Blogs review: Takeaways from Jackson Hole

Although Jackson Hole was relatively calmer this year in the absence of market moving speeches, it featured a number of provocative research pape

What’s at stake: Although Jackson Hole was relatively calmer this year in the absence of market moving speeches, it featured a number of provocative research papers. Robert Hall suggested that the tradition of regarding high unemployment as a disequilibrium may rest on a misunderstanding. Arvind Krishnamurthy argued that the portfolio balance channel of QE works largely through narrow channels contrary to what the Fed thinks. And Helene Rey argued that the global financial cycle transforms the monetary policy trilemma into a “dilemma”. In this review, I focus on the first two contributions.

Financial crises, higher discount factor and higher equilibrium unemployment

Robert Hall writes that the tradition of regarding high unemployment as a disequilibrium that gradually rectifies itself by price-wage adjustment may rest on a misunderstanding of the mechanism of high unemployment.

Robin Harding writes that the meat of Hall’s paper is about why inflation did not fall much after the crisis despite high levels of unemployment. This has been a surprise during the last few years: unemployment has not driven down wages in a way that led to deflation. The standard explanation is that yes, all that slack in the economy should have led to falling prices, but workers will not let wages fall and inflation is anchored to central bank targets.

Robin Harding writes that what Hall proposes is that the financial crisis did not just affect demand in the economy but also directly affected supply. Thus high unemployment was not a disequilibrium, where the economy’s supply capacity was much greater than demand, but actually an equilibrium because supply temporarily took a hit as well. This rests on a model where hiring a worker is like an investment decision: it depends on all the revenue that a worker will produce in the future, relative to their wages, discounted back to the present day.

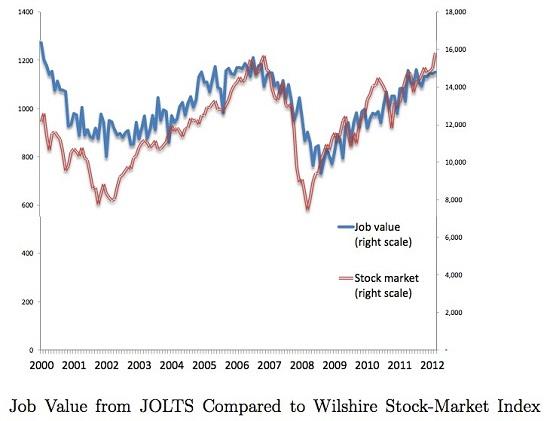

Robert Hall considers a source of fluctuations in the job value that has been implicit in the Diamond-Mortensen-Pissarides model from the outset, but has escaped attention. The job value is the present discounted value of the future difference between a worker's productivity and the worker's pay. Even if that difference is unaffected by a negative shock, if an increase in discount rates accompanies the shock, the job value will decline and unemployment will rise accordingly.

Source: Robert Hall

Robert Hall writes that the evidence that the job value moves along with the stock market has two implications for output in the post-crisis economy and in other contractions. First, events that trigger a rise in financial discounts, such as a financial crisis, will lower job values substantially, causing a corresponding increase in unemployment and decline in output. In other words, there is a direct linkage from financial disturbances to unemployment, not just a response operating through a decline in the demand for output. A financial crisis has a direct adverse effect on output supply through the discount channel. Second, other forces connected to a financial crisis, such as a decline in real-estate prices, cause declines in output demand. The zero lower bound may block a decline in the discount rate that would have had a favorable effect on the job value and thus cut unemployment and increased product supply.

Paul Krugman writes that Bob Hall’s paper for Jackson Hole is, characteristically for Hall, a mix of very sensible stuff and strange-looking stuff that just might involve a deep insight. Hall used to be famous at MIT for talks along the lines of “Not many people understand this, but the IS curve actually slopes up and the LM curve slopes down” — and then, not most of the time but often enough, his apparent craziness would turn out to be a big insight that changed the way you thought about a major issue.

Market segmentation, limits to arbitrage and Wallace Neutrality

Cardiff Garcia notes that in a previous paper Arvind Krishnamurthy and Annette Vissing-Jorgen recommended that the Fed continue buying MBS while actually selling longer-term Treasuries. (This would have been like a tweaked version of the Fed’s earlier Operation Twist). In this new paper, they again emphasize the superior potency of MBS purchases vs. Treasury buying, this time stressing how they incentivize banks to originate new mortgage loans. Neil Irwin notes that the with Treasury bonds is that they fulfill a unique role at the bedrock of the financial system, allowing investors an ultra-safe place to park money that can be readily used as collateral. When the Fed buys up a big chunk of Treasury bonds, fewer other investors can enjoy that benefit. That would be fine if those investors could just shift into near-substitutes, like highly rated corporate bonds, which could lower borrowing costs for big companies and thus encourage them to invest. But the problem is that there aren’t that many AAA-rated companies, so those benefits have not percolated through the economy to the degree one might hope.

Neil Irwin writes that there is an irony here. If this analysis is right, the economic benefits of QE come from MBS purchases, not Treasuries. Yet the Fed itself prefers not to be in the role of favoring one sector (housing) over others, and so many officials there lean toward focusing heavily, or even only, on the less-effective Treasury bond market.

Arvind Krishnamurthy writes that there exists theoretically a role for LSAPs on Treasury and mortgage yields even after stripping out signaling effects. For example, in the context of mortgage-backed securities (MBS), consider a setting in which a certain set of sophisticated investors (banks, dealers, asset managers) are the only investors in the MBS market (i.e., it is costly for new investors to enter the market) and these investors have limited access to capital, so that there are limits to arbitrage. This is an environment in which MBS yields will be inflated relative to an Arrow-Debreu complete markets benchmark in which MBS risks are broadly diversified across all savers. If capital constraints are slack, there will be no effects of an MBS purchase on prices. The economy then resembles the frictionless economy of Woodford (2012) where LSAPs have no effects on asset prices. On the other hand, if capital is scarce, as was likely in 2008/2009, there will be effects on prices.

Arvind Krishnamurthy writes that asset purchases can have effects precisely because the asset is traded in a narrow and segmented market. Nevertheless, spillovers may arise in this channel. First, to the extent that the LSAP strengthens intermediaries’ balance sheets and relaxes capital constraints, other assets that are traded in a segmented market and concentrated in the portfolios of the MBS specialized investors will also rise in price. Second, there is a possible macroeconomic spillover. If the affected assets are central to economic activity, then the policy may have significant macroeconomic effects and this indirectly spills over to other asset prices.

Arvind Krishnamurthy writes that the portfolio balance channel of QE works largely through narrow channels that affect the prices of purchased assets, with spillovers depending on particulars of the assets and economic conditions. It does not, as the Fed proposes, work through broad channels such as affecting the term premium on all long-term bonds.

Pedro da Costa and Alister Bull report that James Bullard, president of the St. Louis Fed, said Krishnamurthy's focus on market impact immediately following policy announcements was misleading. "I just wanted to push back against this conclusion that you get an effect in one single market and then there's not that much (impact) over a variety of assets," Bullard said. Donald Kohn, a former Fed vice chair, was also skeptical saying that "the findings do not comport very well with the experience of the last couple of months".