Professor Blanchard writes a Greek tragedy

Olivier Blanchard has, with his customary clarity and candor, addressed criticisms of the IMF’s role in Greece’s financial rescue. His is a perso

Olivier Blanchard has, with his customary clarity and candour, addressed criticisms of the IMF’s role in Greece’s financial rescue. His is a personal statement. But in writing it, he also presents the IMF’s operating philosophy and mandate. Blanchard’s statement will, therefore, not only shape our thinking on the evolution of the Greek crisis but it could define how we view the proper role of the IMF. His blog post deserves careful reading and consideration.

The risk of contagion prevented debt restructuring

The critics, he says, complain that “The [official] financing given to Greece was used to repay foreign banks.” But that, Blanchard insists, is not the right way to think of it. Memories of the post-Lehman meltdown were still fresh. The risks of contagion were real, or were perceived to be real, and there were no firewalls to contain those risks. That is certainly the official view. But is it right?

While a moment of great uncertainty, it was also a time for new ideas and initiatives. Barely 10 days after the Lehman fiasco, Washington Mutual Bank became the largest ever bank to fail in the United States and the U.S. authorities forced the creditors and equity holders to bear all the losses. The IMF, in contrast, went in the opposite direction, overriding its well-founded principle that the distressed country’s debt must be reduced to a “sustainable” level. In the Greek case, debt reduction required imposing losses on creditors. To the fear of contagion, a simpler solution—with much lower costs to all—would have been for the French and German authorities to stuff their banks with cash so that they were protected from the losses on their Greek debt holdings.

If even with these efforts, the risk of a wild-fire contagion could not be eliminated, then the question should have been who should bear the burden of preventing the contagion. An IMF paper that bears Blanchard’s name lays out the principle by which Greece should have been compensated—with a financial grant (not a loan)—for agreeing to hold on to its unsustainable debt burden in the interest of limiting losses on others. The IMF paper says:

“[…] there may be circumstances where any form of debt restructuring … would be considered problematic from a contagion perspective. […] in these cases, sustainability concerns could be addressed not through a debt restructuring but through concessional assistance [the official euphemism for financial grants] provided by other official creditors.

The argument is that contagion is a global problem and the global community should share the cost of preventing contagion. Absent such burden-sharing, it is an arithmetical matter that the austerity required on Greece was much greater than it would otherwise have been. And before the terms of the official loans were finally eased, the wind was knocked out of the Greek economy.

But austerity was needed in any event

The critics, Blanchard says, are not right to complain that “The 2010 program only served to raise debt and demanded excessive fiscal adjustment.” Fiscal austerity, he insists, was not a choice, it was a necessity. He makes a strange claim:

“Had Greece been left on its own, it would have been simply unable to borrow. … Even if it had fully defaulted on its debt, given a primary deficit of over 10% of GDP, it would have had to cut its budget deficit by 10% of GDP from one day to the next.”

Surely, that is a non-sequitur. No one has proposed that the alternative would have been to leave Greece “on its own.” That is not what the IMF does. The process requires the creditors to bear losses and the IMF simultaneously provides temporary financing. Both help to ease the pace of fiscal austerity.

In any event, Blanchard says, Greece’s failure to grow was not because of “growth-killing” austerity but because Greece failed to implement structural reforms.

Here he departs from his own script. Speaking to Sky News in April 2013, Blanchard had warned the U.K. authorities that by indulging in obsessive austerity, they were “playing with fire.” Of the major industrialized economies, the U.K. was the slowest to recover from the crisis, faster only than Italy.

If austerity in the U.K. was like playing with fire, in Greece, it was like being in a choke-hold. Unlike in the U.K., Greece had no help from monetary policy; while the U.K. moved aggressively to stabilize its banks, Greek banks continue to be laden with non-performing assets. Without these aids, the entire burden was on Greek fiscal austerity. Greek public expenditure has come down by one-third since 2010; its structural budget deficit of 12 percent of potential GDP has been transformed into a surplus of 2 percent. These are extraordinary degrees of austerity.

Perhaps, the most famous scholarly paper of the crisis is by Olivier Blanchard and Daniel Leigh, in which they say that in the midst of a crisis, austerity slows growth down significantly. And extraordinary austerity slows growth by an extraordinary degree. And yet another IMF paper, this one by Luc Eyraud and Anke Weber, says that if austerity persists, output and incomes will fall and the debt burden will actually increase. The collapse in Greek output and the rise in the debt-to-GDP ratio were validation of these scholarly studies.

There is no acknowledgement in Blanchard’s blog of the very unrealistic expectations that underlay the growth and productivity consequences of structural reform. How could the IMF have assumed such a quick growth rebound without exchange rate flexibility and a global economy still dealing with its traumas? And with structural reforms necessarily designed to lower wages and prices, the debt burden of businesses and households was bound to rise, causing a further slowdown in growth and increasing the government’s debt burden.

The IMF has learned as the crisis has evolved

The critics say: “Creditors have learned nothing and keep repeating the same mistakes.” Not so, says Blanchard.

Between 2010 and 2012, Greek GDP fell much more than had been projected. In his blog, Blanchard says: “fiscal consolidation explains only a fraction of the output decline.” This is an odd claim, as also pointed out by Paul Krugman and Brad de Long. We know that the output collapse was, in large part, due to the severe austerity because the Blanchard-Leigh paper documents that:

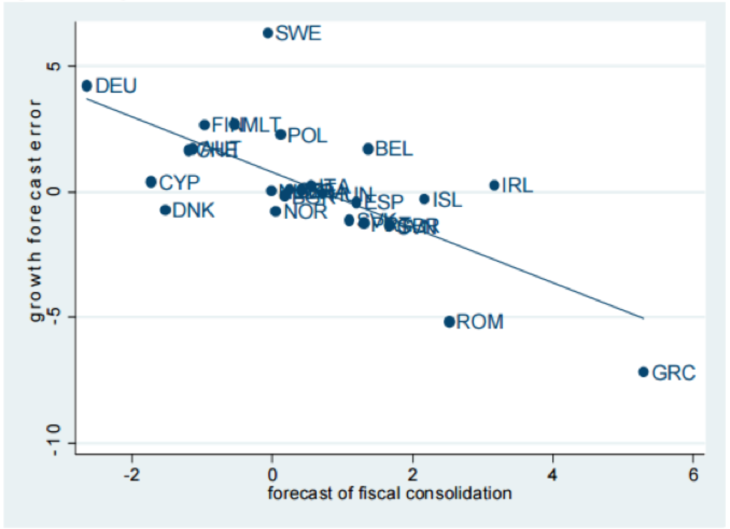

Figure 1: Europe: growth forecast errors vs fiscal consolidation forecasts

Note: Figure forecast error for real GDP growth in 2010 and 2011 relative to forecasts made in the spring of 2010 on forecasts of fiscal consolidation for 2010 and 2011 in spring of the year 2010; and regression line.

Greece fits exactly the European pattern: the Greek economic contraction was so deep because its austerity was so stunningly large.

In December 2012—to retain access to the IMF’s funds—the Greek authorities dutifully said: “Despite the [fiscal] adjustment we have undertaken so far, further efforts are needed to restore fiscal sustainability.” A large adjustment was undertaken in 2013, GDP continued to fall; a small adjustment occurred in 2014 and GDP began to stabilize. So far, the evidence is pretty clear: more austerity, lower growth.

Then, in 2013 and 2014, prices fell by a cumulative 5 percent. This is Irving Fisher’s debt-deflation cycle. As more debt is repaid, demand for goods and services is held back, prices and wages fall, but because the value of debt outstanding does not change, the debt burden grows. This is not rocket science: the IMF’s own studies acknowledge that.

Yet, the IMF’s latest debt sustainability analysis continues to disregard that logic. The IMF projects that the Greek authorities will increase their primary surplus (the budget balance without interest payments) by a net of about 1 percent of GDP a year to about 3½ percent of GDP in three years. Along with continued deep austerity, the debt sustainability analysis also projects renewed growth and a rise in inflation. In combination, the value of GDP—so-called nominal GDP—is expected to grow at between 3 and 4 percent annually in the next two years. Maybe that will happen. But the evidence of the past 5 years says that it is far more likely that nominal GDP will contract by between 3 and 4 percent every year.

When the economy does eventually contract because of the debt-deflation cycle and persistent austerity, the blame will be on the events of the past few months. But it is important to remember that deflation had set in well before the new government came in. By early February, President Obama had diagnosed Greece to be in the midst of a depression. Yes, the past five months will make things worse; allocating the responsibility for that, however, must await a more careful accounting.

When the Greek economy does contract in the coming years, the blame will also be in the lack of structural reforms by the Greeks. Blanchard gives ammunition to those who will make that easy charge. But again, the IMF’s own research department cautions that the dividends from structural reforms are weak and take time to work their way through (see box 3.5 in this link). In contrast, the debt-deflation cycle and the contractionary effects of austerity work immediately. The risk is that the Greek economy may be deeply hobbled before any benefits of reforms show through.

Recall, that Greece has already undertaken heroic austerity, its growth has collapsed, and it has entered a debt-deflation cycle. Irving Fisher told us that at this point, only a reflation—the opposite of austerity—is needed to revive growth. We can all agree that reflation is not possible. But is more austerity really needed now? More to the point, is more austerity sensible now?

Policymaking works under political constraints

Twice in this remarkable essay, Blanchard refers to political constraints on the creditors that have restricted the scope of economic policy. In May 2010, he says, “there was a political limit to what official creditors could ask their own citizens to contribute.” Now, in 2015, he reiterates, “there were and are political limits to what they can ask their own citizens to contribute.” The IMF’s role, he says, is to point to the economic trade-offs, the politics dictates the decisions. Since creditors are unwilling to provide debt relief, the politics dictates that Greece undertake more austerity. That sounds right. But it is wrong on two counts.

First, the IMF’s role is not merely to explain the trade-offs; it is to help make smart policy choices. In this instance, debt relief by creditors now will prevent more debt relief (or larger defaults) later. If the likelihood is great that the austerity demanded will, in fact, lower incomes and increase the debt burden, then the saga we have gone through in the past several months is bound to repeat. Debt relief in driblets will increase the agony and pain of creditor and debtor alike.

Second, for the past several months, the IMF has stood shoulder-to-shoulder with the European creditors in requiring more austerity from the Greeks. Indeed, in demanding more revenues from value-added taxes and reduced pensions, the IMF’s voice has perhaps been the more strident one. But although Blanchard now confirms that the IMF had communicated the need for debt relief to the European creditors, this fact—that the IMF believed that substantial relief was needed—was not made public until the debt sustainability analysis was published on July 2, three days before the Greek referendum. In delaying the release of this analysis, the IMF acted in bad faith. An earlier release would have created a legitimate and transparent public counterweight to those opposing debt relief and would, thus, have weakened the political constraints and increased the prospects of a superior economic decision.

So, why did the IMF finally release its numbers on needed debt relief? The U.S. role is crucial. Although President Obama had in early February warned against squeezing a nation that was in the midst of an economic depression, the U.S. authorities remained disengaged from the discussions. Hence, the European creditors—with their significant voice on the IMF’s Board of Executive Directors—could hold sway. But finally, with the threat of Greece exiting the eurozone becoming real, the Americans woke up to the reality of financial and geopolitical turmoil. It would now appear that the decision to make public the analysis that Greece needed debt relief came at the prompting of the American authorities.

Only July 7, U.S. Treasury Secretary Jack Lew called for more debt relief by the European creditors, and nearly simultaneously, the IMF’s Managing Director, Christine Lagarde, made a nearly identical statement. Indeed, the IMF’s coy phrase “debt operations”—its code for debt relief—was dropped and “debt restructuring” could now be openly stated.

What lessons have we, in fact, learned?

The economics of a program design based on the IMF’s research, which I outlined on June 21 on voxeu, still looks pretty good to me. The primary surplus should be maintained at 0.5 percent of GDP for the next three years. There should be sufficiently large debt relief upfront—now, not as a vague promise to consider relief later—so that: (a) Greece is not forced to borrow new money from official creditors to repay their old loans; and (b) in three years, the debt burden is so low that Greece can borrow from private lenders with sovereign contingent convertibles to create a limit on the borrowing. Of course, the politics of this is impossible, as many would no doubt point out.

That the IMF operates under “political limits” is more troubling. The experience of the past few years is a reminder that the IMF acts in the (often misguided) interests of its major shareholders. For this reason, the IMF cannot be a technocratic institution that speaks truth to power. At crunch time, it must do as it is told. Thus, the question must be asked, why does the IMF exist, and for whom?

And, as for Greeks, in 2009, their problems were of their own making. But then they got trapped in a power play that took on a life of its own. In that power play, politics defied the economics. That should not have been a surprise: the euro emerged from a political process that defied economics. The past few years were merely a logical continuation of that economically illogical construction. The deal hammered out this past weekend—if it is a real deal—remains defiant of economic logic, and the likelihood is high that Greeks will suffer more pain and the creditors will eventually see less of their money. That ultimately is the Greek tragedy.

About the authors

Related content

The ECB and the Fed: a comparative narrative

Although the Great Recession was viewed as a US problem, the Eurozone was affected by it from the start. This column compares the monetary policy resp

Greece: a European tragedy

Wrapped up in the details of pension reforms and home foreclosure—matters that, no doubt, have important consequences for many— the big picture has fa

Delays and half measures

Are the eurozone’s continuing woes the result of its incomplete construction or because of policy errors in responding to the crisis?

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and