Chinese banks: the way forward

Despite the economic downturn the Chinese banking system continues its expansion. Concerns are rising about the institutions' strenght, as bad loans c

Where is the Chinese banking sector coming from?

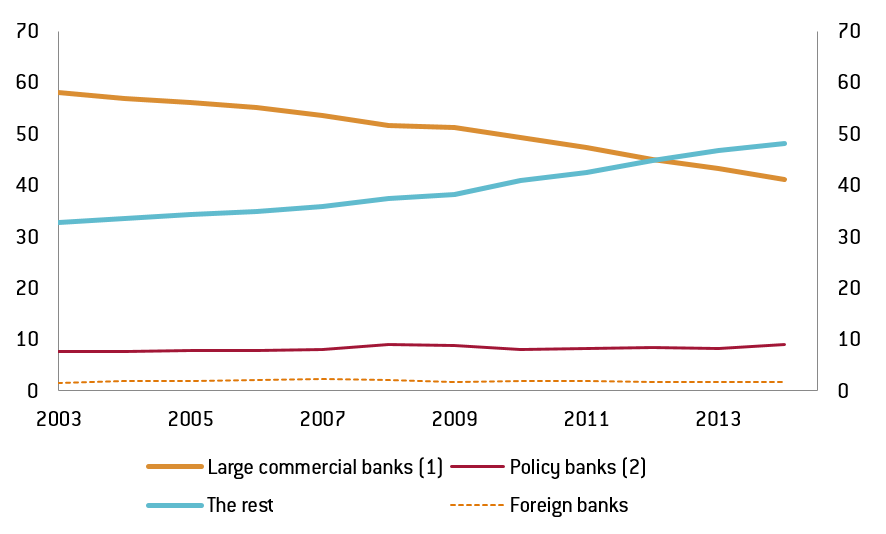

China’s banking system was deemed monolithic, with the central bank People's Bank of China (PBoC) as the major entity authorized to conduct operations until the early 80s when the government started opening up the banking system and allowed four state-owned banks to take deposits and conduct banking business, which include Industrial & Commercial Bank of China (ICBC), China Construction Bank (CCB), Bank of China (BOC) and Agricultural Bank of China (ABC). As the economy skyrocketed in the past few decades, China’s financial system has grown exponentially. The assets managed by banks once grew more than 25% a year during the period of the massive fiscal stimulus plan to combat the global financial crisis (2008-2009) but also before and after that period. At the same time that massive credit boom is also showing on the quality of bank assets. In fact, total bad loans reached 1.27 trillion yuan at the end of 2015, the highest since the global financial crisis, on the back of an economic slowdown and a ballooning corporate debt. All in all, one can argue that the banking sector is becoming the Achilles' heel of the Chinese economy once again, as happened in the past. Chinese public banks are particular hit hard amidst the rise of non-bank financial institutions and rural banks. In fact, Chart 1 shows that the assets managed by large commercial banks have been dropping over years from nearly 60% of total assets in system in 2003 to about 40% in 2014. Yet compared with non-bank financial institutions and rural banks, large commercial banks generally still enjoy the support of the state, which still brings enormous benefits. The latest example can be found in the rumours saying seven listed Chinese banks may have received permission to lower their coverage ratios.

Chart 1 - Total assets of banking institutions (% of total)

Source: CBRC, Natixis

Where is bank credit heading?

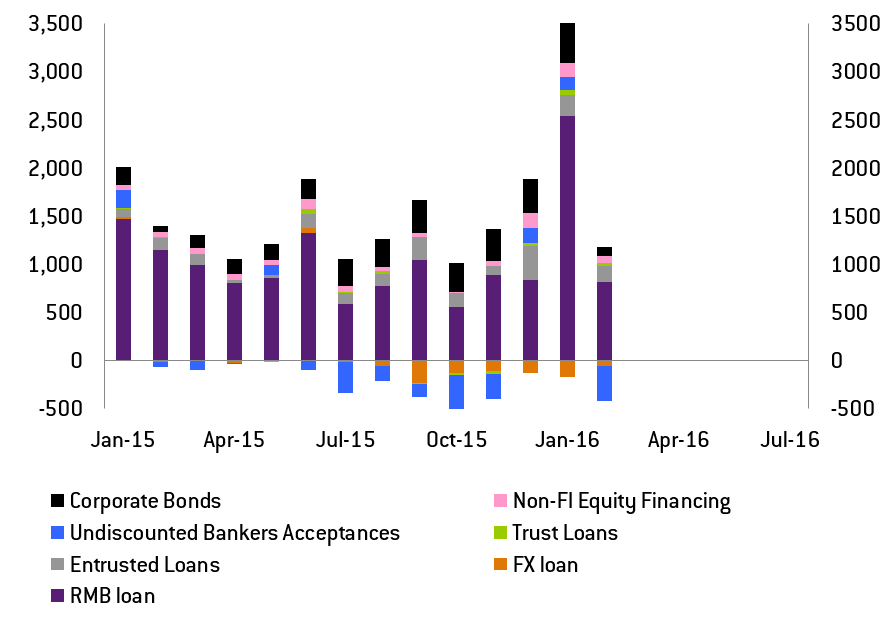

Notwithstanding the slowdown of the Chinese economy, bank credit has continued to expand quite rapidly. This includes both official bank credit but also the shadow banking. Only in the first two months of 2016, bank credit rose a significant 28% to RMB 3351 billion compared with the same period in previous year. When adding corporate bond issuance and shadow banking, total credit expansion in the economy totaled RMB 4200 billion in January and February, a 23% increase from the same period in 2015 (see Chart 2). Such growth is clearly very high when compared with nominal GDP growth, which remained below 6% in 2015. In particular, net issuance of corporate bonds skyrocketed (up 117% from 2015) but its size is still limited compared to bank financing. This signals a very high demand for credit in the whole financial system of China and also the massive leveraging that the economy is undergoing, especially the corporate sector.

Chart 2 - New Total Social Financing (RMB bn)

Source: Bloomberg, NATIXIS

Laxer monetary policy is of course helping towards such rapid credit growth. It seems that the last instruments used by the PBoC to ease (i.e. large scale injections of liquidity through reverse repos) have been the most effective in pushing banks to lend. The problem is that it is very hard to avoid leveraging continuing to pile up, even in sectors which are now to suffer from overcapacity and, thus, with very little capacity to repay.

Over all, the outcome of the Annual Party’s congress last month has made it very clear that growth is the key target and that the rest, including excessive leverage, is to subsidiary to that. This was confirmed by the surprising move of the People’s Bank of China (PBoC) cutting the required reserve ratio (RRR) by 50 bps effective from March 1st, 2016. This reflects the central bank is keen to ease liquidity in the China banking sector. The central bank may then need more window guidance to commercial banks to ensure this additional liquidity would not be directed to save zombie corporates in overcapacity industries. The high bank loan growth was also amplified by the fact that zombie corporates rushed to get credit before the PBoC announced that banks could not grant loans to unapproved projects taken by zombie corporates, which however seems hard to implement given the overwhelming importance of the growth target.

How much are Chinese banks being hurt by the slowdown?

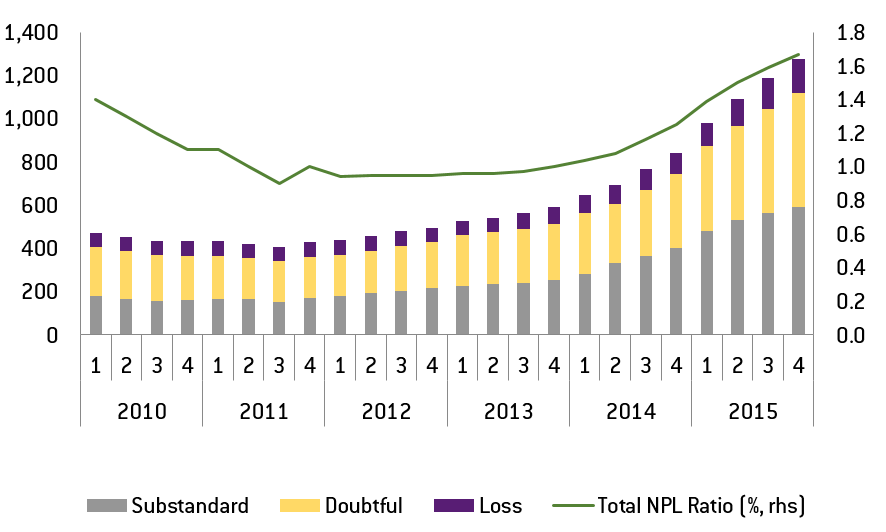

The extensive credit expansion in January and February, especially from the banking sector, has several implications. First, it masks the growth of the non-performing loan ratio as the denominator has experienced such a big increase (see Chart 3). Second, such surge in credit granted must have had a surge in demand as well. Whether that new demand reflects an improvement in the economy or simply more financing needs is a key question. If it is the latter then it reflects an increasing demand for new funds to repay outstanding loans.

Chart 3 - NPL in Chinese Commercial Bank by Type (RMB bn)

Source: Bloomberg, NATIXIS

Having said that, China had a bad-loan coverage ratio of 150%, which is considered high for international standards. However, there is rumor that this will be lowered to 120%. In any event, credit risk is rapidly rising in China as the economy slows down and financial conditions are lax enough for corporates to continue to leverage. The question, thus, is how weak are Chinese banks in the current circumstances.

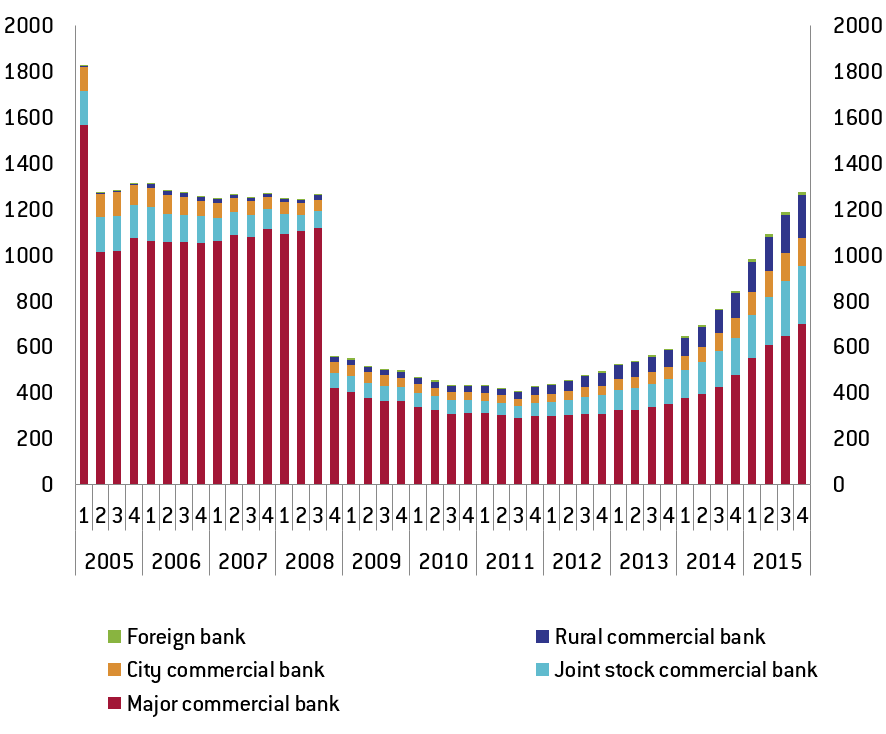

We cannot take banks in the whole China banking sector as homogenous. For the banking sector as a whole, pre-provision profits and cash loan loss reserves are enough to charge off bad loans as the average coverage ratio is 235%. This basically means that large banks should be quite prepared for the current economic downturn. However, city commercial banks and rural commercial banks may experience accelerating credit costs, especially if their lending has concentrated on the excess capacity sectors (see Chart 4). As for the risk of contagion through a liquidity channel, the PBoC has swiftly moved to daily open market operations which lower the risk of a liquidity crisis.

Chart 4- Amount of NPL in Chinese Commercial Banks by Type of Bank (RMB bn)

Source: Bloomberg, NATIXIS

The more important factor to assess future profitability of Mainland banks would be the net interest margin (NIM). The reality is that NIM has already dropped quite aggressively in the last few years. It was only 2.54% at the end of 2015 from 2.70 in 2014. However, as the central bank tries to help banks through lower funding costs via open market operations, the NIM in 2016 may actually not be as thin as expected.

Beyond bank the credit quality from bank loans and profitability from NIM, Chinese banks could also be hurt by defaults on wealth management products (WMPs), which are closely related to shadow banking. Shadow banking includes many activities, from undiscounted bankers’ acceptance, trust products, entrusted loans to P2P lending. Different shadow banking activities incur different level of credit risks. The problem is complicated by the fact that many of shadow banking products are securitized and sold as part of wealth management products by banks and trust companies. Investors in Mainland would demand banks to repay their investments when the wealth management products default. As credit risk is rising, the same happens with WMPs and, thereby, the likelihood of banks having difficulties to pay back their customers in times of product default.

Recently, due to market sentiment of FED’s rate hike and a stronger dollar, Mainland corporates tend to repay their offshore loans in foreign currencies. This has affected some Mainland banks that have offshore branches, especially for Mainland banks in HK, in the respect of shrinking loan book. However, as the Belt and Road Initiative is still on-going, we expect that Mainland banks would be able to take advantage of the “going out” project financing. This is especially positive to big banks that have branches outside China.

New threats to Chinese banks: new players

Mainland banks have put their business focus on corporates for many years. Until 2014, lending to households was virtually limited to mortgages. The space to lend to SMEs was also limited as large corporates had enough appetite to drive a very rapid loan growth anyway.

Part of the household and SME needs have been filled by fintech companies. Leveraging on their big data capabilities, as well as loose regulation, they are providing flexible personal finance products to the younger generation in the Mainland. Still, fintech is still only a complement to banking services but the competition for banks is clearly increasing. In response, some commercial banks have developed their own fintech subsidiaries. The most renowned representative is Ping An’s P2P lender Lu.com (previously known as Lufax) which recently raised US$1.2 billion by selling about 5 percent of stake, making it one of the world’s most valuable financial technology startups. Given the rapid development of the industry, it would be interesting to see how would regulators keep up with the evolution and set a regulatory framework.

All in all, it seems clear that the Chinese banking sector, which has become massive – even for China’s huge economic size – will have to navigate difficult waters in the next few years. The key risk is coming from corporate borrowing and, to a lesser extent, from the reduction of profitability stemming from financial liberalization and heightened competition. As Chinese banks’ linkages with the rest of the world have grown enormously in the last few years, it seems clear that the health of the Chinese banking sector will remain a topic of interest for years to come.