2014 Financial Odyssey

The European Banking Union matures in 2014, with the ECB assuming its role as single supervisor. This column outlines the transition to the new steady

This article was published in VoxEU.

The European Banking Union matures in 2014, with the ECB assuming its role as single supervisor. This column outlines the transition to the new steady state. This will involve a comprehensive balance sheet assessment, new rules regarding recapitalisation, restructuring, and resolution, and the determination of how recapitalisation costs are distributed across taxpayers in different European nations.

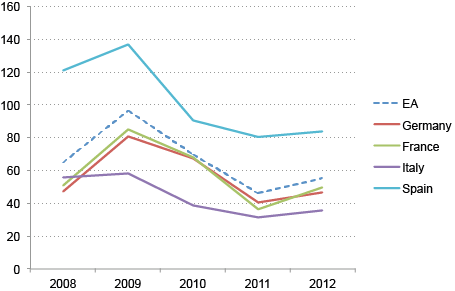

The year ahead will be one of major change for the European financial system. Decisions will be taken that will shape Europe’s banking system for years to come; for example, on whether to accept more or less cross-border bank consolidation. The European Banking Union will assume its definitive shape, while the ECB will become the single supervisor of Eurozone banks (ECB 2013). At present, investors have significant doubts about the quality of banks’ assets and the potential losses still hidden in their balance sheets. Market-based valuations of banks in Europe suggest that investors’ confidence remains low.

Figure 1 Price/book ratio (%)

Note: The data are computed as the un-weighted average of the largest five banks in each respective country.

Source: SNL Financials and Bruegel computations.

The implementation of single supervision could greatly reduce these concerns. The far-reaching preliminary assessment of banks’ balance sheets that will be conducted during 2014 can make balance sheet information more transparent, comparable and credible. For this to happen, some major uncertainties need to be addressed.

First, the central elements of the ECB’s balance sheet assessment exercise need to be clearly communicated. The ECB has already outlined the broad structure and some important technical elements (ECB 2013). The assessment will involve all banks to be directly supervised by the ECB – about 130 banks in 18 Eurozone countries – accounting for approximately 85% of total Eurozone bank assets. The comprehensive assessment will be undertaken by the ECB based on the transitional arrangements laid out in Article 33.4 of the SSM regulation. National authorities and the credit institutions concerned will supply the necessary information as requested. According to the ECB, the assessment has three elements:

- A supervisory risk assessment addressing key risks in the banks’ balance sheets, including liquidity, leverage, and funding.

- An asset quality review examining the asset side of banks’ balance sheets as of 31 December 2013. All asset classes, including non-performing loans, restructured loans and sovereign exposures, will be covered.

- A stress test building on and complementing the asset quality review by providing a forward-looking view of banks’ shock-absorption capacity under stress.

The ECB will set capital thresholds as a benchmark for the outcomes of the exercise amounting to 8% Common Equity Tier 1 (CET 1). The threshold is decomposed to 4.5%, which is the ratio that will be legally mandatory as of 1 January 2014 according to Capital Requirement Directive1 and the Capital Requirement Regulation,2 a capital conservation buffer of 2.5%, and an add-on of 1% to take into account the systemic relevance of banks. There is still some uncertainty regarding the definition of capital because of the various transition periods in the CRD IV and the timing of the ECB exercise (for details, see Merler and Wolff 2013).

There are also a number of crucial issues that remain to be settled. These include, in particular, the treatment of sovereign debt, the magnitude of the stress test and the treatment of systemic risk. The choices to be made on these issues will potentially affect the results significantly. In fact, the lack of information about the balance sheets of banks, together with the uncertainty about these central parameters of the exercise, can probably explain the significant variance in market estimates of the recapitalisation needs that might be identified by the stress tests for the Eurozone banking system. The estimates that we could collect in Table 1 vary between €50 billion and €650 billion, depending on the different way systemic risk is accounted for (Merler and Wolff 2013).

Table 1

| Source | Estimation (billion euros) | Publication date |

|---|---|---|

| Credit Suisse | 50 | 16/10/2013 |

| Goldman Sachs | 75 | 31/10/2013 |

| Standard & Poor's | 95 | 08/11/2013 |

| PricewaterhouseCoopers | 280 | 28/11/2013 |

| VLAB | 652 | 23/11/2013 |

Source: Merler and Wolff (2013), based on company reports.

Considering how crucial such variables are for the formation of market expectations ex ante – and for the credibility of the stress tests ex post – it will be important for the ECB to be as transparent as possible, as early as possible.

Once the exercise is underway, the ECB should not shy away from forcing non-viable banks into restructuring, standing ready to provide large amounts of liquidity to the remainder of the financial system if needed. We acknowledge that this could lead to short-term volatility in financial markets, but this should be weighed against the cost of a persistently weak and dysfunctional banking system and the value of the credibility of the ECB as a supervisor and a monetary authority.

Second, uncertainty remains over the rules that will apply to bank recapitalisation, bank restructuring, and bank resolution in 2014 and after. If a recapitalisation need is identified, decisions will need to be taken about how to meet it. Currently, the main guiding framework is national decision-making authority, with some harmonisation introduced through the amended state aid framework. This regime could lead to significant differences between countries and could thereby deepen financial fragmentation. In this context, the discussion on bail-in is likely to remain topical during 2014.

To credibly break the link between banks and sovereigns, creditors need to be more involved in the sharing of the burden than during most of the last five years. But at the same time, the rules applicable to bail-in should be the same in different countries in order to avoid competitive distortions. The modified state-aid regime de facto introduces bail-in of junior debt as a precondition for accessing public funds for bank recapitalisation, and the BRRD will introduce tougher requirements from 2016. The new steady-state system should be based on strict and clear rules, and decisions on bail-in, bank restructuring, and resolution should be based on rules that limit discretion and prevent different approaches in different countries. However, policy discretion will always be exercised in some exceptional cases in order to prevent major systemic fall-outs from bail-ins. Which entity will exercise this discretion and how it will do so is a matter of great importance.

Discretion should be exercised by a European resolution authority. Relying on national authorities can only lead to major differences and applications in different countries, thereby undermining financial integration and reinforcing the re-nationalisation of finance that has been seen in the last few years. This is not only sub-optimal, but also undermines monetary integration to the extent that the fragmentation of financial markets along national borders hinders the transmission of the single monetary policy. To credibly break the link between banks and sovereigns, the Eurogroup should agree that the same rules be applied to bank recapitalisation and creditor involvement in different countries, also during the transition.

Finally, a crucial question is how remaining recapitalisation costs should be distributed between national taxpayers and taxpayers of other European countries. Governments should support the ECB in its efforts to restructure and bring the banking system back to health. Most importantly, governments should accept and support cross-border bank mergers when sensible (Sapir and Wolff 2013). They should also be ready to recapitalise banks where necessary. During the transition to the new steady state, national taxpayers will inevitably shoulder most of the burden. But in the steady state, in order to credibly break the vicious cycle between banks and sovereigns, a European insurance scheme for the major risks combined with a contribution from national taxpayers is needed. A clear commitment to a single resolution mechanism with an appropriate common backstop is important to reverse banking re-nationalisation, keeping in mind that a resolution fund, even when fully built-up, needs to have a common fiscal backstop to be credible. Moreover, the transition period should be limited in duration so as to avoid prolonged financial fragmentation with unavoidable negative implications for growth and jobs.

References

ECB (2013), "ECB starts comprehensive assessment in advance of supervisory role", ECB Press Release, 23 October.

Merler, S and G Wolff (2013), “Ending uncertainty: recapitalisation under European Central Bank supervision,” Bruegel Policy Contribution 2013/18.

Related content

The European defence industrial strategy: important, but raising many questions

The European defence industrial strategy helps to focus thinking but has significant flaws

Use the financial system to enforce export controls on Russia

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up