Supply policies at the zero lower bound

What’s at stake: While the benefits of structural reforms are largely undisputed in the long run, several authors consider that reducing mark-ups and

Structural reforms in the Great Recession

Gauti Eggertsson, Andrea Ferrero, and Andrea Raffo write that conventional wisdom among academics and policymakers suggests that structural reforms that increase competition in product and labor markets are the main policy option to foster growth. But the short-run transmission of reforms depends critically on the ability of the central bank to provide monetary policy accommodation. In normal times, reforms increase agents’ permanent income and stimulate consumption. Amid falling aggregate prices, the central bank cuts the nominal interest rate and the currency union experiences a vigorous short-term boom. These effects, however, are completely overturned in crisis times. When the central bank’s nominal interest rate is at the ZLB, reforms are contractionary, as expectations of prolonged deflation increase the real interest rate and depress consumption.

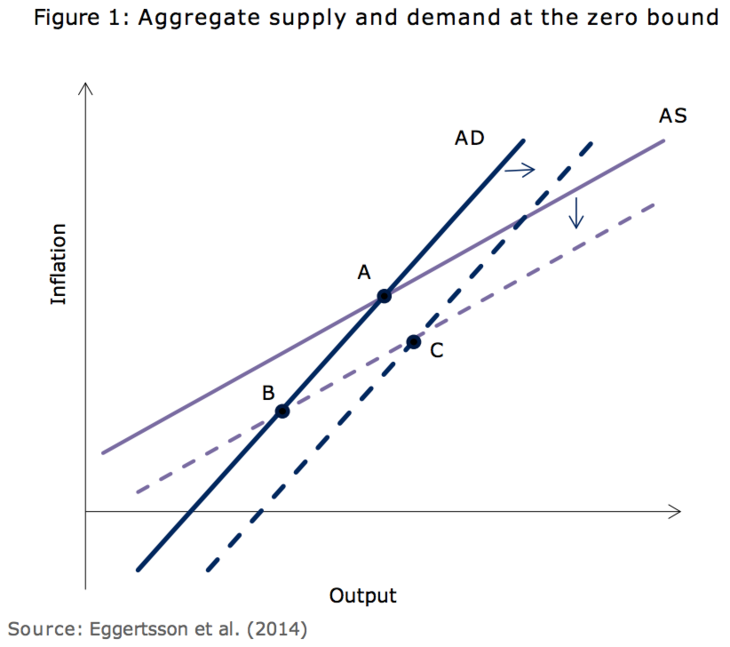

Lukas Vogel writes that product and labor market reforms that shift the level of potential output have two effects in the stylized diagram below: First and foremost, the AS schedule shifts downwards as the upward pressure on costs and prices declines for any level of output. Second, the AD schedule to the right, because expected increases in wealth and investment profitability strengthen consumption and investment demand for given levels of current inflation and real interest rates. It is the first effect, i.e. the standard AS shift, which is contractionary in the ZLB environment. It raises real interest rates and, hence, weakens interest-sensitive aggregate demand. In Figure 1 it moves the economy to point B. The second effect, i.e. the shift of the modified AD curve, is inflationary. In Figure 1, in conjunction with the AS shift, it moves the economy to point C. The relative strength of the two effects is ultimately a quantitative question.

Jesús Fernández-Villaverde, Pablo Guerrón-Quintana, and Juan F. Rubio-Ramírez write that it is true that increments in productivity in the current period make the problem of the ZLB worse. But, in practice, nearly all policies that increase productivity will have a considerable implementation lag. Hence, when we talk about supply-side policies, we are talking about future productivity increases. If this is the accurate way to think about structural reforms, then the net impact of structural reforms in the short run is positive. Outside the ZLB, increases in future productivity are undone, in terms of consumption today, by an increase in the interest rate that ensures market clearing in the current period. At the ZLB, that effect disappears and hence consumption today also rises.

Jesús Fernández-Villaverde, Pablo Guerrón-Quintana, and Juan F. Rubio-Ramírez write that the wealth effect mechanism works even if structural reforms generate just a one-shot increase in the level of productivity over its original path, rather than a permanent increase in the growth trend of an economy. Benoit Coeure writes that structural reforms should be frontloaded rather than applied in a staggered way. A one-off price adjustment has distributional effects ex post, but it does not affect the perception of real rates going forward – insofar as it boosts future income, it may indeed raise inflation expectations and lower real rates. By contrast, if adjustment is gradual, it creates disinflationary expectations and real rates increase. In other words, a slower adjustment makes the contractionary effect of reforms more prolonged.

Supply polices in the Great Depression

Gauti Eggertsson writes that the National Industrial Recovery Act (NIRA), which created distortions that moved the natural level of output away from the efficient level by temporarily increasing the monopoly power of firms and workers, may have increased rather than decreased output in 1933. Under regular circumstances, these policies are counterproductive. The NIRA is helpful because it breaks the deflationary spiral, by helping firms and workers to prevent prices and wages from falling.

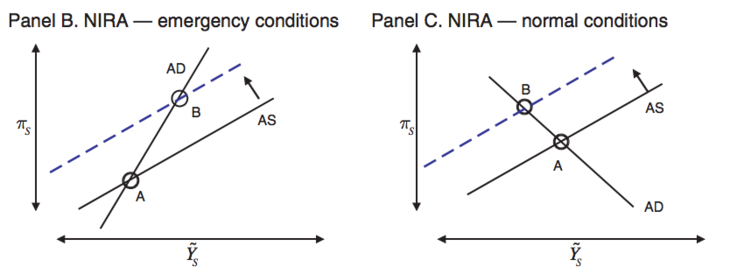

Jeremie Cohen-Setton, Joshua K. Hausman and Johannes Wieland write that this conclusion is striking both because it is an unavoidable outcome of taking the standard new Keynesian model seriously, and because it is at odds with a long-standing literature criticizing the supply-side elements of the U.S. New Deal. The authors note that if the NIRA were a positive for the U.S. recovery, then the French recovery from the Great Depression ought to have been strong since the Popular Front’s policies were an extreme form of the NIRA. The size of these supply-side shocks as well as their temporal isolation from demand-side policies make France from 1936 to 1938 a useful setting for the purpose of understanding the effects of supply-side policies in the Great Depression.

Jeremie Cohen-Setton, Joshua K. Hausman and Johannes Wieland exploit variation in the implementation of hours restrictions across industries in France and find that it caused a persistent 3-15% relative decline in the output of affected industries. While the authors can calibrate a multi-sector new Keynesian model to match these partial equilibrium estimates, the model generates implausibly large positive general equilibrium effects given the poor aggregate performance of the French economy. The authors present as an alternative a disequilibrium model that can reconcile the negative effect of supply shocks with a coherent view of macroeconomic behavior in a depressed economy with fixed nominal interest rates. In this model a high real wage prevents firms from accommodating higher demand, even when output is far below potential. In this environment, policies that raise inflation expectations without raising real wages will be expansionary, while policies that raise inflation expectations and raise real wages may not be.

Bruegel Economic Blogs Review is an information service that surveys external blogs. It does not survey Bruegel’s own publications, nor does it include comments by Bruegel authors. We, exceptionally, deviated from this policy this week.