Charts of the week: funding costs keep coming down in the wave of euro optimism

Funding costs in the euro area have continued to decrease since Mario Draghi’s July announcement. This blog post updates our previous data covering th

Funding costs in the euro area have continued to decrease since Mario Draghi’s July announcement. This blog post updates our previous data covering the insurance cost of the 5 major financial and non-financial corporations and the governments of France, Germany, Italy and Spain.

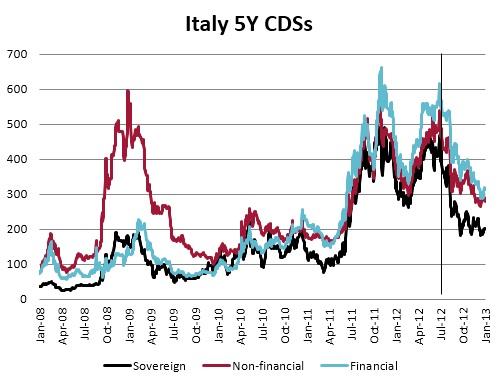

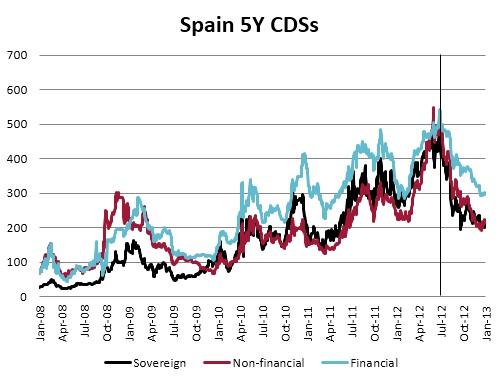

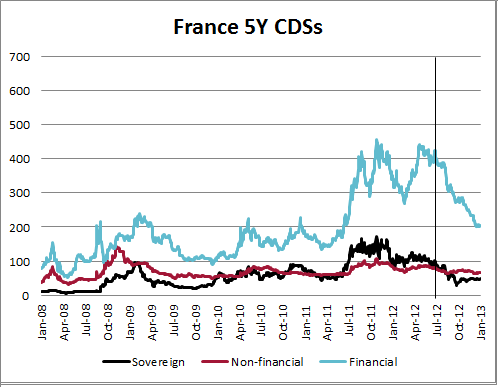

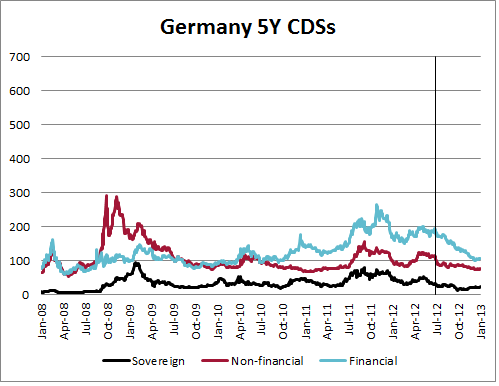

The risk premia for the sovereigns have decreased by 56% in Italy and Spain, 52% in France and 32% in Germany during the last 6 months (since Draghi’s announcement) and are now lower than at the beginning of 2012. Lower sovereign yields in Germany during the last months document that less risk in the euro area periphery is also beneficial to Germany.

As regards the funding costs for the 5 major financial and non-financial corporations:

o In Spain, they have decreased by 59% for the non-financials and 44% for the financial corporations. Funding costs of Telefónica, Iberdrol, Repsol, Gas Natural and Abertis are now at about the same level of risk as the Spanish government.

o In Italy, funding costs for both sectors have also dramatically come down (by 47%).

o In France they have decreased by 19% for the non-financial and 52% in the case of financial corporations. (It must be noticed than 5Y CDS of Dexia (currently at 396 bp) significantly increases the average of the French financial corporations from around 156 to above 200 basis points)

o In Germany they have decreased by 45% in the financial sector and 33% in the non-financial

As in the previous blog entries, we plot the CDS risk premia on 5 year sovereign bonds along the CDS premia for the financial and non-financial corporate bonds of the five largest corporations in Spain, Italy, Germany and France[1]. We build an unweighted average across the largest five financial and the five non-financial corporations. The corporations included are listed in the table below.

The vertical bar marks Draghi’s announcement of doing whatever it takes to preserve the euro.

|

|

Italy |

Spain |

France |

Germany |

|

Financial Corporations |

Unicredit |

Banco Santander |

BNP Paribas |

Deutsche Bank |

|

Unione di Banche Italiane |

BBVA |

Credit Agricole |

Commerzbank |

|

|

|

Banco Popolare |

Banco Popular Espanol |

Dexia Credit Local de France |

HypoVereinsbank |

|

|

Intensa Sanpaolo |

CaixaBank |

Societe Generale |

Bayerische Landesbank |

|

|

Banca Monte dei Paschi di Siena |

Caja de Ahorros y Monte de Piedad de Madrid |

Natixis |

Norddeutsche Landesbank |

|

Non-Financial Corporations |

Atlantia |

Telefonica |

Total |

Siemes |

|

ENI |

Iberdrol |

Sanofi-Aventis |

SAP |

|

|

|

ENEL |

Repsol |

LVMH |

Basf |

|

|

Telecom Italia |

Gas Natural |

L'Oreal |

Volkswagen |

|

|

Fiat |

Abertis |

GDF Suez |

Daimler |

[1] For financial corporations, the sample includes the top five financial institutions ranked according to its value of total assets at the end of 2012. Non-financial corporations have been selected according to the Financial Times' Global 500 list, where ranking is based on prices and market values from 30 March 2012. If data from one of the top-five ranked institutions was not available (financial and non-financial), the next highest ranked institution with data was considere

Related content

Taxation for Competitiveness: enhancing EU's own resources

How can the EU improve tax efficiency and establish new resources amid pressures for competitiveness, tax fairness, and green transition?

The macroeconomics of decarbonisation

At this event we will launch the book "The Macroeconomics of Decarbonisation: Implications and Policies"

What visions for Europe? Unpacking EU parties’ economic strategies

The EU elections are around the corner. What economic plans are the parties advocating for?

Halftime for the European Union’s recovery fund: is the glass half full or half empty?

How has the RRF performed at its halfway point in terms of implementation, results orientation and additionality for future EU funding instruments?