Third time lucky? China’s push to internationalise the renminbi

This paper analyses China’s different attempts to internationalise its currency and how they have fared.

Executive summary

Western concerns that the renminbi could rival the dollar as an international currency contrast with underwhelming numbers in terms of global settlements in renminbi and with the experience of China’s two main previous failed attempts to achieve renminbi internationalisation. However, China is moving towards a more realistic plan for renminbi internationalisation, focusing on China’s strengths in trade and financing. China is now the main trading partner for a very large number of countries and has become a major creditor for a good part of the Global South. This, together with the increasingly frequent restrictions on the use of the dollar, is strengthening the renminbi.

The cross-border use of the renminbi for trade settlements and financing (Chinese banks’ overseas loans denominated in renminbi and official renminbi swap lines offered by the People’s Bank of China) has been on the rise since 2022, coinciding with Russia’s invasion of Ukraine and the related Western sanctions. The increase is notable considering that the renminbi has been depreciating since January 2023 and China’s economic performance has been underwhelming. However, the use of the renminbi as investment currency has declined since 2022, in terms of both the share of foreign-exchange reserves denominated in renminbi and the share of Chinese onshore assets held by foreign investors.

The current push is so far proving successful compared to previous attempts, but it remains hard to tell if China will succeed in this renewed attempt to internationalise its currency through use of its heavy weight among trading nations. Obvious constraints remain that could hold back full internationalisation of the renminbi, especially the absence of full capital account convertibility. Nevertheless, China’s somewhat heterodox approach to internationalising its currency could succeed given the ongoing placing of restrictions on use of the dollar. How the dollar, the euro or the international monetary system may be further affected by the rise of the renminbi is a major policy question that must be explored further.

1 Introduction

China is an economic giant not only in terms of manufacturing and exports, but also in terms of the size of its financial sector. China’s financial sector is now the largest in the world, with $60 trillion in assets, equating to 340 percent of China’s GDP. Chinese banks also top the list of the largest globally systemic financial institutions, with increasing interrelationships with the rest of the global financial system

1

Alicia García-Herrero, ‘China’s new regulator hints at a major clean-up of the world’s largest financial sector’, First Glance, 13 March 2021, Bruegel, https://www.bruegel.org/first-glance/chinas-new-regulator-hints-major-c….

. However, China’s currency, the renminbi is little used internationally, at least when compared with the size of China’s economy and financial sector.

There are three main reasons for this. First and foremost, the renminbi is not fully convertible, which means it cannot move freely in and out of China. Second, the legal framework surrounding renminbi payments is uncertain. In particular, investors continue to lack confidence about the rule of law in China. Third, China’s financial markets, especially the Treasury market, are less liquid than US markets, and there is no expectation that this will change any time soon (García-Herrero, 2021).

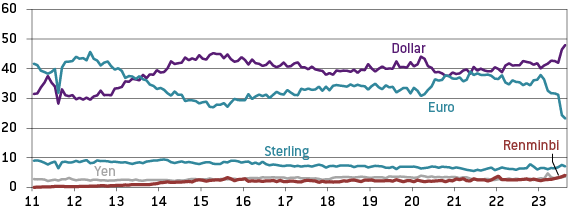

According to the financial messaging provider Swift, the share of renminbi payments in total cross-border transactions increased somewhat during the first half of 2023, but remains low at 3 percent, compared to 46 percent for the dollar and 24 percent for the euro (Figure 1). The dollar and euro shares have seen the largest movements since the start of 2023, with a significant increase for the former, and a sharp reduction for the latter. It is hard to understand why the euro has suffered the most in terms of international settlements since usage constraints have been placed on the dollar as much as on the euro, if not more. The euro’s declining share could, however, be related to the flight to safe assets (essentially, the global reserve currency) at a time of geopolitical uncertainty.

Figure 1: Share of payments via Swift by value (% of total)

Source: Bruegel based on Swift, Bloomberg, Natixis. Note: Data as of August 2023.

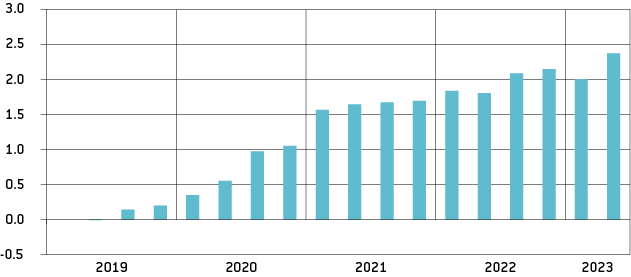

A broader definition of what it takes to become an international currency also includes use of the currency for investment and funding (both public and private). In these respects, the renminbi has become more international since the start of the COVID-19 pandemic (Figure 2, which shows a composite index of internationalisation developed by the People’s Bank of China

2

http://www.pbc.gov.cn/goutongjiaoliu/113456/113469/5114765/202310272017…

). The process of internationalisation of the renminbi was particularly strong in 2021, as the rest of the world battled with lockdown restrictions while China was relatively free of COVID-19.

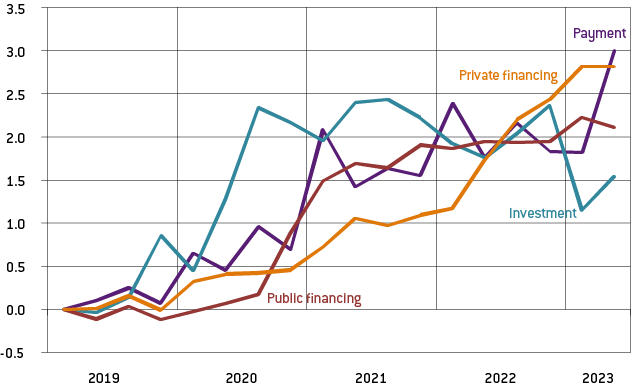

Even during the much tougher period from early 2022, as the Omicron variant reached China and zero-COVID-19 policies ravaged its economy, renminbi internationalisation continued, though at a much more moderate pace, even receding in the first quarter of 2023 as China opened up after the pandemic. In the second quarter of 2023, though, international use of the renminbi increased rapidly. The increase in the international use of the renminbi was quite balanced across the three functions captured by the index – payments, investment and funding – until recently. Since the end of 2022, investors seem to have lost interest in investing in renminbi, while use in trade and financing remains strong (Figure 3).

Figure 2: Renminbi internationalisation index (relative to Q1 2019)

Source: Natixis. Note: The index is composed of different indicators of cross-border use of the renminbi, including payments, investment and funding (see the appendix). Payments relates to trade settlements, and investment refers to demand for renminbi assets from foreign investors (whether private or public, such as central banks). Financing, from the host perspective, is borrowing in renminbi from private markets (loans from Chinese banks or issuing of renminbi-denominated bonds). Borrowing can also come from the People’s Bank of China, though a growing number of swap-lines; this is classified as official borrowing.

Figure 3: Renminbi internationalisation sub-indices (relative to Q1 2019)

Source: Natixis.

To gauge the different speeds at which the renminbi is internationalising across the different uses of an international currency, we conducted an empirical analysis of the determinants of the cross-border use of the renminbi (Amighini et al, 2023). The results show that economic factors are certainly relevant in explaining the increasing cross-border use of the renminbi, but these are not alone in driving the international demand for renminbi.

Trade and financial linkages with China are the main drivers of cross-border renminbi payments, but only for countries that participate in China’s Belt and Road Initiative (BRI). In particular, alongside trade transactions, receiving loans from China is found to explain to a significant degree bilateral renminbi cross-border transactions. For non-BRI countries, trade relations with China are not significant in explaining bilateral renminbi transactions. Similarly, the extension of renminbi-denominated bilateral swap lines (BSL) by the People’s Bank of China and the establishment of renminbi clearing houses abroad help explain the increased cross-border use of the renminbi. For non-BRI countries – in the main, developed economies – bilateral swap lines and loans are not significant in fostering the cross-border use of the renminbi. However, qualified foreign institutional investor (QFII) schemes

3

See http://www.csrc.gov.cn/csrc_en/c102049/common_list.shtml?channelid=9c00….

, which are granted by China’s financial regulator, and renminbi clearing centres do contribute to fostering the use of the renminbi among non-BRI members. In other words, the internationalisation of the renminbi does not appear to be a natural process only, but seems steered by economic policy choices.

In the next sections, we analyse China’s different attempts to internationalise its currency and how they have fared, with the aim of drawing out some lessons about what has worked best. From this, we highlight some policy considerations on the potential impact of renminbi internationalisation on the international monetary system and Europe.

2 China’s attempts to internationalise the renminbi

The Chinese government began a wide-ranging process to internationalise the renminbi in the wake of the 2008 global financial crisis. There were two reasons for this response.

- First, there was a sudden loss of confidence in the value of the US dollar, stemming from massive money creation done by the Federal Reserve to mitigate the consequences of the financial crisis on the US financial system and the economy as a whole. Having accumulated significant dollar reserves through large trade surpluses after accession to the World Trade Organisation in 2001, China became wary about the value of its foreign assets, especially since they were mostly concentrated in US Treasuries.

- Second, rapidly vanishing dollar liquidity in global financial markets prompted Chinese policymakers to look for alternatives, not only for China but also for other countries that might run short of foreign currency. None of the swap lines that the Fed extended in 2008 went to China, or even Hong Kong or Southeast Asia, with the exception of Singapore.

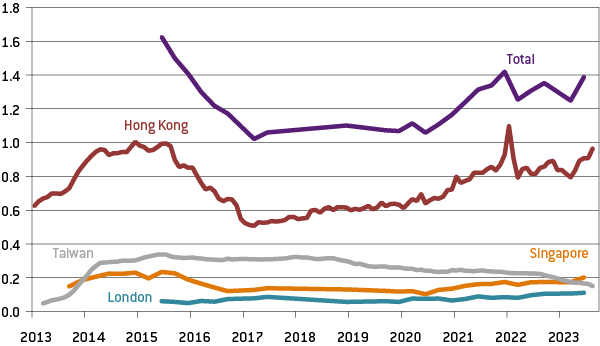

The first set of measures to promote the international use of the renminbi were policies allowing cross-border trade settlements in Shanghai and Guangdong in April 2009. Later, offshore renminbi centres were designated, starting with Hong Kong and followed by Singapore and London. Offshore renminbi-denominated deposits (so-called CNH to distinguish it from the onshore renminbi, the CNY) were allowed in these offshore centres. Because of these measures, CNH liabilities, mainly bank deposits, grew rapidly from 2010 to 2015 (Figure 4), especially since those offshore renminbi (CNH) could be used to enter the mainland at a time when there were tight capital controls on the entry of capital and an ever stronger renminbi

4

Offshore renminbi were allowed to enter the mainland through a quota called RQFII (renminbi-denominated qualified foreign institutional investor).

.

Figure 4: CNH deposits in major offshore centres (renminbi trillions)

Source: Bruegel based on PBoC, HKMA, CEIC, Natixis. Data as of August 2023.

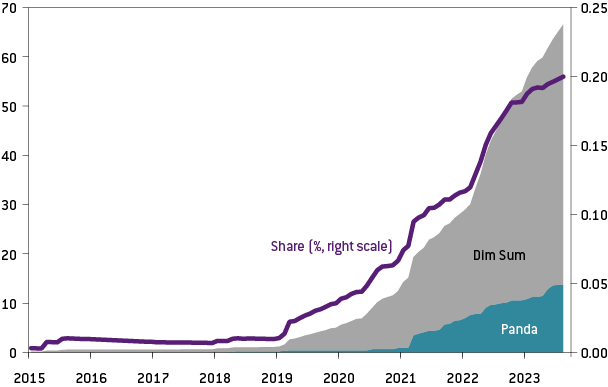

While CNH deposits kept on growing, peaking at 1 trillion renminbi ($145 billion) in December 2014, it became clear that it would be much harder to develop a set of CNH assets, whether loans or bonds. For the latter, a new market for renminbi-denominated bonds was created in Hong Kong, on which foreign companies or sovereigns could issue debt. This market, called the dim-sum bond market, has remained underdeveloped until recently (Figure 5). The loan market denominated in renminbi, meanwhile, has never really taken off. The tiny pool of CNH assets was one of the shortcomings of China’s first attempt to internationalise the currency, but was not the greatest obstacle. The 2015 stock market crisis and related renminbi devaluation led to the sharp reduction in CNH deposits in Hong Kong and, with it, a setback for the currency internationalisation process that the Chinese authorities had been fostering.

Figure 5: Outstanding renminbi bonds issued by non-residents as a share of global total bond issues ($ billions)

Source: Bruegel based on Bloomberg, Natixis. Data as of August 2023. Note: Panda bonds are renminbi-denominated bonds issued in China’s mainland by non-residents (sovereign, financial or non-financial institutions). Dim sum bonds are renminbi-denominated bonds issued in Hong Kong by institutions that are not resident on the mainland.

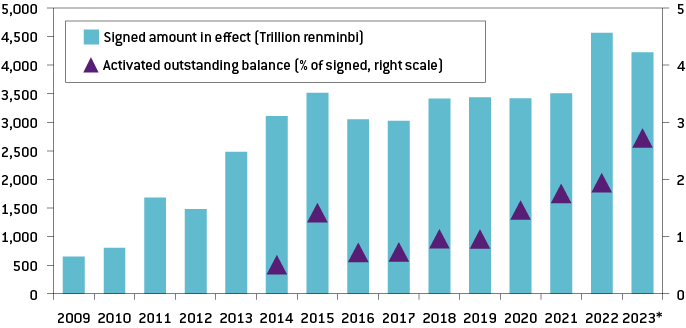

One way to solve the reduction in CNH deposits was for the People’s Bank of China to offer a pool of renminbi liquidity to other central banks through swap lines. That pool of liquidity was intended to respond to potential deposit withdrawals in offshore renminbi centres, which is why China signed its first bilateral swap line (BSL) with the Hong Kong Monetary Authority in 2009 (the first official offshore renminbi centre). Since then, the number of countries with BSLs has expanded to 40 (Figure 6).

Figure 6: People’s Bank of China bilateral swap lines with foreign central banks

Source: People’s Bank of China. Note: * Data as of H1 2023.

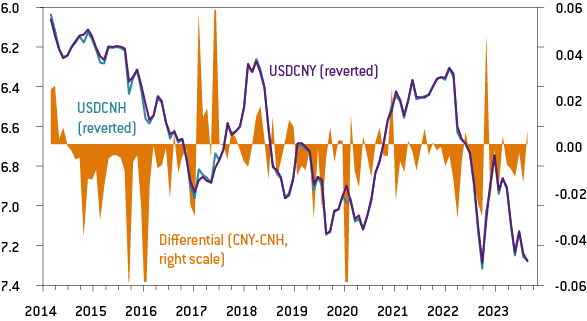

China’s stock market collapse in 2015 and the renminbi devaluation forced China to intervene in the offshore renminbi market to reduce the wedge between the offshore and onshore renminbi exchange at a time when the CNH was considered the best market signal of the future value of the renminbi (Figure 7). After huge capital flows and the loss of as much as $1 trillion in international reserves, China opted for the introduction of very stringent reserve requirements for CNH deposits (for the lack of a better option as the People’s Bank of China could not intervene in the CNH market). All of this meant that offshore renminbi liquidity was frozen. In other words, China decided to give up on the progress made in the cross-border use of the renminbi in favour of domestic financial stability.

Figure 7: Renminbi exchange rate

Source: Bloomberg, data as of September 2023.

Since then, the attempts to promote the international use of the renminbi have changed in nature. The next step was much more official: the entry of the renminbi into the International Monetary Fund’s Special Drawing Rights (SDR) basket, where it joined the dollar, the euro, the yen and sterling.

While this move was important symbolically, the SDR share of central banks’ foreign exchange reserves is quite small, and even more so the renminbi quota of just 10.9 percent of that basket. Most central banks managed to cover their renminbi needs to comply with the new SDR basket with the renminbi they already had in their reserves. This means that new demand for renminbi has so far has been limited.

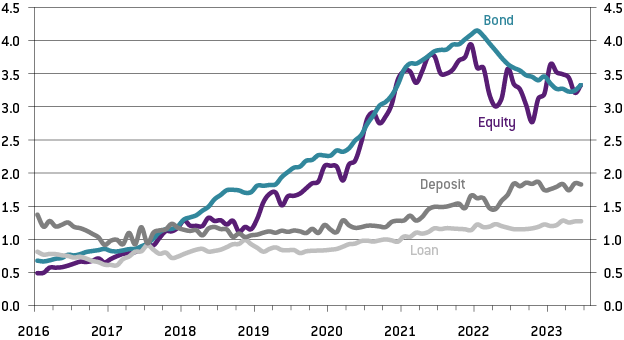

Another important step towards increasing the foreign demand for renminbi was to set up additional venues from which to invest in China’s financial market. In particular, the Hong Kong-Shanghai Stock Connect[5], which started operating in November 2014, aimed to bring foreign investors to China’s stock exchanges through the Hong Kong Stock Connect. A similar venue was created for foreign fixed-income investors in 2017, the so-called Stock and Bond Connects. Both are still at very low levels, even compared to Japan (3 percent to 4 percent of domestic renminbi assets for China compared to 9 percent 10 percent for Japan; García-Herrero and Ng, 2020). Furthermore, that share has fallen quite drastically, especially for bonds, since 2022 (Figure 8).

Figure 8: Foreign holdings of domestic renminbi assets (trillion renminbi)

Source: CEIC, data as of August 2023.

After Donald Trump won the US presidential election in 2016, an additional rationale for expanding the international use of the renminbi arose: diversifying away from dollar assets, and in particular US Treasuries, in light of the measures taken by Trump to contain China, starting with the trade war and followed by export controls on key technologies. Since Trump’s election defeat in 2020, the Biden Administration has continued with such containment and has weaponised the dollar by placing restrictions on its use even more than Trump (Eichengreen et al, 2022).

Against this backdrop, China’s dependence on the dollar, whether for trade or finance, has been identified by China’s leaders as a vulnerability. This is why the project of renminbi internationalisation, which had been set aside in favour of more urgent endeavours, has been revived again with a radically different strategy involving the use of China’s central bank digital currency (CBDC) beyond its borders. Chinese advancements in the realm of financial technology, together with the rapid adoption of mobile payment applications such as Alipay and WeChat Pay, are expected to facilitate the cross-border acceptance of China’s CBDC, thus profiting from a first-mover advantage.

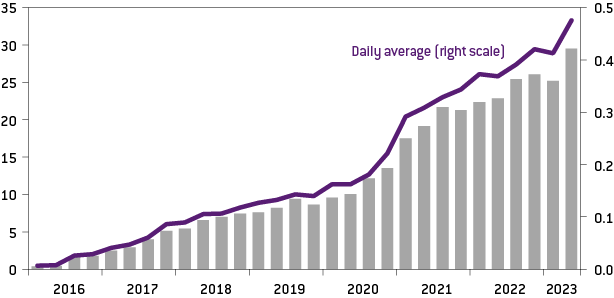

The digital renminbi has been designed, first, to replace the limited physical cash that remains in circulation within the Chinese mainland’s borders. But memorandums of understanding have been signed with several central banks, including the Hong Kong Monetary Authority (HKMA), the Bank of Thailand and the Central Bank of the United Arab Emirates, to foster the cross-border use of the digital renminbi in these jurisdictions. In addition, a joint venture has been set up with Swift, which indicates China’s aspiration of facilitating the global use of its new digital currency and, possibly, for the renminbi to become a reserve currency one day. Finally, the rapidly increasing use of China’s international payment system (Figure 9), especially since Russia’s invasion of Ukraine in February 2022, is also helping support the cross-border use of the renminbi.

Figure 9: Chinese international payments system, transaction value, trillion renminbi

Source: Bruegel based on People’s Bank of China, Wind; data as of Q2 2023.

The cross-border use of the digital renminbi suffered a setback from the collapse in movement of people across borders because of the COVID-19 pandemic. In particular, the massive number of Chinese visitors to other parts of the world were expected to have made use of the digital renminbi for international payments, starting with those countries where the People’s Bank of China has memorandums of understanding with central banks. The reality has been underwhelming, as the rollout of the digital renminbi has been much more limited than expected, even domestically.

3 The current push for internationalisation

A new momentum for the internationalisation of the renminbi has followed on from the Western response to Russia’s invasion of Ukraine. The renminbi has offered a route to escape such sanctions, most obviously for Russia, for which a large share of trade – as well as international reserves – is already denominated in renminbi. China has used the opportunity presented by Russia’s invasion of Ukraine to step up its efforts to foster the use of renminbi as an alternative currency for international payments, especially trade, and for private and official financing.

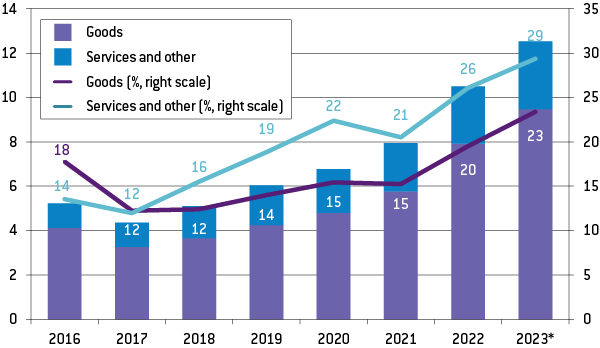

Starting with trade, China is pushing the use of renminbi to pay for its imports, on which it is advancing quite fast. Nearly 30 percent of services imports are already denominated in renminbi, while China’s trade in goods denominated in renminbi stands at 23 percent, according to China’s State Administration of Foreign Reserves (SAFE) (Figure 10).

Figure 10: Renminbi settlements and shares (renminbi trillions)

Source: Bruegel based on People’s Bank of China, SAFE, CEIC. Note: * Trailing 12 months as of June 2023.

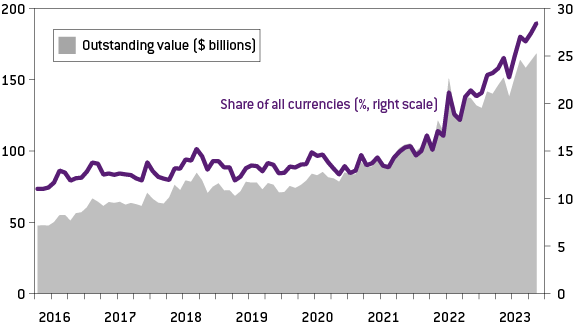

The latest phase of renminbi internationalisation has also benefited from elevated US interest rates since 2022. Given the higher costs of borrowing in dollars, many borrowers have turned to the renminbi for financing or refinancing, as shown by the sharp rise in the renminbi’s share of Chinese banks’ overseas loans and outstanding offshore bonds (Figure 11). Moreover, shocked by the Fed’s aggressive hikes and the continued tightening of dollar liquidity, the long-idle renminbi swap lines, which the People’s Bank of China had extended to the monetary authorities of 40 countries, have started to be withdrawn by those with dwindling foreign-exchange reserves (see Figure 3).

Figure 11: Overseas renminbi loans from Chinese financial institutions

Source: People’s Bank of China.

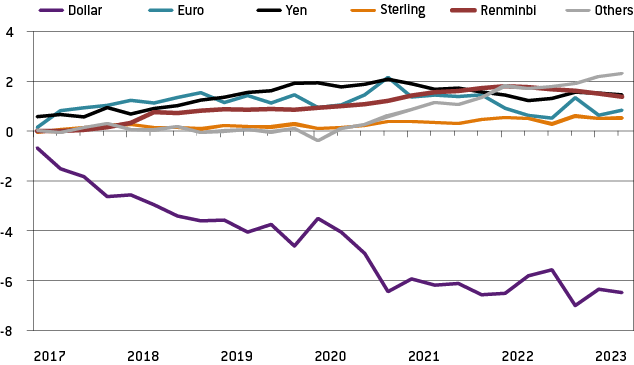

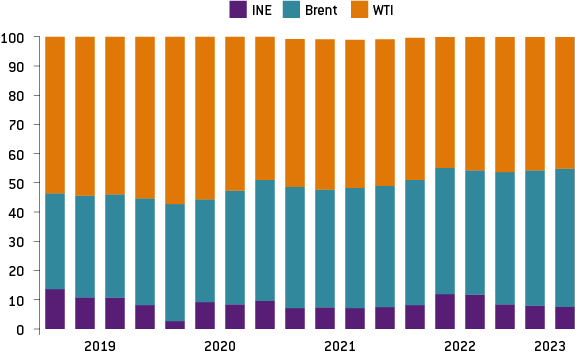

However, there are also areas in which the international use of renminbi remains stagnant or is even decreasing. This is mostly the case for investment, whether private or official (see Figures 12 and 8). However, there does not seem to be a significant increase in the share of oil transactions in renminbi (Figure 13), which is somewhat surprising as China is the world’s largest oil importer and has specific arrangements for renminbi settlements with major exporters (from Russia to Saudi Arabia).

Figure 12: Change in share of global allocated reserves (percentage points, relative to Q4 2016)

Source: IMF COFER. Data as of June 2023.

Figure 13: Shanghai INE crude futures turnover as % of global benchmarks

Source: Bruegel based on INE, ICE, NYMEX. Note: Shanghai INE is the Shanghai International Energy Exchange. WTI is West Texas Intermediate, the North American benchmark.

4 Implications for the rest of the world

Notwithstanding China’s multiple attempts to achieve renminbi internationalisation since the 2008 global financial crisis, global settlements in renminbi have remained underwhelming until recently. The fast increase in renminbi cross-border transactions started in 2022, after Russia’s invasion of Ukraine, for two main reasons. First, China has taken a more pragmatic approach towards renminbi internationalisation which relies on its trade and financing strengths, especially in relation to countries of the Global South. The second reason is the increase in restrictions put on use of the dollar by the US. More generally, a de-dollarisation narrative is now embedded in the new alliances that China has been pursuing, including the BRICS+ and the Belt and Road Initiative.

While the renminbi does not possess all of the key characteristics for a currency to become a global reserve currency, such as an open capital account, China is encouraging countries to create – or use – the necessary infrastructure to facilitate settlement in renminbi, from renminbi regional hubs to swap lines between the People’s Bank of China and other central banks. At a time when the renminbi is under severe depreciating pressure, notwithstanding the post-pandemic reopening of the Chinese economy, this strategy should be more effective than promoting the development of offshore renminbi centres, as was the case from 2010 to 2015, or the cross-border use of the digital renminbi at a time when the Chinese are travelling little overseas, at least compared to the pre-pandemic period.

Beyond the potential long-term race between the dollar and the renminbi, it is important to discuss how the renminbi may affect the role of the euro as the second most-traded currency after the dollar. First, it might be easier for China to overtake the euro than the dollar, since euro markets are not as liquid – or as integrated – as dollar markets. Furthermore, the contribution of the euro area to global growth is shrinking faster than that of the US economy. This is partly because use of the euro has been restricted as much as the dollar, given the coordinated response in terms of sanctions to Russia’s invasion of Ukraine. The very rapid fall in euro cross-border settlements based on Swift data (Figure 1) points to this possibility, although it is too early to tell.

Beyond the euro, the use of the renminbi to fund emerging economies, either through official funding such as bilateral swap lines, or renminbi-denominated lending, may have implications for the functioning of the international monetary system. This would be even more the case if China were to push an Asian Monetary Fund, as the Japanese government did after the Asian financial crisis, and Malaysia’s prime minister Anwar Ibrahim has proposed[6]. The renminbi could, over time, become the currency of reference for the Asian Monetary Fund, were it to be created.

References

Amighini, A., A. García-Herrero and H. Mu (2023) ‘What determines the international use of the RMB: economic versus institutional factors’, mimeo

Eichengreen, B., C. Macaire, A. Mehl, E. Monnet and A. Naef (2022) ‘Is Capital Account Convertibility Required for the Renminbi to Acquire Reserve Currency Status?’ CEPR Discussion Paper 17498, Centre for Economic Policy Research, available at https://cepr.org/publications/dp17498

García-Herrero, A. (2021) ‘Internationalisation of the RMB through its Digital Currency: Consequences for the Dollar and the Euro’, in S. Berman and E. Fabry (eds) Building Europe’s Strategic Autonomy Vis-À-Vis China, Institute Delors

García-Herrero, A. and G. Ng (2020) ‘Hong Kong: One Country, Two Systems, Three Challenges’, in A. Amighini (ed) Between Politics and Finance: Hong Kong’s ‘Infinity War’? ISPI

Appendix: Renminbi Internationalisation Index and its components

About the authors

Related content

China economic database

Repository of what we consider to be the most relevant macroeconomic data for China and EU-China relations.

China’s ‘new productive forces’ risk overcapacity bubble

India's economy can overtake China's if it can stay on track