confiscate Russia’s reserve money

The EU can use interest income made on immobilised Russian reserve assets to support Ukraine, but confiscating the assets now would be a mistake

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

European capital markets union: make it or break it

Capital markets union has not delivered, but it should be given a last chance, with a focus on supervisory integration