Russian crude oil tracker

First published: 7 July 2022

Latest update: 12 February 2024

Comments to improve the coverage and the estimates are welcome. Please send your comments and any feedback to [email protected].

Data policy

This page provides a number of Bruegel datasets for public use. Users can freely use our data in its unchanged form or after any transformation for any purpose and can freely distribute it, provided that proper attribution is made to the source, but not in any way that suggests that Bruegel endorses the user or their use of the data. We will continually explore possibilities to improve data-quality.

The EU has placed embargoes on the import by sea of almost all Russian crude oil imports, and since 5 February, refined oil imports are also included. At the same time, the EU and G7 alliance, complemented by Norway, has introduced a price cap which domestic shipping and insurance services must respect when transporting Russian produce. Consequently, the trade of Russian oil is rapidly changing.

In this dataset we focus on crude oil (not including refined oil products) exports from Russia. We draw on a variety of sources to do so, beginning by decomposing pre-invasion crude oil exports in figure 1, and then providing monthly updates on how each export route is changing.

In 2021, Russia produced 540 million tonnes of crude oil, accounting for 13% of global production. Of this, 260 million tonnes were exported directly as crude oil, comprising 13% of global exports. Domestically, Russia refined the remaining 290 million tonnes of which 140 million tonnes were exported as refined products (11% of global refined exports) and 150 million tonnes were consumed domestically (BP). Figure 1 shows Russian average monthly crude oil exports in million tonnes for 2021.

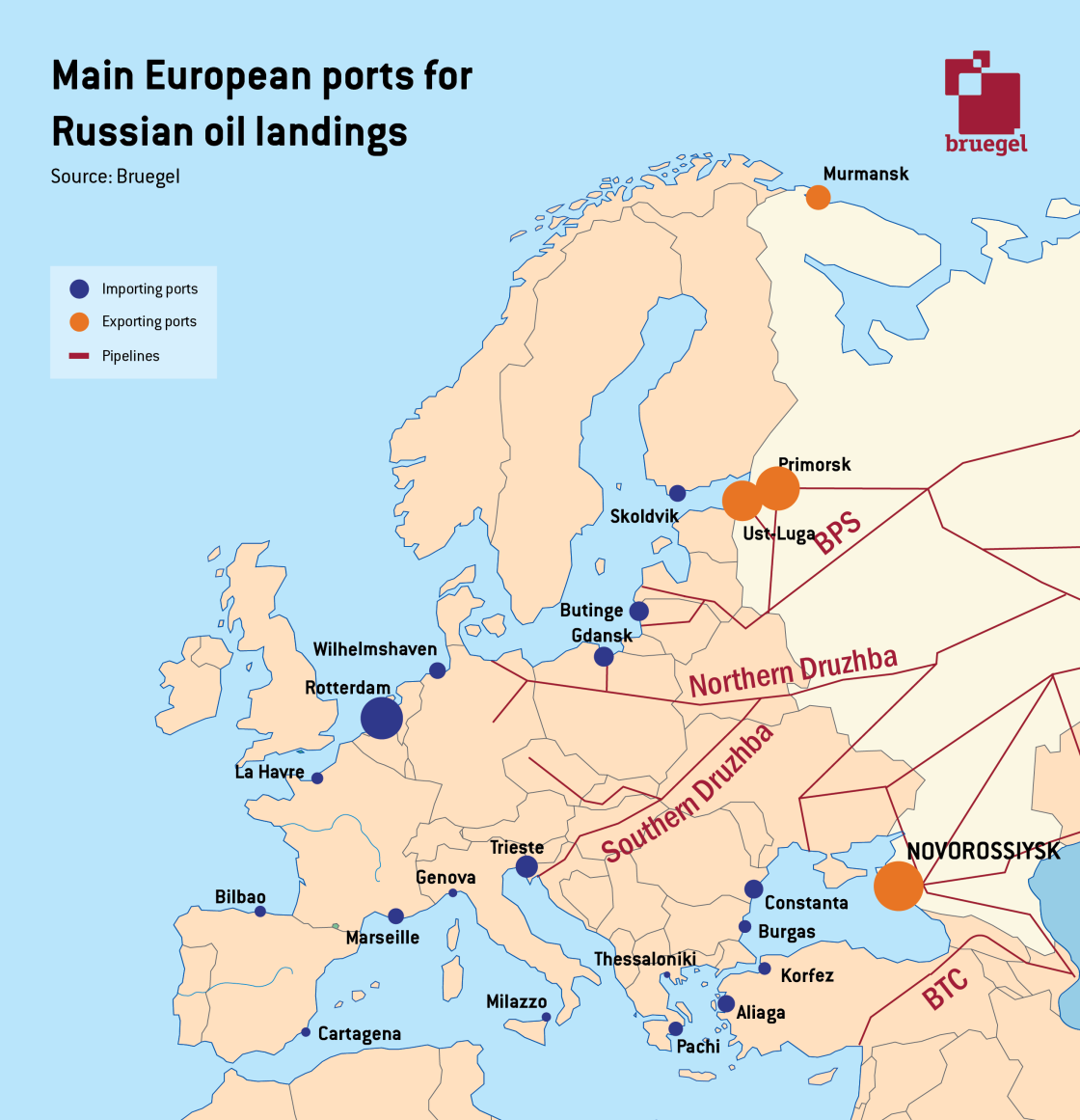

The two major routes for exporting crude oil are by pipeline and by oil tanker at sea. The Druzhba pipeline system carries oil to the EU, while the ESPO pipeline carries oil to China. Remaining Russian crude oil has historically been exported by sea to the EU, China, and other countries to a lesser extent.

Timely and publicly available data on Russian oil exports is insufficient (the best effort we are aware of comes from CREA who we build upon). Our aim is to help fill in the gap by providing clear and comprehensive information on recent export volumes and routes. We have compiled our data from multiple sources and validated numbers against external sources, and we believe the data allows for sensible interpretation of trends over time. In certain cases, we have consistently higher or lower estimate than other sources, which can be due to difficulties in identifying the exact cargo a ship is carrying (e.g., crude oil vs diesel) or the exact origin of oil (significant amounts of Kazakh origin crude oil leave from Russian ports). More detail is offered in a methodology section, and we welcome critical feedback.

Seaborne Exports

Historically, seaborne EU crude oil imports from Russia originated from Urals fields via western ports in the Baltic and Black Sea (see map at bottom). This is where the largest impacts of the embargoes and price caps are being felt. Eastern Siberian fields have historically served Asian customers, largely China.

We track oil leaving the four main Western Russian ports (Primorsk, Ust-Luga, Murmansk and Novorossiysk) and two main eastern ports (Kozmino and Prigorodnoye) using real-time vessel data to infer the amount and destination of exports.

Figure 2 shows 4-week moving average exports of Russian crude oil for 2021, 2022, and 2023. All oil leaving Russian ports is included, no matter the destination. Numbers are aggregated according to the departure date of the tankers.

Figure 3 shows an aggregation of monthly numbers by destination of imported Russian oil. Here, ships are aggregated according to arrival date of tankers (i.e., different from figure 2). EU countries are in various shades of blue (decomposed by region) and have largely ceased imports of Russian oil following the embargo. Ship-to-ship transfers are a part of the “undetermined” category.

Pipeline Exports

Russia also exports oil via the Druzhba pipelines, which have not been sanctioned at the EU level. The origin of this oil is also from the Urals fields serving western ports. Reductions in pipeline exports could be compensated by increasing crude oil loadings from these ports.

Figure 4 shows EU imports via this pipeline. From December, imports especially via the northern Druzhba branch (to DE and PL) are falling and can be expected to fall further in the first months of 2023 as Germany and Poland are in the process of ceasing purchases, while flows through the Southern branch (SK, CZ and AT) are expected to continue.

ESPO Pipeline

Eastern Siberian oil is also exported to China via pipeline. These flows have remained stable since the invasion, as shown by figure 5.

The Price Cap: Ship owners and insurance

Alongside the prohibition of Russian imports to the EU, the EU and G7 alliance (including Norway) has set a price cap of $60 per barrel of Russian crude oil. Companies from these jurisdictions are forbidden from providing shipping or insurance services to facilitate the trade of Russian oil unless the trade is verifiably below the price cap.

The functioning of the price cap depends on the volume of crude oil which is still carried or insured by EU and G7 companies. While there has been a slow decline as Russia has looked elsewhere to develop its own shipping and insurance services, the alliance is still involved in over 50% of ship departures from Russia implying a strong market power remains.

Figure 6 shows the proportion of ships by insurance country who have loaded with Russian oil in the respective month. Figure 7 shows the same for ship ownership. This data is taken from the CREA API, who extensively track ships departing Russia, and use external sources to validate ship ownership and country of insurance.

About the authors

Related content

European natural gas imports

This dataset aggregates daily data on European natural gas import flows and storage levels.

European natural gas demand tracker

The Letta report: an assessment of the energy proposals

The report has the potential to substantially impact the European Union's strategic agenda from 2024-29

Beyond the numbers of EU national energy and climate plans

The authors conduct a simple relative frequency analysis for a series of words mentioned in the NECPs to identify interesting policy insights within