Spain: a tale of two crises

In March, Jean Pisani-Ferry and I documented a significant capital flight affecting the euro-area periphery. The flight started in Greece, spilled over to the other programme countries and eventually reached Italy and Spain during summer 2011. The latest data shows that the situation is becoming extremely serious in Spain, where capital outflows since April 2011, when the acute phase of the crisis started, have reached 30% of pre-crisis GDP.

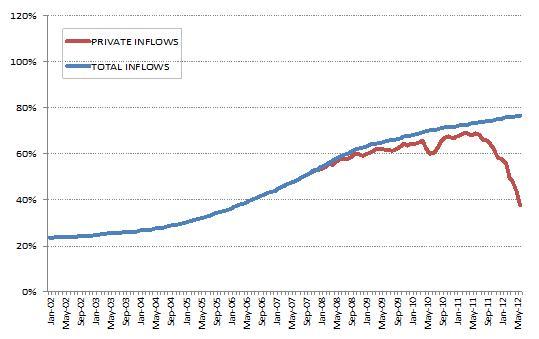

Figure 1 – Cumulative capital inflows (% 2007 GDP)

Note: data from national authorities. Capital flows are cumulated on the 2001 international investment liabilities

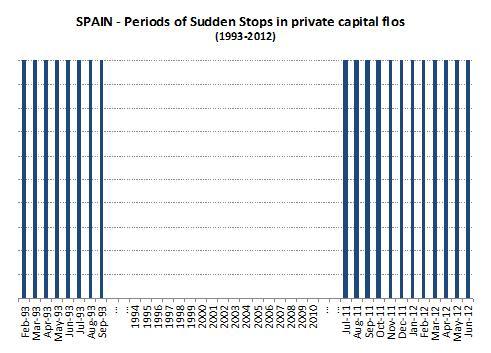

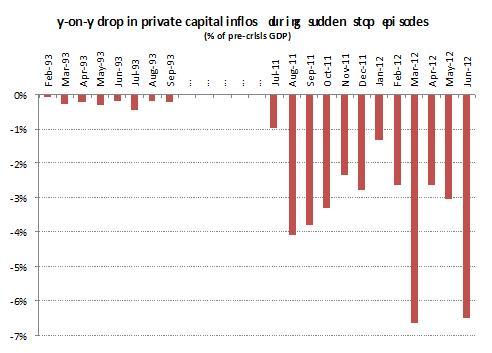

This is not the first time that Spain has experienced a sudden stop, and looking at capital flights in an historical perspective is enlightening. Applying the methodology generally used for the formal test of sudden stops[1] to monthly financial accounts data for 1990-2012, I can identify an earlier sudden-stop episode during the Exchange Rate Mechanism (ERM) crisis of 1992-1993[2]. Figure 2 compares this with the current episode, in terms of duration and size of capital outflows.

Figure 2a – duration of sudden stops

Figure 2b – magnitude of sudden stop

Note: own calculation on data from national sources. Pre-crisis GDP is 1991 for the first sudden stop episode and 2007 for the second one.

The size of the capital outflow experienced by Spain since July 2011 is unprecedented. During the 1993 sudden-stop phase, monthly capital outflows[3] amounted on average to 0.24% of pre-crisis GDP, whereas during the 2011 episode the corresponding figure reached 3.3%, showing how devastating the loss of investors’ confidence can be in a world of perfect financial integration and no capital controls[4].

The difference in terms of duration is no less striking. During the ERM crisis, Spain went through several tense moments. First it had to devalue by 5% on “Black Wednesday” (16 September 1992), following the abandonment of the ERM by Italy and the UK. A second 6% devaluation took place after the Swedish Riksbank decided to float the Krona, on 19 November 1992. Lastly, the peseta came under the strongest pressure in early 1993. In April 1993 the currency was quoted at its lowest level since Spain entered the ERM, forcing a third devaluation by 6.5% in May[5] (Buiter et al, 1998). Overall, the sudden stop of 1993 lasted eight months. The episode that started in July 2011 has been going on for 12 months already, and recent data shows no sign that the pace of capital outflow is abating.

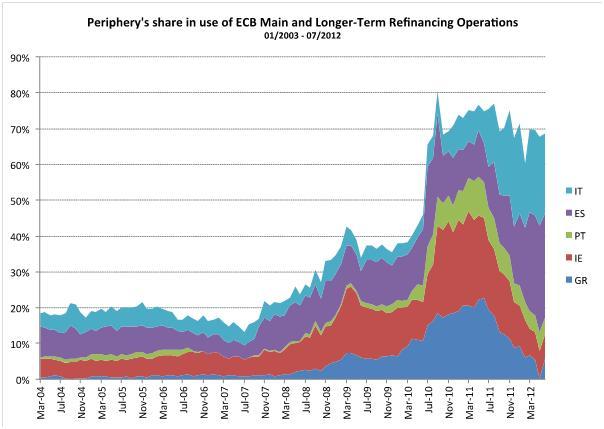

Figure 3 – Eurosystem Liquidity

Note: data from national sources

Unlike 1993, Spain has access this time to a powerful absorption mechanism: Eurosystem liquidity provision, on which Spanish banks have become increasingly reliant during 2011/12 (Figure 3). As of July 2012, the Spanish banking system had borrowed via main and longer-term refinancing operations as much as €402 billion, i.e. about 30% of total Eurosystem liquidity provision. This is mirrored in the steady deterioration of the – by now famous – TARGET2 balance.

The long denial and the disorganised management of the problems in the banking system, the overshooting of central government fiscal targets and the lack of clarity and transparency about the fiscal positions of the regions, led to a loss of trust in Spain on the part of private investors. As a consequence, private capital is fleeing and the country is becoming more and more dependent on Eurosystem support. Unlike foreign exchange reserves in 1993, the compensating function of TARGET2 balances is virtually unlimited. But it does not mean that this precarious equilibrium will remain stable. After the European Central Bank decisions of 6 September, the Spanish bond market seems to be experiencing some relief. This should not lead to the gravity of the overall situation being overlooked. Stopping the confidence crisis is crucial, and addressing the underlying causes of investors’ mistrust is essential for private capital to return. Allowing the absorption power of the ECB to work in full – including with the new OMTs – may help. The impact of the announcement effect has been positive, but stems from market expectations, and as such might be short-lived. The OMT is necessarily conditional to a request for help being made. Without Spain making the first move, the ECB cannot act. The relief on the Spanish yields is therefore a sign that investors expect Spain to recognise the unsustainability of the present situation, and to make use of all the instruments at its disposal (once the conditions attached to them are clarified).

[1] Described in Calvo et al (2004). I apply the same criteria as in Merler and Pisani-Ferry (2012) and consider only episodes that lasted for longer than 3 months.

[2] Consistently with Calvo et al (2004), who also identify a sudden stop for Spain during the ERM crisis in 1992-93.

[3] Measured as the change in capital flows with respect to the same month of the previous year

[4] Capital controls were abolished in February 1992, but they were reintroduced temporarily in September 1992 and definitely abolished at the end of 1992. This was compatible with the Single Market legislation that allowed countries to use temporarily capital controls in order to deal with disorderly exchange rate markets – see Buiter et al (1998)

[5] This is the episode identified in figure 2. Unfortunately we cannot investigate the existence of sudden stops in 1992 due to data limitations (the way the test for sudden stop is constructed implies that the first 3 years of observations are lost).

About the authors

Related content

Is the current crisis management framework enough for the age of digital bank runs?

Fast and furious: how digital bank runs challenge the banking-crisis rulebook

The speed of recent bank failures has shown the need for more systemic protection of the financial system.

How Europe can sustain Russia sanctions

Russia's war in Ukraine has underscored the need for Europe finally to invest more in its own defence and security. Such an outrageous act of aggressi

The microeconomics of Christmas

Review of major contributions to the literature on the controversial topic of the deadweight loss of Christmas.