Cryptoeconomics – the opportunities and challenges of blockchain

While the activities using the peer-to-peer cryptocurrency Bitcoin swing between legal and illegal, the attention has been increasingly shifting to th

What is blockchain?

The Economist explains that in order to understand how blockchain works, first we need to distinguish between three things: the bitcoin, the cryptocurrency, the specific blockchain underlying it and blockchains in general. Bitcoin is the largest, most known project that uses this technology, but numerous other large cryptocurrencies are emerging based on blockchain. Blockchain is a trusted public ledger without single user control or centralized authority, where the participants themselves collectively keep track of the system. Bitcoin’s blockchain, for instance, keeps track of the transactions continuously and prevents double-spending.

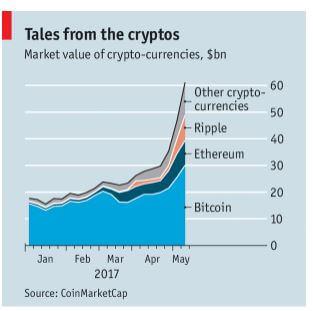

Source: The Economist.

Christian Catalini explains on the MIT blog that blockchain, like the internet in its early years, is hard to understand and predict. In a blockchain, transactions are recorded chronologically and form a “block” which can be data of many types- currency, digital rights, identity, property titles to name a few and these data are then formed into “chains” and distributed across many participants in the network. Increasingly, the attention is shifting from Bitcoin to Blockchain and it’s not solely about the use of the digital currency anymore, but rather what other applications blockchain technology could create in the future.

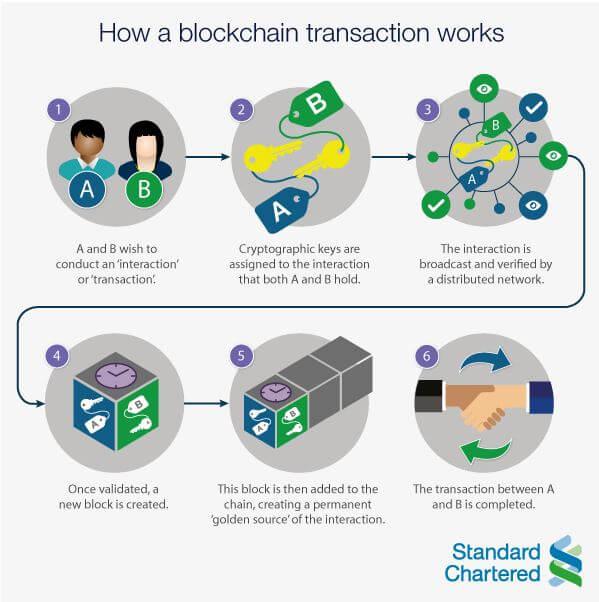

Source: Standard Chartered.

Why use blockchain?

Christian Catalini finds two types of costs that blockchain can reduce for business - the cost of verification and the cost of networking. Businesses and organizations engage in many types of transactions and verifications that demand some kind of review of credentials and verifications, these and related audit processes can be costly and labour intensive. Blockchain, instead has recorded all these attributes and when the need for verification arises, you can do them without incurring any cost. There will be no need for Paypal or audits to verify information anymore. Blockchain can reduce costs of running a secure network. Even though the sharing economy created a more distributed exchange of goods and services and gave rise to Airbnb and Uber, these platforms are still intermediaries. Using blockchain technology can be a step closer to a radical re-think of the way we conduct business and engage in competition. Blockchain as a general purpose technology could have many applications in various industries, such as banking, finance, money transfer, microfinance, identity and privacy, ownership and internet of things, robotics and artificial intelligence. However, he says, like internet at earlier stages, the blockchain’s potential will unfold over many years. But in some industries, such as finance, the disruption might come sooner than the other industries.

These disruptions already seem to be taking hold. A Financial Times report states that IBM has been hired by seven European banks to create a blockchain system for small and medium-sized companies (SMEs) to access cross border trade finance. The plan for the banks is to start offering trade finance to SMEs through the system. The platform will further add banks, shippers, freight forwarders and shippers and allow SMEs to track orders, make payments and record deliveries.

Case and Wong from Harvard Business Review write that the fundamental advantage of the blockchain system is that it resolves problems of disclosure and accountability between individuals and organizations whose interests might not be the same. Mutually important data is recorded in real time without a single entity organizing and controlling this process. So far a lot of discussion on the application of the blockchain technology has been centered around the financial sector, but it could also be a potential test case for global value chain systems. Use of blockchain technology in supply chains could be realized through chip and sensor technologies that could translate data from automated movements of physical goods. For instance, the Everledger start-up has uploaded unique data on a million individual diamonds to a blockchain ledger in order to build a verification system and help jewelers comply with regulations against “blood diamonds”. The main obstacle with the blockchain technology is its governance challenge. Inevitably, the issue of private, closed ledgers run by a consortium of companies will arise. Therefore, it is crucial to design blockchain applications that ensure free access, competition and open innovation in public blockchains with no single entity controlling it.

Why think twice?

Ceccheti and Schoenholtz write that the interest in the blockchain technology is still in its infancy and has not extended much beyond banks and other financial institutions. Public networks of distributed record keeping like blockchain can be very beneficial where there is a lack of private sector involvement or where competition is scarce at the moment, such as reaching out to the poorest in our societies and meeting their needs to borrow, make payments and save. But the authors remain sceptical that blockchain could compete against big clearinghouses that dominate wholesale payments and settlements. Today’s wholesale payment systems and electronic trading platforms are much safer, more efficient and cheaper and most importantly they exploit the economies of scale. Whereas blockchain’s advocacy of eliminating the “third party” could sacrifice the economies of scale that third-party clearinghouses generate. Nevertheless, the authors point out that surely the current system has not reached its technological plateau and the burden of proof lies with the innovators.

Izabella Kaminska of the FTAlphaville writes that at heart of the problem, as always, lies the governance challenge, namely who dictates and enforces the rules as well as who do we hold accountable when things go wrong. What the techies are failing to understand is that the public wants to place trust in the institutions operating the “conventional” platforms, especially when they are operated by real people, so that they could be held accountable. For instance, Airbnb was built on a notion that people organize and arrange themselves, but soon enough the trust issues emerged - bad consumer experience, fraud, vandalism etc. Soon Airbnb found itself transformed from a tech company and a platform to rules and standard authority. As long as blockchain’s governance challenges are not thought through, blockchain’s truly transformative potential will fail to be realised.

According to John Cochrane, traditional cash has the useful property of having no memory. The economy does not need a memory of every transaction, which is something that blockchain will create. Moreover, the current set-up of banks and financial institutions providing transaction services to people allows for competition and innovation and is better able to provide privacy and anonymity in transactions.

The way ahead

Philip Boucher’s analysis suggests that since middlemen will be displaced by blockchain the intermediaries will need some kind of regulation. These alternative regulation levers need to be placed to ensure the capacity for effective action and that parties uphold the law. He gives four options that governance institutions could use to respond to the challenges that blockchain will create:

Option 1: No use of blockchain at all. If citizens’ desires to use blockchain as a way to demand more transparency, government institutions could grant more access to government data without using blockchain at all.

Option 2: Actively support the private sector in their development of blockchain technologies, for instance recognizing to some extent the legitimacy of certain transactions and records.

Option 3: Reverse of Option 2, that is refuse to grant legitimacy to contracts and transactions developed by private actors using blockchain.

Option 4: Adopt permissioned blockchain by maintaining the role and power of middlemen and provide basic functionality without offering full decentralization. This model is already observed in UK and Estonia in their public sector use of blockchains and in some private sectors.

He concludes that in the coming decades various combinations of these four options will be employed, but for the time being there is little effort to intervene at the European level.

About the authors

Related content

Reconciling contradictory forces: financial inclusion of refugees and know-your-customer regulations

The authors contributed to the new issue of the 'Journal of Banking Regulation' with a paper on financial inclusion initiatives and banking regulation

South Korea's semiconductor strategy

Economic ties are being reshaped by the semiconductor industry's evolution

Financial literacy and inclusive growth in the European Union

Financial literacy is financial education, such as basic economics, statistics and numeracy skills combined with the ability to employ these skills in

People on the move: migration and mobility in the European Union

Migration is one of the most divisive policy topics in today’s Europe. In this publication, the authors assess the immigration challenge that the EU f