Debunking 5 myths about Frexit

French elections are fast approaching and the debate on euro membership is now in full swing. ‘Frexit’ supporters promise that the benefits of leaving

This blog is also available in French on laviedesidees.fr

A debate is raging in France about the benefits and drawbacks of the Euro. The argument echoes that of the first half of the 1990s – between those in favour of joining the Euro and those against. However, the parallels are misleading and should not inform today’s debate. The Euro has been the official currency of France for almost two decades now, and exiting it would be very different from choosing not to join in the first place. In this blog post, I expose five myths about the supposed benefits of Frexit.

Myth 1: Frexit would unambiguously boost French competitiveness

Advocates of leaving the Euro claim that Frexit would provide a competitiveness boost to French exports and essentially solve two alleged problems: the persistent trade deficit and the decline in market share for French goods, especially compared to Germany (see graphs below).

Indeed, in theory, a flexible exchange rate provides an automatic adjustment mechanism to correct external imbalances. It plays the role of a shock absorber for country-specific shocks and allows countries to quickly improve their price competitiveness. And a nominal devaluation should be easier and less painful to achieve than an internal devaluation inside the Eurozone, which would requires a period of lower inflation and wage growth than euro area partners.

First of all, these two problems are largely exaggerated. The decline in export market share since 2000 is not specific to France and is actually the norm across industrialised countries. It is the result of China and other emerging countries joining the global economy. Germany’s stable share is actually an outlier in comparison to other advanced countries. As for the French trade deficit, it has in fact slowly decreased over the last 5 years and its current level (-1.3%) is not a concern.

In addition, the Euro has weakened over the last two years due to the accommodative monetary policy of the ECB. And this has already provided a significant boost in terms of price competiveness. Since mid-2014, the Euro has depreciated by 25% against the US dollar and it cannot be considered overvalued for the euro area as a whole.

In fact, the main issue comes from imbalances within the Eurozone. According to a recent estimation, France is, in real terms, overvalued by 7% with respect to the Eurozone average and by 20% with respect to Germany. A new French currency (let’s called it the Franc for simplicity) would thus probably depreciate against the Euro after its introduction.

At first glance, recent estimations suggest that the French imports and exports are sensitive to price shifts[1], so a nominal depreciation against the Euro would help France improve its trade balance after a few years. Indeed, I am not denying the powerful effects of exchange rate fluctuations on the trade balances (as confirmed again recently in an IMF paper). However, for the effects of a depreciation to be beneficial and long-lasting, inflation needs to be contained and therefore monetary policy needs to be credible to avoid a dis-anchoring of inflation expectations. Otherwise, the inflation spike resulting from a sudden increase in import prices can lead to second-round effects through an upward adjustment in wages and other prices which gradually erode the gains from the nominal depreciation.

Equally important, if France were to leave the Euro, it could be followed by others. In that case, the Franc would depreciate against northern European currencies, but it would probably appreciate against new currencies from Southern Europe. Looking at France’s main trading partners, it is true that Germany represents by far the most important single export market for France – 16% of French exports. But Southern Europe as a whole amounts to a similar percentage.

Given the current sectoral specialisation of French industry, an increase in price competition resulting from an appreciation of the Franc against southern currencies could end up being more detrimental for the French trade balance than the benefits of the depreciation against the currencies of Germany and other Northern countries.

So, overall, it is true that a flexible exchange rate is a helpful adjustment mechanism to absorb temporary shocks and to reduce external imbalances, if combined with a credible monetary policy framework. However, France does not really have an overvaluation problem relative to the rest of the world and within the euro area the country is not very far from the average. Supposed gains in terms of price competitiveness would thus be much less significant than what Frexit supporters suggest.

Myth 2: Frexit would lead to a more appropriate monetary policy

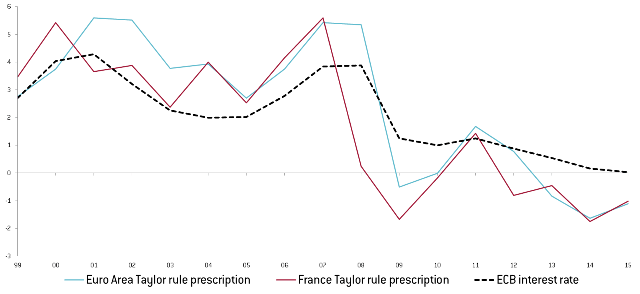

Another major benefit promised by Frexit advocates is an independent monetary policy tailored to the domestic economy and not to the Eurozone average. This argument is valid in theory, but in practice it is once again not relevant for France. France is generally well represented by the Eurozone average because its economy behaves like the average of the euro area. For instance, the interest rate prescriptions provided by simple Taylor rules (see graph below) for France and the euro area are very similar. This suggest that monetary policy decisions made by an independent Banque de France following a mandate similar to the ECB’s would not be so different than the ones taken by the ECB governing council.

Figure 3 – Taylor rules for France and the Euro area

Source: Bruegel based on Eurostat, AMECO, Fries et al. (2016), Holston, Laubach and Williams (2016). [8]

An exit from the monetary union could actually make French monetary policy more difficult, especially in the short term, as it might lead to an increase of inflation to undesired levels. Not only would the Franc depreciate, but the experiences of countries abruptly changing exchange rate regimes suggest that some overshooting would take place beyond what fundamentals require.

Depreciations make imports more expensive, and past episodes of rapid currency depreciation (see table below) suggest an immediate surge in inflation. Given the importance of imports in some key sectors in France (energy in particular), a strong depreciation of the Franc would have a negative effect on the economy in the short term and would (at least) lead to a temporary spike in inflation.

To ensure that the spike is only temporary, a credible monetary framework would need to be established quickly. This is, however, incompatible with other policies advocated by the partisans of Frexit, who also want to deprive the Banque de France of its independence and authorise direct financing of the government by the central bank. This appears especially incoherent with the promise by Frexit advocates to keep inflation low after leaving the Euro.

Frexit advocates want to get rid of the Euro to boost French exports, but paradoxically they are also sceptical towards a fully flexible exchange rate regime because they fear excessive volatility in the foreign exchange market. In fact, general public support for flexible rates has always been relatively weak in France. That’s why some Frexit partisans are pleading for the return to the ECU and to the European system of fixed exchange rates that was in place before Maastricht. It is strange to want to leave a common currency only to bind yourself to another currency in a fixed exchange rate system.

Even putting aside this paradox, pegging oneself to a foreign currency requires policy credibility to achieve exchange rate stability. Monetary sovereignty under such a system is in practice illusory because the Banque de France would have to adjust its policies to defend its parity and thus adapt its interest rates in reaction to its neighbour’s cyclical situation (be it the Eurozone or Germany) [2]. In this case, the current shared sovereignty in the Governing Council of the ECB appears preferable in terms of macroeconomic policy performance, as well as sovereignty.

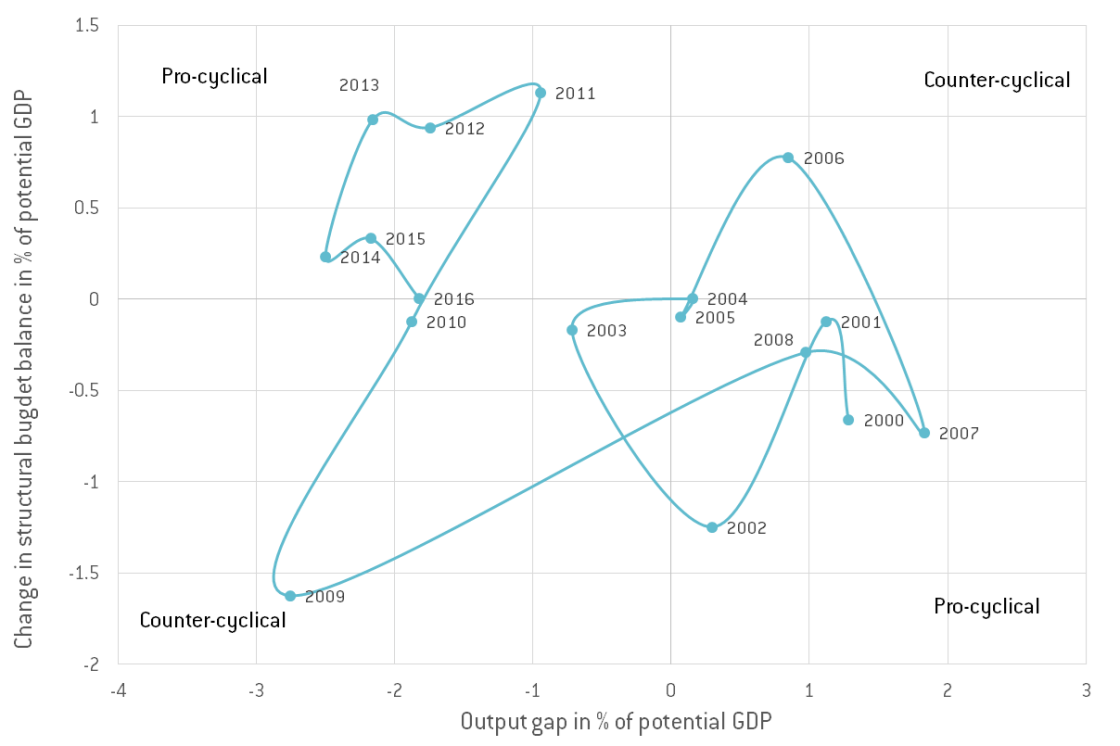

Myth 3: Frexit would relax constraints on fiscal policy

Frexit partisans suggest that leaving the Euro could free the country from the constraints of European fiscal rules and allow the French government to pursue a more countercyclical fiscal policy. But countercyclical fiscal policy doesn’t seem to be a French speciality anyway, and leaving the Euro could damage France’s credibility, making it difficult to borrow the money needed for counter-cyclical spending.

As the graph below shows, over the last 17 years, French fiscal policy has only been countercyclical in 2006 and 2009. The rest of the time fiscal policy is mainly procyclical. In good times the government increases spending or cuts taxes, even if this drives GDP further above potential. In bad times the government increases taxes and cuts expenditures, even if growth is negatively affected.

Figure 4 – Fiscal stance in France

Source: Bruegel, based on World Economic Outlook (October 2016 – IMF)

But it is difficult to believe that this behaviour is driven by the European fiscal rules. As I explained in a paper published last year, it is true that the current European fiscal framework is highly imperfect. This has led the European Commission to provide mistaken policy recommendations to member states during the crisis. These recommendations might have played a role at the height of the euro crisis (from 2011 to 2013 in particular), encouraging a fiscal tightening at the worst moment. However, most of the time, bad fiscal policy in France seems to be self-inflicted.

Frexit would probably not change that – quite the opposite. The French government might not have to listen to recommendations from the European Commission anymore, but Frexit could also cut off the market access needed to implement countercyclical policies.

Conversion of public debt from Euros to Francs might be possible from a legal perspective[3] but such a drastic change in the conditions of debt instruments could be technically considered as a default by rating agencies. This would make it more costly for the French government to borrow from financial markets, and could even result in France losing access to international markets for a few years.

In any case, it would be logical for international investors to require higher interest rates in new bond issuances to compensate for the depreciation of the currency and to hedge against inflation risk. The French government would also be under much more market scrutiny. In addition, in the long run, franc-denominated debts would lose the benefits of being issued in a reserve currency, a status reserved to countries with a long history of credible and stable monetary policy.

For all these reasons, borrowing from international markets to support the economy when needed could become much more difficult and expensive. And trying to circumvent that by using the central bank to finance budget deficits will not be a good idea at a time where it needs to establish its credibility to anchor inflation at a low level or to defend a stable exchange rate.

Myth 4: Frexit would be painless for French companies

Currency fluctuations affect economies through various channels. Apart from trade, another important channel is the balance sheet channel. The combination of currency mismatches in the balance sheets of some economic agents and unexpected currency fluctuations played an important role in the financial crises that affected emerging markets at the end of 1990s and the beginning of the 2000s.

The main mechanism at work during these crises is pretty simple. The implementation of what were considered credible fixed exchange rate regimes, such as currency boards, led agents to think that it was safe (and cheaper) to have un-hedged positions in foreign currencies. However, the abrupt abandonment of these exchange rate regimes and the subsequent domestic currency depreciation led to a significant increase in the value of the debt issued in foreign currency, making it difficult to repay and sometimes ending in a series of bankruptcies[4].

The French government and French banks, companies and households do not borrow much in foreign currencies. When they do they typically hedge themselves against exchange rate variations. The issue with leaving the Euro would thus not be about existing debts in other (non-euro) currencies. The difficulty would be converting assets and liabilities in Euros into Francs.

The governing law and jurisdiction of the financial contracts would determine whether an instrument can be converted, or if it will remain in Euros. To make it simple, if a debt is contracted under French law, the conversion into Francs should be possible. If it is contracted under foreign law – generally English or American law – it will continue to be denominated in Euros after Frexit. Some actors will therefore end up having to repay their debts in what would become for them a foreign currency, and some un-hedged currency mismatch would appear rapidly in their balance sheets. (Because the Euro was considered irreversible, there was no need to protect oneself against the redenomination risk coming from debts contracted in Euros under foreign law).

Most household and SME debts take the form of loans from French banks (or French subsidiaries of foreign banks) which are therefore contracted under domestic law and should easily be converted into francs. Conversely, assets of French banks in the form of domestic loans would be redenominated in Francs, while on the liability side deposits made by households and corporations would also be converted.

The biggest risk would therefore come from other debt instruments such as cross-border loans from foreign banks and bonds issued under foreign law by French banks and big non-financial corporations. In aggregate, the situation could ex ante appear to be manageable, but many companies would be affected by currency mismatches[5]. In practice, at the micro-level, the transition would be chaotic and lead to thousands of endless legal disputes that would hurt economic activity. These mismatches would lead to many instances of debt restructuring, possible bankruptcies or bailouts of systemic actors, and the subsequent negative impact on creditors, shareholders and taxpayers. Frexit would end up looking like a lottery for all companies in France: having more assets or more liabilities converted into Francs would determine whether they are bankrupt or richer after Frexit.

Myth 5: Frexit would be smooth and orderly

To anticipate what could happen in such an exceptional situation, it is natural to look at historical experiences of currency break-ups. Rose (2006) offers a database of such departures from currency unions since World War II and counts 69 such occurrences (not taking into account the abandonment of currency boards or hard pegs). This paper is often quoted by Frexit advocates because Rose does not find much difference between the countries leaving and staying in the monetary unions in terms of macroeconomic performance.

The problem is that these data provide little useful information for today’s France. Most monetary union dissolutions in the sample took place after the independence of former European colonies or after the fall of the Soviet block. Current circumstances differ in many relevant ways: the size of the French economy; its financial development; the importance of the financial sector; the financial links between France and other European countries which have been subject to free capital movement for more than two decades. A Eurozone breakup, or even just Frexit, would be an unprecedented event which could not be compared with the currency dissolutions of the last sixty years[6].

In fact, the very idea of quietly organising a referendum in France followed by a calm negotiation with European partners is illusory. The main issue is that a ‘preventative’ bank run and capital flight would take place as soon as people consider Frexit a credible possibility and expect their deposits to be converted into a weakening currency. Depositors participating in a bank run would be perfectly rational in that case[7]. The chart below shows that in Greece, a slow-motion bank run started as soon as people started believing that a euro exit was a credible possibility. This movement accelerated in 2015, and resulted in bank closures and the imposition of capital controls at the end of June. The same would happen in France to avoid a banking meltdown. Again, the Greek example is informative about the negative impact of such a move: after capital controls were put in place, real GDP fell by -1.7% during the third quarter of 2015 alone, as the economy was frozen because of banking restrictions.

In France, a euro exit is still considered as a tail risk by markets and depositors for the moment, but sovereign bond markets have already reacted to changing probabilities of Frexit. If Frexit was becoming more probable, deposit withdrawals and the sovereign risk premium could increase quickly.

Another risk is that Frexit could happen by accident, before it could be properly organised or even before a referendum. Imagine, for instance, a scenario in which the Front National wins the elections and the French government’s rating were downgraded by all major ratings agencies below BBB- (following Fitch and Standard & Poor’s rating system). This would make it difficult for French banks – who could also be facing a bank run at that time – to access the main refinancing operations of the ECB, as they would not be able to use French government bonds as collateral in the Eurosystem monetary operations. In turn, they could be forced to use the – more expansive but also more flexible in terms of collateral – Emergency Liquidity Assistance (ELA) at the Banque de France under limits set by the ECB’s Governing Council.

The situation would then be pretty similar to one in Greece in February 2015. And as in 2015, the ECB would be caught in extremely political discussions about whether it should continue providing liquidity to the French banking sector to face the run or not. The decision would be even more complex for the ECB this time because the ECB would face a government openly favourable to an exit from the monetary union. And if its decision were to stop providing liquidity, the Banque de France and the French government would have no other choice but to decide whether to impose very strict capital controls or to launch a new currency to provide the needed liquidity to the banking sector. The risk of Frexit could thus become a self-fulfilling prophecy.

The probability of such a scenario is today extremely low and the sequence of events to arrive at that point unlikely. But this thought experiment shows how quickly such a situation could spin out of control and lead to a disorderly exit from the monetary union, which could have devastating consequences for the French economy.

Overall, it is important to realize that the French financial system is at the core of the euro area financial system and is tightly interwoven with the global financial system. Frexit would lead to a freezing of financial flows and bring the global financial system to a cardiac arrest. The failure of Lehman brothers could look like a small shock in comparison, and even that had major real economic implications.

Notes

[1] For this depreciation to result in an improvement of the trade balance, French exports and imports need to be sensitive enough to prices. In economic terms, the Marshall-Lerner condition has to be fulfilled, i.e. the sum of the absolute value of price elasticities of import and export has to be bigger than one.

[2] Committing to a fixed rate with the Euro or with a basket of European currencies (in case the Euro would disappear after Frexit) would lead to a come back of the so-called ‘n-1 problem’ inherent to any fixed exchanged rate system. Basically, if n countries participate to a fixed rate system, only n-1 central banks need to defend their fixed rate towards the nth country. This often results in an asymmetric monetary system in which one country, the most credible one generally, can pursue a monetary policy related to its own domestic goals (inflation and/or growth) while other countries adjust their interest rates to maintain the parity without taking into account their internal economic situations. This was mostly the case from 1945 to 1971 with the US at the centre of the Bretton Woods global fixed exchange rate system and after its demise with Germany at the centre of the European ‘currency snake’ from 1972 to 1979, and of the European Monetary System after 1979.

[3] Contrarily to the private sector, redenomination of the French public debt from euro to francs should not be a problem because almost all of it (approximately 95%) is issued under French law, so the value of past debts should not increase in terms of francs if the new currency depreciates.

[4] The case of Argentina at the end of 2001 is a perfect example of this mechanism: the unexpected end of the currency board and the conversion in pesos of deposits held in dollars were followed by a massive depreciation of the peso, by more than 60% in trade-weighted terms. Given this, many debtors saw the value of their debt from abroad explode in terms of local currency, which led to huge losses, difficulties to repay their debt, and in the end a series of defaults.

[5] Several papers have recently attempted to measure the extent of the potential mismatch that would result from Frexit. Durand and Villemot (2016) using macro data from the BIS argue that an exit should be manageable on aggregate because French companies and households own enough assets abroad, whose value would be increased in terms of francs by the depreciation, compared to the relevant liabilities that would not be converted. It is true that assets and revenues from abroad could mitigate the negative impact of having debt in a foreign currency. Nevertheless, the issue with using aggregate numbers is that it misses completely potential mismatches in specific firms. For instance, if half of the firms would be vulnerable to Frexit and the other half would benefit from it, on aggregate the economy could ex ante appear to be able to cope well with such a shock even if that’s not the case given that it would be impossible to redistribute positive and negative impacts across firms. To avoid that pitfall, Amiel and Hyppolite (2015) build a comprehensive firm-level dataset of major French banks and non-financial corporations. They show that, in their sample, between 41% (in the best-case scenario) and 59% (worst-case) of euro-denominated marketable debt is issued under foreign law and would therefore not be converted in francs. Moreover, they also show that numerous corporations with ‘foreign debt’ (in the financial sector in particular) would not generate enough income from abroad to be able to cover for the repayment of their debt in euros, which could quickly lead to very serious difficulties for some firms, and ultimately to some defaults, or to some significant bail-outs of systemically-important financial and even non-financial corporations by the government.

[6] The break-up of the Czechoslovak currency union in 1992 is often used as an example of a smooth and orderly currency separation that could be emulated in the Eurozone. But, the two situations are very different. Czechoslovakia had been socialist for more than four decades and its financial system was in its infancy when it happened. Moreover, the negotiated solution between Czechs and Slovaks included massive transfers from the strong currency country towards to the weak currency one. This would be unthinkable today in the Eurozone.

[7] If depositors expect the new currency to depreciate (which again is one of the goals pursued by Frexit advocates), they will have an incentive to take their money out of their bank accounts before the conversion, keep it in cash or put it in a bank of another Eurozone country, wait for the new currency to depreciate, convert their money in francs once it has hit rock bottom, and make a profit (in the new currency) equivalent to the depreciation that has taken place.

[8] The ‘Taylor rules’ follow a slightly modified version of Taylor’s specifications (1993) and take the form: r=inflation+r*+0.5(inflation-target)+0.5(output gap), using the latest output gap estimations from the European Commission, core inflation for the euro area and France, and r* equal to the time-varying estimates of Fries et al. (2016) and Holston, Laubach and Williams (2016). For more details on the Taylor rule used, see explanations in Claeys (2016)

About the authors

Related content

Inflation inequality in the European Union and its drivers

What will it cost the European Union to pay its economic recovery debt?

Servicing the EU debt until 2058 seems feasible, despite increased borrowing costs, but member countries must make choices about budget funding

A tale of two treatises: the Werner and Delors Reports and the birth of the euro

Focusing on the Werner and Delors Reports, this essay aims to capture key ideas and debates, giving a chronological overview of the EMU process

Ukraine’s future with the EU

What happens after the start of Ukraine's official accession talk?