Europe’s China problem: investment screening and state aid

China’s state capitalist economy poses a challenge to EU openness to foreign investment. In response, the European Commission 17 June published a Whit

As the Chinese share of global GDP grows, so have concerns about its use of subsidies to facilitate acquisitions. These concerns relate to the use of investment as a political tool, through the acquisition of strategically relevant companies and technologies, and the use of state aid to gain competitive advantages in European markets. Since World Trade Organisation (WTO) rules have failed to provide protection against foreign state aid, the EU is developing its own unilateral tools. This is the context behind the European Commission White Paper on levelling the playing field with regard to state aid that the European Commission published 17 June. The paper does not mention China explicitly, concerns over Chinese subsidies and state-owned enterprises (SOEs) are evident when reading in between the lines.

Given the challenge posed by state aid in global markets, we think that the European Commission’s White Paper is a welcomed and measured proposal to ensure a level the playing field in the European market. A reform of the way the WTO deals with subsidies would be the best solution for this problem, but as WTO reform is stalling and the multilateral trading system is in crisis, the EU needs to develop unilateral instruments to prevent distortion in its own markets. At the same time, the EU has long been engaged in negotiations on a comprehensive bilateral investment treaty with China, with very little progress. We look at both the geographical breakdown of foreign direct investment (FDI) into the EU as well as projections of the performance of global direct investment flows for this year. Prospects for the latter are particularly poor, with FDI expected to fall between 30 and 40 percent in 2020. At the same time, Chinese investors currently control only a very small fraction of European companies. We thus argue that concerns over large market distortions caused by Chinese investment are unjustified.

Overblown worries from an economic point of view

Before discussing the main proposals contained in the Commission’s White Paper, it is worth briefly assessing the actual challenge posed by foreign investment into the EU from non-market economies and state-owned enterprises (SOEs). The geographical origin of acquisition plays an important role here: while investment ties with the US and Canada are less controversial, Chinese acquisitions receive greater public scrutiny.

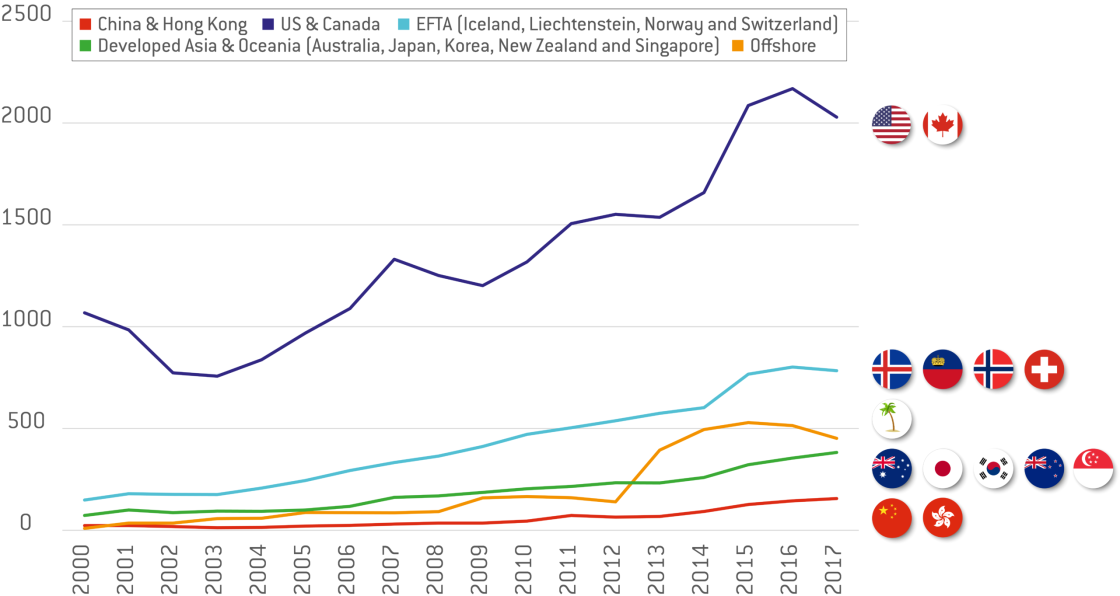

Figure 1: FDI stocks into the EU (including the UK), € billions

Source: European Commission Finflows database (updated version). Notes: Developed Asia and Oceania includes Australia, Japan, Korea, New Zealand and Singapore.

Figure 1 illustrates the overblown nature of the concerns over the Chinese presence at the macro level. It shows the stock of FDI into the EU, which includes mergers and acquisitions (i.e. investments that allow a foreign player to take active control of an existing company). While the stock of FDI from China and Hong Kong has grown substantially since 2000, to around €150 billion in stocks in 2017, it still represents less than 8 percent of that from the US and Canada (which stood at over €2 trillion). Chinese stocks are also less significant than FDI stocks from all other major sources of origin, exhibited in the graph. The European Commission estimates that investors from China, Hong Kong and Macao control only 1.6 percent of assets in EU-based companies. Even as there has been a significant increase from 0.2 percent in 2007, it remains very small. Indeed, at the height of the euro-crisis, when fear of Chinese buy-outs was rife, their presence in Figure 1 is barely perceptible.

SOEs are playing an increasingly significant role in foreign mergers and acquisitions, with almost 400 European companies having been acquired by foreign SOEs since 2007. However, a third of transactions involved SOEs originating in EFTA countries (chiefly Norway and Switzerland), while only 60 of them involved SOEs in China, Hong Kong and Macao (for a discussion of this see Claeys et al 2020 pg 64).

Moreover, the Chinese current account and exchange rate position has recently become far less conducive to large international investments. The size of Chinese investment abroad is defined by the overall depth of capital flows (eg foreign investors buying Chinese assets and Chinese investors using the revenue to invest abroad), and by the current account surplus (where a trade surplus is invested abroad). In 2007, the Chinese current account surplus grazed 10 percent, resulting in a large net capital outflow. However, despite the large surplus at that time, due to the limited nature of investment relations, the overall level of Chinese FDI in the EU remained very small.

Since then, Chinese capital controls have been substantially tightened to prevent large scale outflows of private capital, after the 2015 devaluation of the renminbi triggered an important episode of capital flight. In 2018 and 2019, the current account has remained under 1 percent and could even become negative. Since 2016, Chinese investment into the EU has been declining: in 2019 FDI stood at only €11.3 billion, 33 percent smaller than 2018 and 69 percent smaller than its peak in 2016. Finally, forecast for 2020 predict a collapse in direct investments globally and into the EU specifically. UNCTAD projects that global FDI flows will fall by 40 percent in 2020, bringing these below $1 trillion for the first time since 2005. Among developed countries, Europe is expected to see a greater fall (30-45 percent) than North America (20-35 percent) because of the more fragile condition in which the EU entered the crisis. The OECD similarly expects global flows to fall by 30 percent.

A key political question

Even though the evidence above does not support concerns over excessive exposure to Chinese investment from a purely economic point of view, the questions of how to ensure a level playing field when one of the largest economies in the world is a non-market economy is high on the political agenda. The introduction of a new system of FDI screening was in fact mentioned as a priority in the mission letter to Trade Commissioner Phil Hogan. Under the previous Commission, the investment screening regulation was introduced, targeting foreign investments that could “affect security or public order”. In March 2019, as the COVID-19 crisis hit European economies and lead to the perception of “economic vulnerability”, the Commission issued investment screening guidance to member states, a few days after the trough in the European stock market (EUROSTOXX). The purpose of these guidelines was to urge member states to make full use of screening mechanisms (and set them up if absent) to protect strategic industries, namely healthcare. A number of European countries have expanded their investment screening procedures during this crisis, including Spain, Italy, France and Germany. Poland is in the process of introducing such legislation.

The Commission’s 17 June White paper on levelling the playing field as regards foreign subsidies takes a pronouncedly different approach and is a complement to these investment screening efforts. It addresses the issue of foreign state aid for acquisitions based on the effects on competition and the level playing field within the single market. The paper explores the regulatory loopholes that exist, which result in inadequate protection against foreign subsidies and their distortive effect. These often lie outside the scope of EU competition policy and are imperfectly addressed by current investment protection measures (conceived to protect strategic industries). The WTO Agreement on Subsidies and Countervailing Measures (ASCM) is generally perceived as ineffective in addressing the problem of state aid, and only concerns trade, not investments.

With regards to investment, ‘Module 2’ of the Commission’s proposal addresses precisely foreign acquisitions of entities within the EU, facilitated by non-EU subsidies. The Commission endorses the option of ex-ante acquisition screening, focusing on those transactions that allow foreign entities to take direct or indirect control of an EU entity, acquisitions where the parent company notifies having received prior subsidies or expect to do. This would allow the competition authority that is responsible for the screening to block the acquisition in question or request remedies.

This approach seems measured and the policies proposed offer ample benefits. Indeed, maintaining fair competition in the single market likely warrants a certain degree of screening. It is further particularly positive that this is considered as a separate issue to the FDI Screening Regulation, which looks to protect investments likely to affect security or public order. Using the FDI Screening Regulation to prevent single market distortions could lead to its indiscriminate and regular application and would be wholly counterproductive.

However, the Commission should avoid introducing excessively cumbersome or restrictive processes, in the implementation of such screening, that disincentivise investment into Europe. Furthermore, one of the problems of the WTO ASCM is that it’s definition of subsidies does not cover benefits received from SOEs. The identification of benefits and subsidies provided to Chinese companies through the opaque system of SOEs and state-controlled banks is not straight forward, and the Commission white paper largely fails to address this issue. Further clarification is necessary.

Conclusion

Compared to transatlantic capital flows, EU-China flows are still very small. Unlike at the height of the financial crisis when the Chinese current account surplus neared 10 percent, China now enjoys a surplus of less than 1 percent and could be nearing deficit, thus heavily reducing its net capital outflow. Given the continued weaknesses and closed nature of Chinese capital markets this is unlikely to change anytime soon. As the Chinese government purses a more consumption-based growth model, large increases in the current account surplus are highly unlikely. We argue therefore that the current overall level of Chinese investment gives no reason for concern.

However, the use of FDI to buy political influence in smaller member states through Belt and Road Initiative funds or the “17+1 group” (a group formed by 17 Eastern European countries and China), on the other hand, can be highly problematic for the EU. However, the investment screening regulation does not remedy this problem, especially as the screening is currently carried out by the same member states these investments try to influence (the European Commission can issue an opinion when public order or security in more than one country is affected, but its opinions are non-binding). This problem requires a political solution, not a regulatory one.

It is important to separate this issue (and investment protection in strategic sectors) from the preservation of single market integrity and competition in the face of foreign state aid. The question of how to level the playing field with regards to state aid is more pressing than ever. Developed economies, with the EU at the forefront, are using state aid at an unprecedented scale in their response to COVID-19, while it is becoming increasingly clear that the progress made in reforming Chinese state capitalism is now being back-tracked. The new white paper rightly focuses on this issue. Making progress on the bilateral investment treaty with China would be very useful as well, as it could introduce rules to safeguard investments and improve market access, but the failure of the June 22 EU-China Summit (which did not even reach a joint declaration) is not encouraging. With global trade and capital flows collapsing, the priority should be to preserve competitive markets, not to close them to foreign investment.

Recommended citation

Poitiers, N., M. Domínguez-Jiménez (2020), ‘Europe’s China problem: investment screening and state aid’, Bruegel Blog, 02 July, available at https://bruegel.org/2020/07/europes-china-problem-investment-screening-…

About the authors

Related content

China economic database

Repository of what we consider to be the most relevant macroeconomic data for China and EU-China relations.

The post-election Taiwanese economy: decisions ahead and takeaways for the European Union

The EU should try to attract more business from Taiwan, though Taiwan’s January 2024 election has not made the job easier

Global supply chains: lessons from a decade of disruption

This paper revisits the effects of three shocks on the functioning of global supply chains.

Knowledge spillovers and geopolitical challenges in global supply chains

Our main message is that policies restricting knowledge flows should be limited to narrowly defined areas of strategic importance.