The oil price cap and embargo on Russia work imperfectly, and defects must be fixed

Violations of the G7 price cap on Russian oil are becoming evident, but Western countries still can tighten rules and reduce the cash flows to Russia.

The unprecedented and extensive sanctions to limit Russia’s oil export income, including the European Union embargo and an oil price cap imposed by the G7 in December 2022, have successfully reduced Russia’s export earnings and budget revenues. In the wake of the sanctions, Russia’s current account surplus fell to $23 billion in January-to-May 2023 from $124 billion in the same period a year earlier 1 Bank of Russia, ‘Estimate of Key Aggregates of the Balance of Payments of the Russian Federation’, 11 July 2023, https://www.cbr.ru/eng/statistics/macro_itm/svs/bop-eval/. . The Russian finance ministry also reported about a 50 percent year-on-year drop in government oil revenues in January-May 2023, and a widening budget deficit 2 Ministry of Finance of the Russian Federation, 'Brief information on the execution of the federal budget' (in Russian), https://minfin.gov.ru/ru/statistics/fedbud/execute/. .

Less clear however is the impact of each different measure initiated by the West to punish Russia for its invasion of Ukraine. Evidence indicates that the oil embargo has had more of an effect than the price cap, in part because the cap has been set too high and enforcement is lacking.

Because of the EU embargo, European buyers of Russian oil have essentially disappeared, and Russia is accepting price discounts to maintain export volumes from the Baltic and Black Sea ports that have traditionally supplied Europe. Russia’s tax revenues have fallen as prices in this market are used to calculate taxes from oil. In an attempt to prop up oil prices, Russia announced on 2 April 2023 a production cut of 500,000 barrels per day 3 Reuters, ‘Novak says Russia to extend 500,000 bpd oil production cut until end of year’, 2 April 2023, https://www.reuters.com/business/energy/novak-says-russia-extend-500000…. . The finance ministry also changed the oil price benchmark it uses to calculate oil taxes to take into account the shifts away from exports to Europe 4 Rosemary Griffin and Elza Turner, 'Russia to use Dated Brent in tax calculations to protect state budget from Urals discount', S&P Global, 16 February 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-ne…. .

The price cap, meanwhile, was intended as an innovative step to reduce Russia’s revenues while keeping its oil flowing to the global market. It allows G7/EU providers of shipping services, including shipowners and insurance companies, to remain involved in the trade with Russian oil as long as the oil is sold below a certain price. This threshold was set at $60/barrel for crude oil. There was scepticism about the price cap regime’s effectiveness when it was announced, citing the potential for circumvention. But the problems appear to be more fundamental.

For a major segment of the Russian export market – shipments of Urals-grade crude from Baltic and Black Sea ports – the EU embargo has driven down prices so much that the $60/barrel cap has become irrelevant. As for exports from Pacific Ocean ports, which never supplied Europe and where, therefore, the EU embargo could not have an impact, prices have stayed above the $60/barrel threshold. But G7/EU companies remain involved to a significant degree, indicating that the cap is not enforced properly. The introduction of the cap did, however, ensure that Russian oil remained on the market (Hilgenstock et al, 2023), and global prices did not rise because of lower supply. This objective was a key concern of the sanctions coalition.

Because of these defects, financial-sector sanctions should be adopted to strengthen oil price cap implementation and curb Russia’s ability to accumulate assets abroad.

Price cap violations are occurring

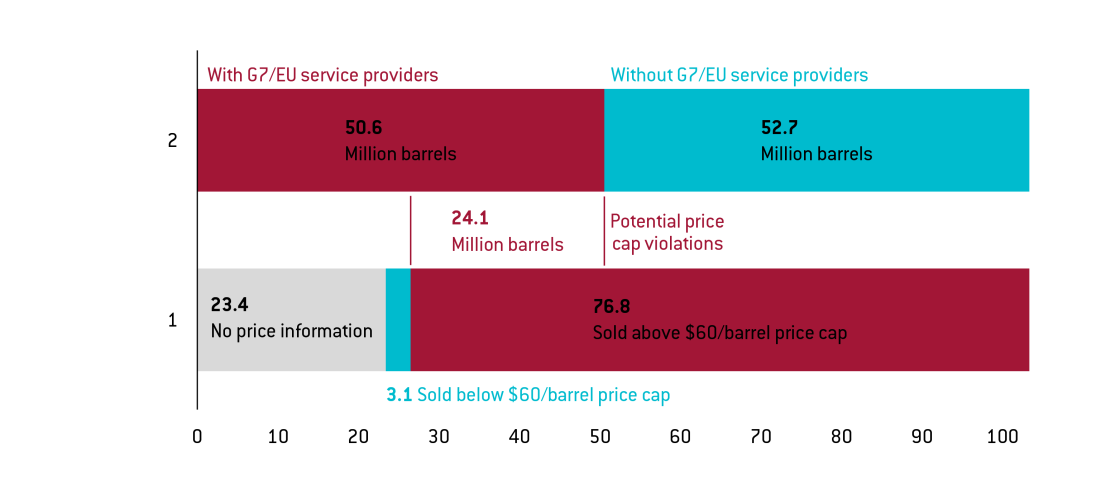

Evidence of potentially widespread violations of the price cap has emerged at Russia’s Pacific port of Kozmino (Hilgenstock et al, 2023). Data on shipments shows that in the first four months of 2023, half of the oil was exported on vessels either owned or insured by G7/EU entities (Figure 1, top bar). At the same time, 96 percent of exports for which price information is available were priced above the cap’s $60/barrel threshold, with an average price of more than $70/barrel (Figure 1, bottom bar). This means that at least 24 million barrels with a price above $60/barrel appear to have been transported on vessels that fall under the cap’s regulations 5 Price information is not available for shipments that appear in trade data under transaction terms other than FOB (free on board), on which the price cap is applied. . These violations are likely the result of straightforward falsification of the records 6 See European Commission oil price cap frequently asked questions, as of 30 June 2023, https://finance.ec.europa.eu/system/files/2023-06/guidance-russian-oil-…. oil buyers are required to provide to G7/EU shipping and insurance companies to demonstrate price-cap compliance.

Figure 1: Potential price cap violations in January-April 2023

Sources: Equasis, Kepler, Russian authorities, authors' calculations

To address these problems, financial institutions should be required to inform implementing agencies (such as the US Office of Foreign Assets Control, the UK Office of Financial Sanctions Implementation and similar agencies in EU countries) of any transactions under the cap that they facilitate, and to notify them of suspicious activities. Regulators should also require G7/EU insurance and shipping companies to retain full documentation on trades, contracts and transaction prices. Sanctions should be enforced on a ‘strict liability’ basis, meaning commercial participants would be liable for violations. Additional financial institutions in Russia and third countries should be subject to sanctions.

‘Shadow reserves’ available to Russia are a problem

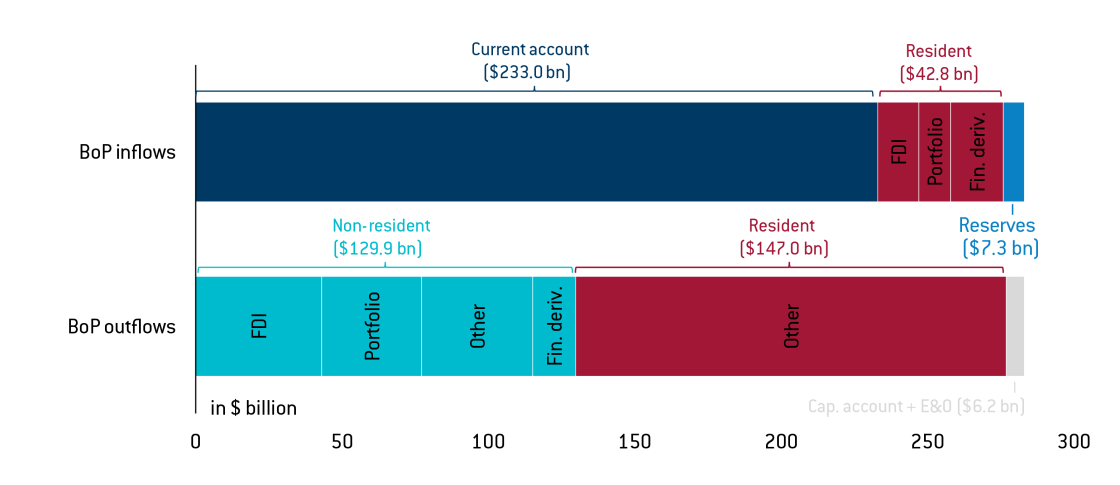

Russia’s export earnings from oil remain substantial, at about $50 billion in January-April 2023 (Hilgenstock et al, 2023). As the Bank of Russia has not been able to conduct reserve operations in US dollars or euros because of sanctions imposed in early 2022, Russian banks and corporates acquired $147 billion in new assets abroad in 2022 7 Bank of Russia, ‘Estimate of Key Aggregates of the Balance of Payments of the Russian Federation’, 11 July 2023, https://www.cbr.ru/eng/statistics/macro_itm/svs/bop-eval/. (Figure 2), and little is known about their physical locations or currencies of transaction. These funds may not formally belong to the Russian government, but they could be used to increase monetary and fiscal policy space.

Figure 2: Russian balance of payments flows in 2022

Source: https://www.cbr.ru/vfs/eng/statistics/credit_statistics/bop/bal_of_paym…

Western sanctions on the Bank of Russia and the National Wealth Fund immobilised assets and banned transactions; they did not affect flows into reserve funds held by Russian entities that may not formally belong to the state but could be used to buttress its finances and enable the government to circumvent energy sanctions and capture oil market arbitrage. The ownership structures of these entities are opaque. Russian energy companies may employ third-country shipping companies, oil traders and refineries to generate revenues in excess of the price cap.

Western central banks and bank supervisors should identify the exact nature and physical location of these ‘shadow reserve’ funds and remove them from the reach of the Russian regime, perhaps by imposing sanctions on third-country financial institutions 8 Alan Rappeport and Emily Flitter, 'Treasury Warns Foreign Banks Against Helping Russia Evade Sanctions', The New York Times, 13 May 2022, https://www.nytimes.com/2022/05/13/us/politics/russia-sanctions-evasion…. .

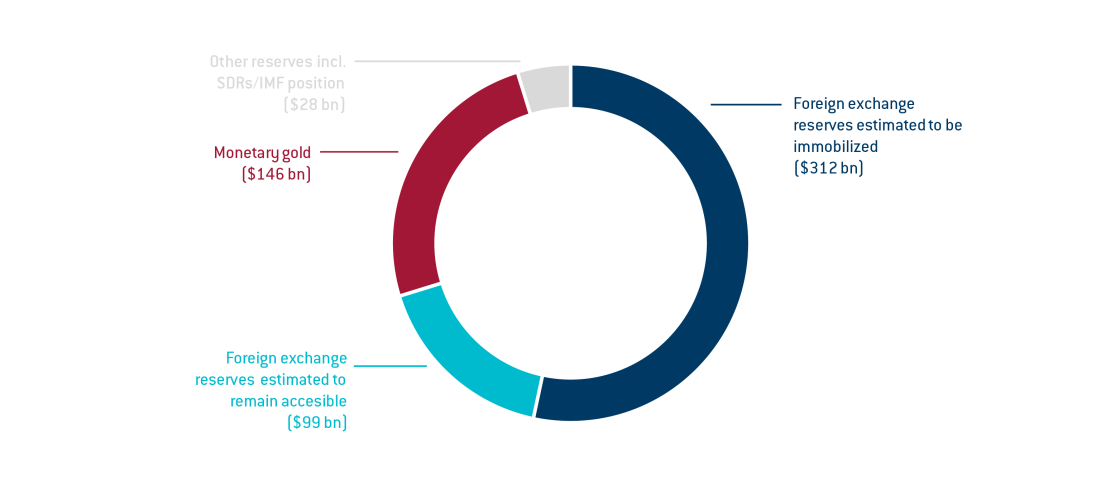

Since February 2022, sanctions appear to have restricted access to a substantial amount of Russia’s reserves, but information on these assets is limited. Roughly $312 billion is estimated to have been immobilised (Figure 3), but this number is based on Bank of Russia data. Coalition authorities should improve the transparency and credibility of sanctions enforcement by identifying these assets, publicly disclosing the information and ensuring that they these funds are effectively kept out of reach. The EU has taken an important step by expanding reporting obligations for frozen assets in its tenth sanctions package 9 See European Commission, questions & answers of 25 February 2023, https://ec.europa.eu/commission/presscorner/detail/en/qanda_23_1187. . Based on these new requirements, it found that it had immobilised more than $215 billion in Bank of Russia assets 10 Stephanie Bodoni and Alberto Nardelli, ‘EU Blocks More Than €200 Billion in Russian Central Bank Assets’, Bloomberg, 25 May 2023, https://www.bloomberg.com/news/articles/2023-05-25/eu-has-blocked-200-b…. .

Figure 3: Estimated composition of official reserve assets

Source: http://cbr.ru/eng/hd_base/mrrf/mrrf_m/

Shifts in the currency composition of Russian exports and imports have materialised since February 2022. Between the start of the full-scale invasion and the end of 2022, the share of US dollar and euro transactions in Russian goods trade fell from around 80 percent to slightly less than 50 percent, and the shares of ruble- and yuan-denominated transactions rose (Bank of Russia, 2023. Additional sanctions may compel Russia and China to cooperate further, while strengthening the negotiating power of China (and other emerging economies) over Russia. New financial sanctions should increase pressure on Russia’s financial resources.

References

Bank of Russia (2023) ‘ОБЗОР РИСКОВ ФИНАНСОВЫХ РЫНКОВ No. 2’, February, available at https://www.cbr.ru/Collection/Collection/File/43828/ORFR_2023-02.pdf

Hilgenstock, B., E. Ribakova, N. Shapoval, T. Babina, O. Itskhoki and M. Mironov (2023) ‘Russian Oil Exports under International Sanctions’, Yermak-McFaul International Working Group on Russian Sanctions & KSE Institute, April, available at https://kse.ua/wp-content/uploads/2023/04/Russian_Oil_Exports_under_International_Sanctions_23Q1_UPDATE26042023.pdf

A version of this analysis was published by the Peterson Institute for International Economics.

[1] Bank of Russia, ‘Estimate of Key Aggregates of the Balance of Payments of the Russian Federation’, 11 July 2023, https://www.cbr.ru/eng/statistics/macro_itm/svs/bop-eval/.

[2] Ministry of Finance of the Russian Federation, 'Brief information on the execution of the federal budget' (in Russian), https://minfin.gov.ru/ru/statistics/fedbud/execute/.

[3] Reuters, ‘Novak says Russia to extend 500,000 bpd oil production cut until end of year’, 2 April 2023, https://www.reuters.com/business/energy/novak-says-russia-extend-500000-bpd-oil-production-cut-until-end-year-2023-04-02/.

[4] Rosemary Griffin and Elza Turner, 'Russia to use Dated Brent in tax calculations to protect state budget from Urals discount', S&P Global, 16 February 2023, https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/021623-russia-to-use-dated-brent-in-tax-calculations-to-protect-state-budget-from-urals-discount.

[5] Price information is not available for shipments that appear in trade data under transaction terms other than FOB (free on board), on which the price cap is applied.

[6] See European Commission oil price cap frequently asked questions, as of 30 June 2023, https://finance.ec.europa.eu/system/files/2023-06/guidance-russian-oil-price-cap_en.pdf.

[7] Bank of Russia, ‘Estimate of Key Aggregates of the Balance of Payments of the Russian Federation’, 11 July 2023, https://www.cbr.ru/eng/statistics/macro_itm/svs/bop-eval/.

[8] Alan Rappeport and Emily Flitter, 'Treasury Warns Foreign Banks Against Helping Russia Evade Sanctions', The New York Times, 13 May 2022, https://www.nytimes.com/2022/05/13/us/politics/russia-sanctions-evasion-treasury.html.

[9] See European Commission, questions & answers of 25 February 2023, https://ec.europa.eu/commission/presscorner/detail/en/qanda_23_1187.

[10] Stephanie Bodoni and Alberto Nardelli, ‘EU Blocks More Than €200 Billion in Russian Central Bank Assets’, Bloomberg, 25 May 2023, https://www.bloomberg.com/news/articles/2023-05-25/eu-has-blocked-200-billion-in-russian-central-bank-assets#xj4y7vzkg.

About the authors

Related content

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up

Use the financial system to enforce export controls on Russia

The European defence industrial strategy: important, but raising many questions

The European defence industrial strategy helps to focus thinking but has significant flaws

Stay away from Russian money

The EU would shoot itself in the foot by confiscating Russian assets and giving them to Ukraine