The impact of the crisis on smaller companies and new mechanisms for non-performing loans

The ongoing recession will result in a fresh surge in non-performing loans (NPLs) once payment holidays and moratoria end later this year.

In November 2019, the European Banking Authority (EBA) and the Eurogroup reviewed progress in ‘risk reduction’ in the euro-area banking system and highlighted the improvement in the management of non-performing loans (NPL). The NPL ratio in ECB-supervised banks had fallen to 3.1% of total loans at end-2019, from 7% in 2015, mirroring the ambitious NPL reduction targets set by the European Central Bank for about 30 high-risk banks. Several elements of the Council’s 2017 NPL Action plan had been implemented, including the ‘prudential backstops’, which require early provisioning, thereby discouraging banks from holding on to questionable loans.

Supervisors tackling the fallout from non-performing loans from the European debt crisis rightly prioritised disposal of NPL assets via the secondary loans markets. Industry estimates suggest that that NPLs worth €340 billion in gross value were transacted in 2018-2019 alone (though ECB figures suggest considerably lower disposals). This approach recognised that banks would inevitably remain constrained in designing workout options for distressed borrowers because they could not, at short notice, build up sufficient capacity and skills in restructuring and servicing. The ECB guidance to banks of 2017 has been effective in raising banks’ NPL management capabilities in areas such as loan documentation and robust disposal mechanisms.

The securitisation of NPL portfolios leveraged government support and played a major role in boosting NPL sales. These schemes, involving government guarantees on senior tranches of NPL portfolios, bridged the persistent valuation gap between banks’ offers and investors’ bids. Italy’s Garanzia Cartolarizzazione Sofferenze (‘GACS’), for instance, is estimated to have mobilized €60 billion of gross value in 14 transactions up to March 2019. Greece gained approval from the European Commission in late 2019 for its very similar ‘Hercules’ scheme, and banks initiated a number of transactions earlier this year to meet the ambitious reduction targets set by the ECB for end-2021.

The European secondary loans market has undergone rapid change as volumes have expanded over recent years. The number and types of investors have grown significantly (the four largest investors were US investment firms that have accounted for just over half the transactions since 2014). Loan servicers now operate across borders and offer more bespoke solutions. But the strategy of fostering NPL disposals by euro-area banks to dispersed financial investors may reach its limits in the current recession. The capacity of governments to guarantee securitised portfolios will be more constrained, and the market for distressed loans and high-yield structured notes at the bottom of the creditor hierarchy has clearly been disrupted. Recognising the imminent constraints, the National Bank of Greece has now re-tabled a proposal for a national asset management company, which would function as a bad bank, as another tool to try to remedy the elevated NPL rates in the country.

The limitations of a young market

The secondary loans market may be inefficient in transferring assets from smaller banks or those owed by smaller-scale borrowers. Banks incur relatively high fees in preparing small loans for sale to investors. Transaction platforms could make price formation more transparent by acting as a central venue for banks and investors, though their shares of trades remain modest. Market failures may arise because of problems in the coordination between several claims on a single borrower, or where there are high fixed costs involved in the financial restructuring of smaller borrowers. The incentives of a loan servicer, who acts on behalf of the asset owner, may not be well aligned.

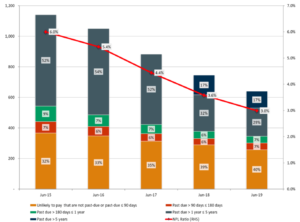

The limited transfers of loans that have not yet defaulted, but are classified as ‘unlikely to pay,’ are further evidence of the market’s limitations. Such loans are past due for less than 90 days, but the lender typically expects the repayment only by realising collateral. Such loans still account for 40% of current European NPLs, but up to last year they accounted for only minuscule shares of European NPL transactions. Banks have so far offered to investors primarily loans in foreclosure, which have been in default for some time, and where there is a straightforward path to enforcement of collateral or liquidation. The chart below shows a particularly rapid reduction in such older loan vintages. By contrast, investors and servicers appear less keen to handle more marginal borrowers, who might require more complex engagement and restructuring if firms are still viable. This is also a reason why ‘unlikely to pay’ NPLs were excluded from the Italian securitisation scheme.

European NPLs by duration of borrower default

Source: EBA.

More complex restructuring cases will now occur in large numbers. The current sharp recession will result in substantial corporate losses that, in the European Commission’s baseline scenario, will amounts to €720 billion by the end of 2020. According to these estimates, about 25% of EU firms would see a shortfall in equity, mainly among firms that were already vulnerable going into this crisis. The sectors most affected by the current recession, such as hospitality and leisure, are largely composed of small and medium-sized enterprises (SMEs). Even where such SMEs default on their loans, many could still be viable if their debt is restructured.

Restructuring the debt of SMEs is more challenging because the business assets and personal funds of the entrepreneur are often intertwined, and the fixed costs of restructuring are high relative to the value that can be recovered. The lack of up-to-date information on the borrower or underlying collateral can also impede proper financial restructuring. For these reasons, banks tend to demand excessive collateral, and appear to be more inclined to exercise their rights over the collateral in a crisis, rather than preserving value and skills in the company through restructuring.

Supportive legislation at EU and national levels

Governments should now expedite a restructuring framework and insolvency regime that encourages the preservation of viable SMEs. The European Commission has already tabled several elements of such a framework.

There should be an ambitious transposition of the 2019 Restructuring Directive (EU 2017/1132). Even though this Directive does little to harmonise the widely diverging insolvency laws of EU countries, it puts in place a more streamlined process that could give entrepreneurs a ‘second chance’ and protect fresh financing offered following a declaration of insolvency.

The directive on credit servicers, which the Commission proposed already in 2018, has progressed more slowly and has been held back by the more controversial elements on accelerated enforcement of collateral. Early this year a trimmed back directive was edging closer to political agreement and member states should similarly reflect the key elements in national law as soon as possible. Greece has already done so, though, as in Italy, with one important exception: credit servicers offering refinancing, for instance in the context of a financial restructuring of the defaulted borrower, are subject to the more onerous licensing regime that applies to banks. But such refinancing, ideally in a more senior and protected position, is exactly what will now be needed from NPL investors.

There is a risk that designing numerous individual restructuring plans will overwhelm banks. The experience with similar corporate debt crises that took a toll on SMEs, such as in Korea in the late 1990s, suggests there is a case for more streamlined temporary restructuring regimes that expedite the corporate sector recovery. Governments could define clear criteria for determining a distressed firm’s viability, and prescribe standardised restructuring options for eligible enterprises, such as capitalisation of arrears or extended payment terms. The just released report of an industry task force in the UK, where unsustainable debt could reach £ 100 billion by early next year, offers some proposals on how state-guaranteed loans could be converted into equity-type instruments. The challenge is to design immediate restructuring solutions that can become effective through agreement between lenders and the distressed borrowers, without the need for formal and lengthy court processes.

About the authors

Related content

Geopolitical risks and banking sector vulnerabilities: implications for the SSM

The EU economy is vulnerable and will be increasingly exposed to geopolitical risk arising from the less peaceful course of international relations.

The Listing Act: no more than a minor boost to EU equity markets

Streamlining of the company listing process is welcome, but more fundamental reform is needed to revive the European Union’s flagging equity markets.

The potential of sovereign sustainability-linked bonds in the drive for net-zero

Sovereign SLBs could help incentivise climate policies in EU countries, and accelerate emission reductions.

Assessing the risks and prospects of European banking system

Giuseppe Porcaro and Nicolas Véron speak with Sharon Donnery about European banking supervision.