The recovery in US housing

What’s at stake: While external factors and fiscal policy at the state, local and federal levels have now started to depress economic growth in the US, the housing market appears to have bottomed out and could become an important force to restore the economy to its normal level. Although construction employment remains sluggish, a series of important indicators point to a revival of the housing market, whose terrible performance acted until recently as a drag on the recovery.

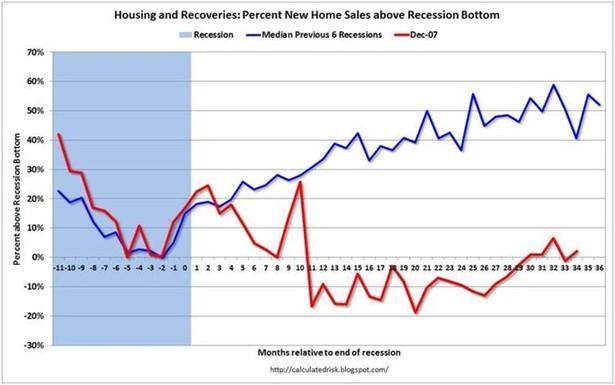

Not your father’s recession

The Oregon Office for Economic Analysis writes that during most recoveries housing has led the economic growth out of recession. Given the causes and consequences of the Great Recession, housing was, however, in no shape to do so in recent years. Bill McBride of Calculated Risk writes that this time was different as housing performed terribly – with a small increase due to the tax credit.

Indicators point to a bull market, but where are the construction jobs

James Hamilton points that Calculated Risk called the bottom to the decline in both house construction and prices last February, and sees considerable confirmation of that prediction since then:

1. Housing starts are increasing

2. Residential construction spending is up 17% from its low

3. New home sales are up 17% so far this year relative to the previous 18 months

4. Case-Shiller and Core Logic house price measures may have started to rise modestly.

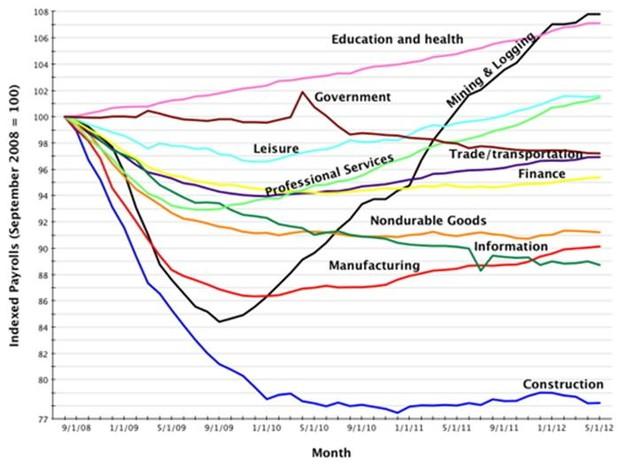

Dylan Mattews points that construction employment has, however, still not increased. Phil Izzo writes that the most widely reported construction numbers weren’t particularly encouraging (a small 2,000 monthly gain in June, that followed four months of moderate declines). This year, the effort to smooth out the figures was, however, complicated by the mild the winter. So even though there were declines in the spring, we saw increases in December and January. To get a look at the broader trend we can look at the monthly change from a year earlier. There we see that surge in December and January, but we also see that there has been consistent growth for 10 months — the longest sustained increase since 2006.

Bill McBride writes at Calculated Risk that the construction jobs will follow. For exactly the same reasons that construction employment didn't start falling until 2007 – and didn't collapse until 2008 although housing started collapsing in 2006. A part of this comes from the fact that many construction workers are paid in cash (illegal immigrants) and are thus not counted on the BLS payrolls.

The net effect of the housing recovery and the declines in manufacturing and external demand

Suzy Khimm writes in Ezra Klein’s Wonkblog that depending on which sector you’re looking at the data is showing either an economy in recovery, or one that is about to fall off another cliff.

The Oregon Office for Economic Analysis argues that there is a handoff that occurs from the manufacturing cycle, which has so far helped to drive the initial phase of the recovery, to housing, which will propel the economy in the near future. Bill McBride argues that the ISM index suggests some weakness now – mostly abroad – whereas housing suggests an ongoing sluggish recovery. The decline in the ISM index was partially driven by exports (no surprise given the problems in Europe and slowdown in China). However some of this export weakness will probably be offset by lower oil and gasoline prices. Housing, on the other hand, is usually a better leading indicator for the US economy than manufacturing.

James Hamilton writes that if autos were just to get back to 3% of GDP – a share exceeded in 94% of the quarters prior to 2005 – and housing to 4% – a share exceeded 87% of the time prior to 2005 – that could add another 2% to GDP right there. If the economy were growing at a 3% annual rate, and housing and autos were doing the same, their contribution to the annual growth rate would only be 0.24 percentage points. But the key point is that housing and autos hardly ever grow at the same rate as everything else. As housing dropped from about 6-1/4% of GDP at the top of the housing boom in 2005 to its value around 2-1/4% today, it took about 4% away from the level of real GDP. In the first year of the current recovery, autos and housing contributed a mere 0.17 percentage point to the 3.3% real GDP growth rate. In the 3 years since the recovery began, autos and housing contributed 0.24 percentage points to the meager 2.4% annual GDP growth rate. But the historical shares illustrate that we could still expect much more from these sectors.

Tim Duy expects overall growth to remain subdued, despite a rebound in residential construction. The latter is helpful and important, but not by itself a magic bullet. The housing bubble was less about a construction bubble, and more about a price bubble, which fueled spending activity via mortgage equity withdrawal.

Jan Hatzius writes that there are too many headwinds for the US economy to reach a satisfactory pace of recovery anytime soon. While the private sector is gradually healing the balance sheet damage incurred during the housing boom and bust, this healing process is inherently slow and subject to reversal. Fiscal policy has also been a net drag over the past two years, especially at the state and local level but now increasingly at the federal level as well. Finally, we have seen some clearer negative spillovers from the European crisis and the slowdown in Asia on US manufacturing, as the new export orders index in the ISM dropped sharply. Real Time Economics points that the service sector is slowing according to the ISM’s nonmanufacturing index, which fell from 53.7 in May to 52.1 in June.

Note to our readers: the blogs review will continue to be published on Mondays over the summer.

About the authors

Related content

The Fed’s rethinking of normality

What’s at stake: As we approach Jackson Hole, monetary policymakers are considering how to redesign monetary policy strategies to better cope with a l

The fiscal stance puzzle

What’s at stake: In a low r-star environment, fiscal policy should be accommodative at the global level. Instead, even in countries with current accou

Racial prejudice in police use of force

What’s at stake: This week was dominated by a new study by Roland Fryer exploring racial differences in police use of force. His counterintuitive resu

Global supply chains: lessons from a decade of disruption

This paper revisits the effects of three shocks on the functioning of global supply chains.