Sovereign bond holdings in the euro area - the impact of QE

Since the announcement of the QE programme by the European Central Bank (ECB) on 22 January 2015, national central banks have been buying government a

The share of domestic government bonds held by national central banks has increased, as expected, but this has coincided with only a limited decrease in holdings by domestic banks, which had increased significantly during the crisis (see here).

As of the end of April 2016, the ECB had bought 732.8 billion euros of bonds under its public sector purchase program (PSPP), of which 87.7 billion were supranational bonds and 645.1 billion were national government and agency bonds. Purchases of asset-backed securities reached 19 billion euros at the end of April, while holdings under the third covered bond purchase programme (CBPP3) amounted to 172.3 billion euros (see here for breakdowns). Starting in June 2016, the ECB will also add a corporate sector purchase programme (CSPP).

After the recent expansion of the QE programme to 80 billion euros per month, the breakdown of monthly purchases is more flexible and no longer clear ex ante. We can still get an idea of how monthly purchases are distributed by looking at the composition of purchases carried out in April 2016, the first month after the announcement of the expansion of the asset purchase programme.

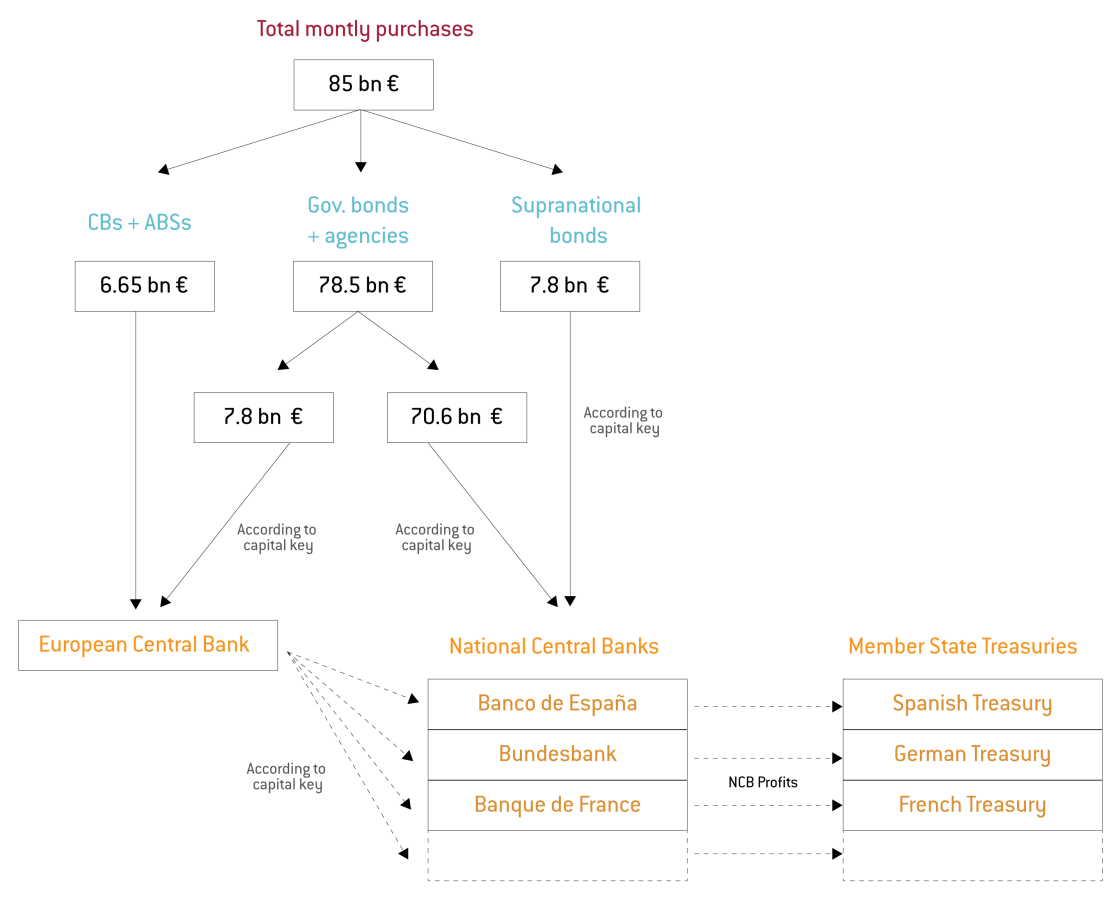

In April 2016 the purchases under the asset purchase programme amounted to 85 billion euros. Of these, 50 million euros (0.06% of the total) were under the asset-backed security purchase programme, 6.6 billion euros (7.8%) were under the covered bond purchase programme and 78.5 billion euros (92.2%) were under the public sector purchase programme. We also know that the share of supranational securities bought under the PSPP has been reduced from 12% to 10% of monthly purchases, so we can infer that supranational securities accounted for about 7.8 billion euros out of the 78 billion of PSPP in April 2016 (Figure 1).

The distribution of purchases conducted in April 2016 are more tilted towards the public sector, compared to the average distribution of the pre-existing stock. This is probably going to be transitory, as the ECB will soon start buying corporate securities.

Figure 1: Implementation of purchases as of April 2016

Source: Bruegel

Note: the share of supranational holdings (which are under full risk sharing) was lowered from 12% to 10%, so the ECB’s share of the other PSPP purchases has been increased from 8% to 10%, in order to keep the risk-shared part of the PSPP unchanged at 20% (see here for details)

The implementation of the 85 billion euros of purchases are split between the ECB and the national central banks, as shown in Figure 1. This means different regimes of risk-sharing apply to different purchases. While loss-sharing applies to the ABSPP and CBPP3, only 20% of the purchases under PSPP is subject to risk sharing (for more details, see the QE manual Claeys et al, 2015 and the 2016 update Claeys and Leandro)[1].

This division of labour is also evident when looking at how QE is impacting sectoral holdings of government debt issued by euro-area member states. A spike in the share of government bonds held by national central banks can be observed, reflecting the implementation of the QE programme (Figure 2)[2]. Comparing the outstanding government holdings of central banks as of the end of 2015 with the end of 2014, German holdings of government bonds rose substantially from 4.4 to 77.2 billion euros, while Italian holdings increased less markedly, from 102.0 to 165.2 billion euros. The French and Spanish central banks increased their holdings from around 40.0 to 155.9 and 84.9 billion euros respectively.

In percent of the total outstanding debt, this increase is offset by decreases in holdings of other institutional sectors (Table 1). In France and Italy, most of the increase of central bank holdings was offset by a decrease in other resident holdings (such as households and non-financial corporations), while in Spain it is a decrease in holdings by resident banks that offsets the increase in central bank holdings. Interestingly, net purchases by the French and German central banks correlate with net sales by foreign bondholders, rather than by domestic banks.

In conclusion, the most recent update of data on sectoral holdings of government bonds allow us to gauge the impact of the ECB’s asset purchase programme on the distribution of government debt across different holding sectors. While the increase in the share held by domestic central banks was expected, the changes in other sectors’ holdings are less obvious. The increase in the share of bonds held by national central banks is mostly offset by a decrease in holdings by other sectors, and less so by a decrease in the holdings of domestic banks. Overall, it appears that the ECB’s purchases have not yet helped reverse the marked increase in banks’ holdings of domestic government debt which happened during the crisis.

[1] On top of the PSPP, six National Central Banks will carry out the bond purchases under the new corporate sector programme on behalf of the Eurosystem. The ECB will coordinate the purchases and the CSPP will be subject to a full income and loss sharing regime.

[2] This is something that we did not observe at the time of the ECB’s Securities Market Programme (SMP), because those purchases were subject to full risk sharing (according to the ECB’s capital key) and thus classified as holdings from “non-residents”, from the perspective of the issuing government

About the authors

Related content

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

Capital markets union - why now?

What is hindering the EU from achieving a Capital markets union?

European capital markets union: make it or break it

Capital markets union has not delivered, but it should be given a last chance, with a focus on supervisory integration

A tale of two treatises: the Werner and Delors Reports and the birth of the euro

Focusing on the Werner and Delors Reports, this essay aims to capture key ideas and debates, giving a chronological overview of the EMU process