The EU’s recovery fund proposals: crisis relief with massive redistribution

Poorer European Union countries and those hardest hit economically by the COVID-19 crisis could obtain up to 15% of their GNI in grants and guarantees

When European leaders convene this Friday (19 June), each will mainly look at how much her or his country can expect to receive from the European Commission’s recovery proposals. However, the Commission has so far shied away from publishing an estimate of national shares.

Limited guidelines were provided however on the estimated overall cross-country allocation in the Commission’s two recent proposals: the €750 billion ‘Next Generation EU’ plan and the additional €11.2 billion amendment to the 2020 annual budget. Cross-countries allocation proposals have been published for only three out of the twelve different instruments that make up the package: the Recovery and Resilience Facility, the Just Transition Fund and agricultural subsidies. Guidance is vague for the other nine, which account for about a third of the grant and guarantee components. The Commission either provided the detailed methodology behind cross-country allocations without any estimate (REACT-EU); indicated broad principles for cross-country allocations (Solvency Support Instrument and Invest EU); or provided no guidelines for cross-country allocation – for good reasons that I discuss.

A Commission staff working document (page 52) uses an “illustrative allocation key” assumed to be the same for all grant, loan and guarantee components of the package. But the regulation proposals, on the contrary, explain that each instrument will be allocated differently, and that there may even be no cross-country allocation key at all.

Moreover, three out of the 12 instruments operate in non-EU countries: Neighbourhood, Development and International Cooperation; Humanitarian Aid; the European Fund for Sustainable Development. Therefore, contrary to what some allocation estimates circulated in the media and on Twitter wrongly assume, no EU country will directly benefit from those instruments but all will contribute to their financing.

This post estimates the overall cross-country allocation of the recovery package’s grants and guarantees. Some countries would obtain 15% of their GNI in grants and guarantees; others less than 1%. The Commission’s proposal contains strong redistributive elements that will mainly benefit those countries hardest hit by the COVID-19 crisis, and those with the lowest GNI per capita. However, while some might try to identify winners and losers in the Commission’s proposal by focusing on each country’s ‘net contribution’, even a minor positive economic impact over the long term would be sufficient for the proposal to benefit all EU countries, even those that receive relatively small amounts. Finally I find that some countries would benefit from the proposed EU loan facility by more than one percent of their GNI in present value terms.

Grants and guarantees working for both insurance and redistribution

The overall package is composed of €438 billion in grants (including €5 billion for non-EU countries); €73 billion in guarantees (of which €11.5 billion is for non-EU countries); and €250 billion in loans. All figures here are measured at 2018 prices unless otherwise specified.

Methodology

In the annex, I summarise the cross-country allocation methodologies proposed by the Commission, so let me only highlight here a few key conceptual issues and my main assumptions.

- RRF – Recovery and Resilience Facility (€310 billion in grants from ‘Next Generation EU’): the basic cross-country allocation (with a number of caps and adjustments that benefit lower-income countries) would depend on (a) 2019 population, (b) the inverse of 2019 GDP per capita, and (c), more problematically, the 2015-2019 average unemployment rate. Why would a facility that aims to “achieve a fast and robust economic recovery in the Union” use outdated data from 2015-2019? Representatives of various countries already noted that such historical data has no direct connection to the pandemic-induced shock.

- REACT-EU – Recovery Assistance for Cohesion and the Territories of Europe (€50 billion in grants from ‘Next Generation EU’ and €4.8 billion in grants from the amended 2020 annual EU budget): the basic cross-country allocation would be based on (a) GDP contraction (67%), (b) level of total and youth unemployment in January 2020 (25%), (c) change in total and youth unemployment after January 2020 (8%). Again, it includes caps and adjustments to benefit lower-income countries; a special allocation to the outermost regions only in 2020; and payment to higher-income countries capped at 0.07% of their GNI. This ceiling would apply to ten countries, according to my estimates based on the spring 2020 European Commission forecast.

- Positive aspects of the allocation proposal: (a) 75% of the basic allocation key considers the adverse economic fallout from COVID-19; (b) the two-step allocation process allows the adverse economic fallout from COVID-19 up to summer 2021 to be considered in the allocation of funds.

- Negative aspects of the allocation proposal: (a) 25% of the basic allocation key relates to the January 2020 unemployment rate, which has no direct connection to the pandemic; (b) as many people who lost their jobs have not registered as unemployed, unemployment data paints only a partial picture of labour market losses. Employment figures would be more accurate.

- JTF – Just Transition Fund (€40 billion in grants: €30 billion from ‘Next Generation EU’ plus €10 billion from the ‘standard’ seven-year budget): the cross-country allocation considers carbon-intensive sectors (with 49% weight), employment in mining of coal and lignite (25%), employment in carbon-intensive industry (25%), production of peat (0.95%) and production of oil shale (0.05%), with an adjustment that favours lower-income countries, but with a cap. My Bruegel colleagues recommend dropping the less-reliable industrial indicators to focus instead on carbon intensity, incorporating the ambitiousness of the countries’ transition strategies into the allocation key; and taking a more granular approach to the allocation by considering smaller regions in the allocation (NUTS-3).

- EAFRD – European Agricultural Fund for Rural Development (€15 billion in grants from ‘Next Generation EU’ to top-up the ‘standard’ seven-year budget): same proposed cross-country allocation as in the May 2018 Commission proposal.

- SSI – Solvency Support Instrument (guarantees: €26 billion from ‘Next Generation EU’ and €5.3 billion from the amendment of the 2020 annual EU budget) and InvestEU (€30.3 billion guarantees from ‘Next Generation EU’ to top-up allocations in the ‘standard’ seven-year 2021-2027 budget): no country-specific allocation is provided, but the regulation proposals emphasise that these instruments should “focus on those Member States whose economies have been most affected by the effects of the COVID-19 pandemic and/or where the availability of State solvency support is more limited.” As the level of development does not feature as a possible factor, I consider here GDP losses since the first half of 2019 and the ratio of public debt to GDP, using a mathematical formulation comparable to that proposed by the Commission for RRF and REACT-EU.

- EU4Health (€9.4 billion in grants: €7.7 billion from ‘Next Generation EU’ plus €1.7 billion from the ‘standard’ 2021-2027 budget) and rescEU (€3.1 billion in grants: €2.0 billion from ‘Next Generation EU’ plus €1.1 billion from the ‘standard’ seven-year budget): no country-specific allocation is provided. As these instruments should be considered European public goods, country allocation is irrelevant. However, to allow for a better comparison between my estimates and others, I illustratively apportion these instruments according to countries’ shares of EU GNI. Since the marginal contribution to the EU budget is based on the shares in EU GNI, this hypothetical ex-ante allocation does not foresee any cross-country redistribution.

- Horizon Europe (€94.4 billion in grants: €13.5 billion from ‘Next Generation EU’ plus €80.9 billion from the ‘standard’ seven-year budget): no country-specific allocation is provided. Existing allocations of EU research funds are primarily based on excellence, with some dedicated instruments for cohesion in research. Excellence is rather persistent: the best research centres attract the best minds and therefore a research centre that successfully obtained EU funds in the past will likely be successful in the future too. For my illustrative calculations I therefore apportioned Horizon Europe funds to the 27 EU countries according to their previous shares in 2014-2018.

- NDIC – Neighbourhood, Development and International Cooperation (€86.0 billion in guarantees: €10.5 billion from ‘Next Generation EU’ plus €75.5 billion from the ‘standard’ seven-year budget), Humanitarian Aid (€14.8 billion in grants: €5 billion from ‘Next Generation EU’ plus €9.8 billion from the ‘standard’ seven-year budget) and EFSD – European Fund for Sustainable Development (€1 billion guarantees from the amendment of the 2020 annual budget): as these instruments are for non-EU countries I do not allocate funds from them to EU countries, but assume that EU countries contribute to their financing.

Estimated cross-country allocation of grants and guarantees

Grants: Italy and Spain would be the largest beneficiaries of grants in terms of euro values, while Bulgaria, Greece and Croatia would receive the highest shares of their GNIs, around 15%. Most other central and southern European countries would obtain about 6-10% of their GNIs while most high-income countries would get below 2% of GNI.

Guarantees: Italy and France would be the largest beneficiaries in raw euros numbers, while Greece would top the list in terms of GNI share. Central European countries would obtain less in guarantees as a share of their GNIs because their economic contraction is forecast to be less severe and they have lower public debts.

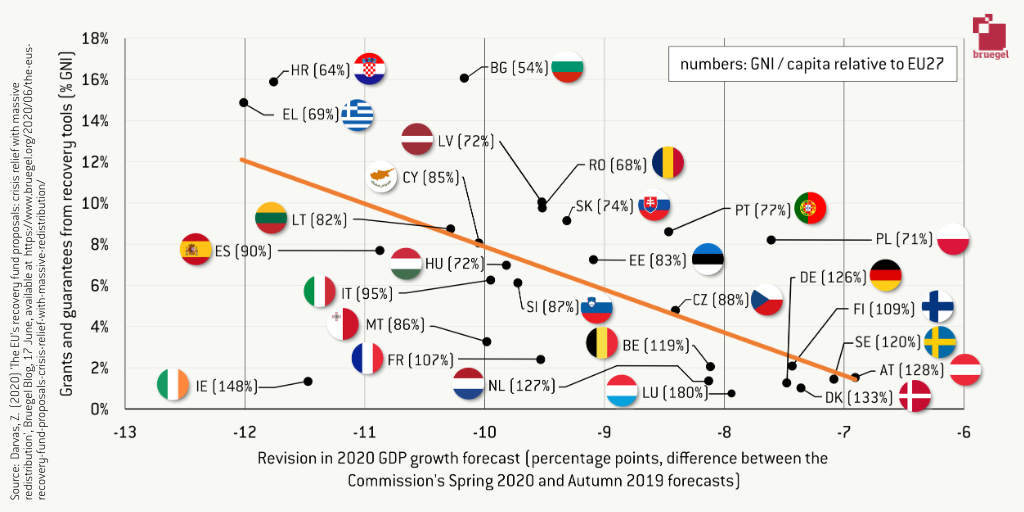

Cross-country allocations show both an insurance element (countries hit harder get more EU funds) and a redistribution element (countries with lower GNI per capita get more EU funds) (Figure 1).

Figure 1: Pandemic economic shock and support from the proposed EU recovery tools

Source: Bruegel.

Note: the numbers in brackets after the country codes indicate GNI/capita at Purchasing Power Standards relative to the EU27 average for 2021, according to the spring 2020 European Commission forecast.

The Commission’s downward revision of GDP growth forecasts between autumn 2019 and spring 2020 is a good proxy for measuring the severity of the pandemic’s economic shock. The amounts of grants and guarantees proposed for each country bear a noticeable association with the severity of the crisis’ impact at national level, suggesting that the package acts as insurance (Figure 1).

But the package also provides redistribution from richer to poorer countries: for a similar shock, countries with lower GNI per capita get much more. For example, the economic shock is almost the same in France, Slovenia, Hungary, Romania and Latvia. Yet France, which has a higher per capita income level, is estimated to get grants and guarantees amounting only about 2% of its GNI, while Latvia and Romania, which have lower per capita income levels, would get about 10%. This suggests that the proposed redistribution component of the recovery tool is very large. The European Council will have to provide a political guideline on this issue.

The massive redistribution component results from various adjustments to the allocation keys of the RRF, REACT-EU and JTF which favour countries with lower GNI per capita (see the annex).

Net contributions: impossible criteria

The EU is a deal-making machine. Each country tends to focus on what it perceives as its net contribution: how much more will it have to pay compared to how much it will receive. However in the particular case of the recovery package, estimating countries’ net contributions is impossible.

First, we cannot currently calculate net contributions. Funds from the recovery tools, financed by EU borrowing from capital markets for rather long maturities, will mainly be spent in 2021-2026. The Commission also proposed that EU debt would be repaid between 2028-2058. Net-contribution estimates thus need to take into account GNI forecasts for each EU country up to 2058, for which no reliable assumption can be made. A crucial question is whether nominal GNI growth will be faster than the nominal interest rate at which the EU can borrow, which is around -0.15% per year for 10 years and 0.3% per year for 30 years. If GNI growth is faster, the burden of debt repayment in the future would take a lower share of GNI than the share of current spending in current GNI.

Second, any calculation of net contributions today would fail to account for the fact that the recovery package is not a zero-sum game. The recovery package will likely have a positive impact on the economies of all EU countries. Increased public sector and EU spending during the recession implies more demand. This in turn can stimulate investment, economic activity and increased productive capacity – the very reason for the deployment of the EU recovery tool, which can also lead to long-term gains. A shallower recession due to EU spending could reduce the long-term negative impacts of the crisis, such as the number of unemployed people whose skills are gradually eroded due to inactivity. Cross-country spillovers also exert positive impacts, as exporting companies benefit from larger markets in other EU countries. In short, the recovery package leads to increased economic activity everywhere, at least over the short and medium terms, but possibly in the long term too.

Third, when we consider future benefits, even a minor long-term gain would make all countries into net beneficiaries of the recovery package. Since interest rates are so low, almost no discount is needed to calculate the present value of future excess income resulting from the recovery package. Suppose that the package increases German GDP by just 0.1% over the long term (that is, in each future year). This would imply that cumulatively over the next 100 years, German GDP would be 10% higher (=0.1%*100). A 10% of GDP net present value gain for Germany is several factors higher than the present value of the German contribution to the repayment of EU debt.

And finally, many EU countries found it difficult to absorb the ‘standard’ seven-year EU budget in the past. The proposed recovery package is additional to the seven-year budget and hence member states would need to absorb very large amounts in a short time, which could be challenging. Absorption rates below 100% would mean lower net contributions, but would also mean lower GDP and employment impacts.

An advantageous borrowing facility for some countries

Unlike grants and guarantees, the €250 billion in loans for EU countries does not involve redistribution between member states (unless, of course, borrower countries default and do not repay and the borrowing costs of guarantor countries do not increase due to the risk they run by guaranteeing the loans to other member states).

Most of the grants and all of the loans aim to finance investment and reform, as spelled out in the recovery and resilience plans in the context of the European Semester process. This comes with two limitations. First, as the loans can only be used for this purpose, the maximum loan volume for each member state cannot exceed the total cost of the agreed investment and reforms, minus the amount of grants received for the same purpose. Second, loans should remain below 4.7% of GNI of each country, though under exceptional circumstances this value could be exceeded.

At current prices, 4.7% of forecast 2021 EU GNI is €658 billion. However, the Commission’s proposed total loan volume is €250 billion at 2018 prices or €268 billion at current prices, suggesting the Commission does not expect all EU countries to apply for loans. Indeed, only countries that borrow at a higher rate than the EU borrowing rate would benefit from a loan from the EU.

Table 2 reports government bond yields for 10, 20 and 30 years of maturity, as well as similar yields of the European Stability Mechanism (ESM) and the European Investment Bank (EIB), on 12 June 2020. Such benchmark yields are not available for EU borrowing in Bloomberg, yet an investor presentation shows that the yields on EU bonds are rather similar to yields on ESM bonds (see slide 16 here).

The loan programme would represent non-negligible savings for some countries. Italy would benefit from the largest net present value gain (1.32% of its GNI) under the assumptions I discuss below, followed by Cyprus, Malta, Portugal and Slovenia. Lacking information on 30-years yields for Greece and 20-year yields of Spain, I could not do the calculations for these two countries, but I estimate that net present value gain for Greece would be between the values of Italy and Malta, while that of Spain would be similar to Portugal.

Countries that could borrow cheaper from the markets are indeed unlikely to borrow from the EU considering that the interest savings would be either small or even negative.

Loan calculations methodology:

Estimates of the net present value gain from borrowing from the EU are based on the following assumptions:

- ESM yields proxy EU borrowing rates.

- Lending rate of the EU to member states: EU’s own borrowing rate plus 10 basis points per year. The regulation proposal for the Recovery and Resilience Facility does not specify the interest rate to be charged on member states, but explains that “costs related to the borrowing of funds for the loans referred to in this Article shall be borne by the beneficiary Member States”. As the ESM lending rate to countries is about 10 basis points higher than the ESM’s own borrowing rate to cover ESM’s costs, I assume a similar charge for EU lending.

- All countries borrow 4.7% of GNI from the EU.

- EU borrowing from the market (and thus EU lending to member states) is assumed to be distributed as such: one third for 10 years, one third for 20 years and one third for 30 years. This is an arbitrary, yet illustrative assumption.

- For each year of all of these three maturities, I calculate the interest saving from borrowing from the EU or the interest costs for countries than can borrow below-EU rates; and add the assumed 10 basis point cost per year. Then I calculate the present value of these savings (or costs) using the yield of the member state in question as the discount factor.

- I do these calculations for euro-area countries for which 10, 20 and 30-year yields are all available. Given that Denmark maintains a fixed exchange rate to the euro, I also do calculations for Denmark. For non-euro countries with floating exchange rates, the relevant comparison would be their euro borrowing rates (if any), not their national currency borrowing rates.

An annex is downloadable here. It describes the proposed allocation criteria in more detail, specifies my methodology and specific assumptions underlying the calculation, and highlights that the measurement of some indicators in the Commission proposals are not defined.

Recommended citation

Darvas, Z. (2020) 'The EU’s recovery fund proposals: crisis relief with massive redistribution', Bruegel Blog, 17 June, available at https://bruegel.org/2020/06/the-eus-recovery-fund-proposals-crisis-relief-with-massive-redistribution/

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

The EU needs a methodology for including reform impacts in fiscal trajectories

Such a methodology, and a governance mechanism for managing associated risks, must be in place before the new fiscal framework kickstarts in September

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition