Blogs review: Revisiting the case for rational expectations

What’s at stake: The debate about what determines the expectations of economic agents and what model of expectations to use in macroeconomic mode

What’s at stake: The debate about what determines the expectations of economic agents and what model of expectations to use in macroeconomic models has been central to economics since the 1970s. Rational expectations, equal to the statistical expected values of the variables in question, opposed to adaptive expectations that are determined by past observations of the variables, were a central component of the New Classical critique of Keynesian economics and the debate has been active ever since. Recently, a post by Lars Syll, in which he attacks Simon Wren-Lewis for his continued defence of rational expectations, has provoked a reaction by Wren-Lewis, sparking a debate involving heterodox and mainstream economists.

The importance of past and present information

Lars P Syll argues that Rational Expectations could only apply to a fictitious, ergodic world governed by stable and stationary stochastic processes. In the real world, however, the future is to a large extent unknowable and uncertain. Structural breaks and regime shifts occur, time and history matter. Events may not be caused by time-invariant stochastic processes with stable probability distributions. Under those circumstances, it is quite possible for agents to make mistakes that turn out to be systematic.

Simon Wren-Lewis writes that if he were to focus in detail on how expectations were formed and adjusted, he would turn to the large mainstream literature on learning. The validity of macroeconomic ideas should be checked within realistic learning environments. However, for modelling purposes, more simplicity is required. One essentially has the binary choice between rational expectations or naive agents with something like adaptive expectations. The problem with adaptive expectations is that they come down to assuming that expectations depend solely on past observations, without regard for monetary policy and the current state of the economy. Given the importance of decisions based on expectations, that seems too simplistic.

Robert Waldmann finds it obvious that it is better to assume adaptive than rational expectations when attempting to model advanced industrial economies and to guide policy. It is plainly true that most economic agents in the USA quite clearly ignore what economists and the media say about inflation. And under naive expectations, irrational speculative bubbles will arise, in which agents assume some asset price will increase because it has in the past. That is consistent with the data (but the data can also be reconciled with the rational expectations assumption. The problem is – any data can be reconciled with it: It is not a falsifiable theory).

In an older article, David Levine writes that he does not think there are viable alternatives to rational expectations in economics despite the resultant inability to predict crises. This “uncertainty principle” in economics is due to the fact that under any form of expectations other than rational expectations, a theory built on those expectations would be wrong once people start to believe and act upon it (this is essentially the Lucas critique).

Simplicity in models and agents’ behaviour

Simon Wren-Lewis argues that while rational expectations may seem a strong assumption, the approach resembles that of microeconomics to other subjects: Firms may not know the true demand curves for their products, yet the assumption of profit-maximising prices may be a better approximation to how they choose prices than a model where they have a fixed mark-up on costs. So it also seems consistent to also assume that agents use relevant and available information to generate expectations when those expectations matter. And how else would one make sense of a whole forecasting industry, and the newsworthy character of macro forecasts?

Mark Thoma takes a measured view of rational expectations. On the one hand, it would be foolish to assume people didn’t use new information and purely extrapolated from past trends. Who would assume a trend will continue when there is good information saying otherwise? And one should think that people will react to announced changes in policies. On the other hand, it is quite a stretch to assume that people fully understand the policy rules used as well as how they will impact the economy. Simplifications, rules of thumb or hard-wiring may explain quite a bit – e.g. why we can catch a ball in flight without solving complicated differential equations – and the correction of individual errors on markets may explain even something more, but it is to be doubted that it extends to fully approximating the functioning of complex markets. Rational expectations may be a good benchmark, just like the assumption of a perfect vacuum in physics, and may approximately hold in some contexts such as simple games and financial markets. However, it would be a mistake to assume they apply universally.

Nick Rowe writes that one should expect people to use rules of thumb in reality. This is a rational strategy for individuals as long as the world is well approximated by the rule used. For any naive way of forming expectations, there exists a world in which that naive way of forming expectations would be rational. In a world where the price level followed a random walk - something like the Gold Standard world - the naive expectation of 0% inflation is rational. In a world where the price level followed a random walk plus 2% drift, roughly a 2% inflation target world, the naive expectation of 2% inflation would be rational. And if the inflation rate followed a random walk, the naive expectation that next period's inflation rate would be the same as last period's inflation rate would be rational. It's when the world changes that things get tricky. The naive expectations that were rational in the old world aren't rational in the new world. This comes down to an argument for small c-conservatism in monetary policy rules and elsewhere in order to keep expectations rational for longer than they otherwise would be.

Expectations and data

Robert Waldmann points out that the Michigan Survey (inflation expectations of ordinary people) shows that inflation expectations are closely correlated to current CPI inflation – except when large external shocks such as oil price shocks occur. And in recent years, survey forecast inflation is persistently higher than actual inflation – while people’s estimates of current inflation also exceed actual figures. This does not seem in tune with rational expectations either and rather point towards backwards-looking expectation formation.

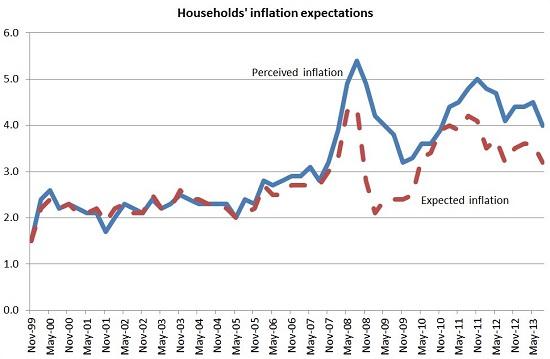

Source: Stumbling and Mumbling / Chris Dillow, using Bank of England data

Chris Dillow points out that in the data, expected inflation and perceived inflation are strongly correlated. While this may be consistent with some rational expectations, it is also largely consistent with a simple rule of thumb: expect inflation to be what it is now, but adjust down if inflation is unusually high, and up if it's unusually low. However, this rule of thumb does not seem to hold for exceptional circumstances. During the recession, inflation expectations were lower than those this rule of thumb would generate. Maybe, it is reasonable to suspect that inflation expectations are indeed formed by backward looking simple rules of thumb in normal times - but in exceptional times, people abandon rules of thumb for more complex processes as the costs of being wrong increase.