Covid19 and emerging economies

What to expect in the short and medium term? Covid-19 will consequently push for a quick reshuffling of the global value chain away from the emerging

Covid-19 dramatically worsening the economic outlook for emerging economies

Covid-19 has ravaged the Chinese economy in the first quarter of the year and it is now doing the very same with Europe and the US. As the epidemic of the first wave of coronavirus outbreak hit, China’s GDP shrank by 6.8% in the first quarter of the year. The coronavirus has led to vanishing domestic demand with local retail sales particularly hit together with a rapidly worsening labour market in terms of a higher unemployment rate and collapsing disposable income. With production resuming in China, one necessary consequence of the collapse in demand versus recovering supply is growing deflationary pressures, which might soon be spreading into the global economy through cheaper Chinese exports.

The situation is much similar in the EU and US. Business confidence has slid significantly with the PMI for the eurozone and the US diving into contraction territory in March. Lockdowns and production disruptions are contributing to significant job losses, dragging down household income and consumption. As in China, plummeting demand is contributing to rapid reduction in consumer prices both in the US and the EU.

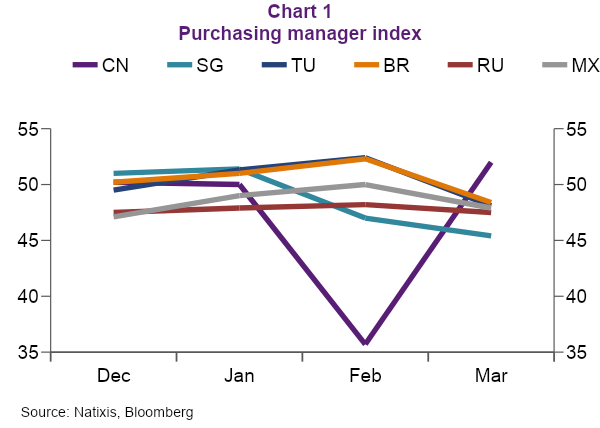

The third wave of the pandemic is reaching the emerging world. In particular, Turkey, Brazil, Russia, India, Singapore and Mexico have seen rapid contagion, pointing to a new wave of coronavirus outbreak. Emerging countries are facing the pandemic with more limited public health capabilities. Also, overcrowded cities and informal labour markets are adding extra complications. While the number of Covid-19 cases as well as the number of deaths are very different across countries and still in relative control compared to the EU and the US, the negative economic impact is increasingly obvious. Sentiment came down in March, as shown by the Purchasing Manager Indices in several emerging countries except China, which has seen a V-shaped recovery since February, the peak of the outbreak (Chart 1).

Since March though, emerging economies have gradually moved towards tighter mobility restrictions as cases started to rise faster. For instance, India has extended its national lockdown to May 3 to curb the wide spread of contagion and the Philippines has done the same until May 15. The lack of mobility is set to weigh on the economic outlook of emerging countries, as has been the case for China and other Asian economies in the past. In fact, the IMF is expecting the emerging world to enter a recession of -1% in 2020, which is a far worse economic performance than in the aftermath of the global financial crisis in 2008.

Fragilities beyond the pandemic: commodity and dollar dependence

Beyond the impact of Covid-19, two more shocks are hitting the emerging world. The first is the collapse in oil prices and the second is related to a sudden dollar shortage globally. As regards oil, the sudden fall in prices followed the breakup in the dialogue among members of the Organisation of the Petroleum Exporting Countries (OPEC) and Russia. OPEC, led by Saudi Arabia, decided, in early March, to conduct a massive increase in oil supply, which Russia disagreed with. This decision was reversed in only a month, with an agreement by OPEC, the US, Mexico and Russia to reduce oil supply collectively by 22%. However, demand meanwhile has plummeted due to very limited mobility worldwide and the incoming recession. With a fall in prices of over 60% and a momentary – but telling – negative price in oil futures, oil exporters have seen their external and fiscal revenues collapse. The situation is not much better for other commodity prices.

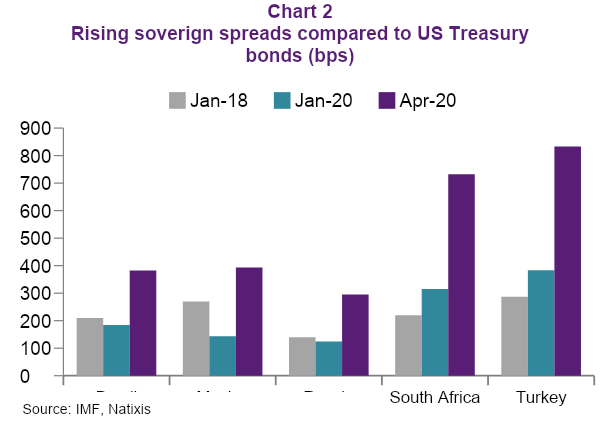

As if this were not enough, the rapid spread of Covid-19 to Europe and, especially the US, brought about a sudden increase in global risk aversion and, thereby, the collapse of global financial markets. Emerging market financing costs are known to be very dependent on the degree of global risk aversion given their dependence on external financing and the inability to issue hard currency. A clear reflection of this is the rapid increase in sovereign spreads since March (Chart 2).

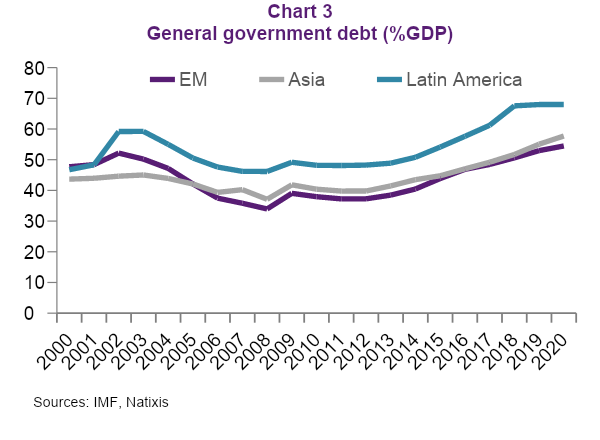

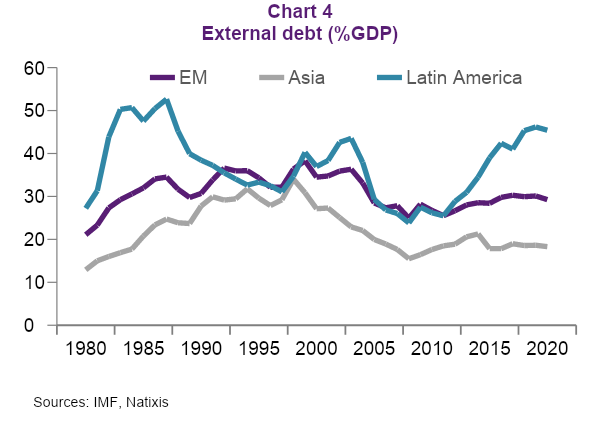

Among emerging economies, Latin America stands out as much more fragile than average and, even more so when compared with Asia. In fact, debt levels have increased across the emerging market space but much more so in Latin America (Chart 3) and the fiscal space remains limited across the board, even in China. This is even more problematic when focusing on external debt (Chart 4) where Latin America clearly stands out pointing to a much higher dependence on external financing.

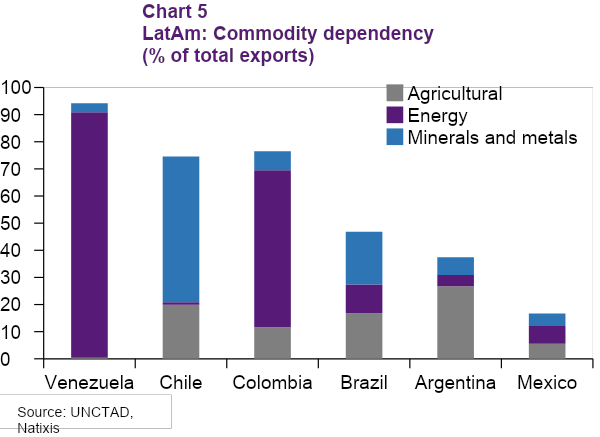

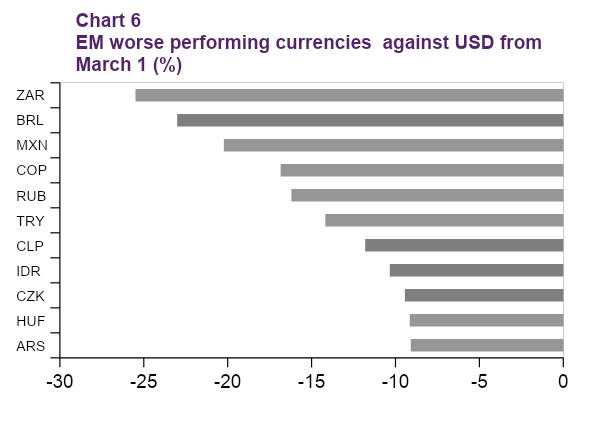

Elevated government debt burdens in Latin American countries are accompanied by high dependency on commodities. Chart 5 shows the contribution of commodities to total exports for major Latin American countries, which gives a sense of how badly the region will be affected both in terms of its external and fiscal finances. All in all, the risk on emerging economies is clearly understood by the market which has been dampening its currencies since March (Chart 6).

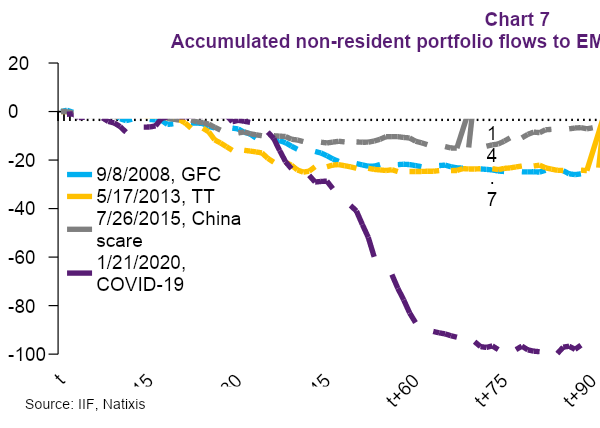

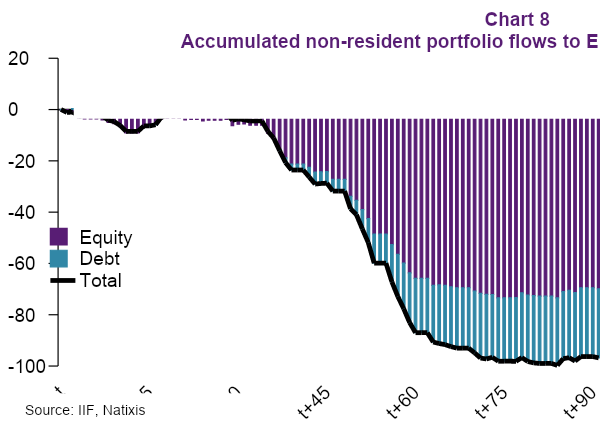

The sudden stop in capital flows into emerging economies has been unprecedented (Chart 7). In fact, not only has there been a sell-off in USD denominated corporate credit from emerging markets but also a sudden exit of foreign investors in local-currency sovereign debt markets, which had long been thought to be more resilient to global risk aversion (Chart 8). In addition, exports – especially commodity exports – but also more generally have collapsed in the light of the incoming global recession. Revenue from international tourism has plummeted in the light of travel bans and even remittances are being hurt as migrants are seeing their incomes cut and their jobs lost. Against such backdrop, the International Monetary Fund (IMF) estimates that total gross financing needs of emerging markets could be as much as 2.5 trillion dollars. This is very much in line with the IMF having received requests for financial assistance for as many as 100 members already with a good part of these needs concentrating in a few systemic emerging markets.

How can emerging markets protect themselves from the external financing shock?

The most immediate way for emerging economies to react to a shock in external funding is to use domestic policies, both monetary and fiscal. Unfortunately, the fiscal room tends to be limited. As for monetary policy, some emerging economies may be pegged to the USD so they need to put up with its strength, no matter how costly. Those with floating exchange rate regimes, though, may still find it difficult to use their monetary space fully since their currencies have already weakened quite substantially against the USD while suffering from capital outflows. The fear of floating at a time of massive outflows from emerging economies is understandable, all the more so given the large negative balance sheet effects which excessively cheap domestic currencies can bring about in countries with large dollar liabilities.

The obvious shortcut is to introduce capital controls. While the general consensus is changing towards a more favorable approach to capital controls, there is an undeniable cost associated with introducing capital controls, at least for those emerging economies with market access, namely. losing such access. No matter the degree of dollar shortage we are already facing, Indonesia, the UAE, and Qatar have recently tapped the bond market with strong investor interest. The introduction of capital controls would immediately push investors away with serious consequences for dollar liquidity and, thereby, growth.

Barring the scenario of strict capital controls with the risk of a cut off from international financing, other tools are needed to address the impact of Covid-19 on dollar funding. The first line of defense is, of course, in full control of the country itself- namely tapping the forex reserves that emerging countries have accumulated over time for rainy days. Such self-insurance, though, is not evenly distributed across the emerging market space. Only a few economies can safely claim that their reserves are massive enough to deal with the shock. Most importantly, they tend to be concentrated in two main regions, Asia and the Middle East, with more than half of the USD 22 trillion forex reserves globally.

Other ways to address external financing constraints are regional insurance schemes, which again tend to concentrate in Asia, with a set of bilateral swap lines since the 1997 Asian financial crisis which has been increasingly multilateralised into the so-called the Chiang Mai Initiative Multilateralisation (CMIM). Other regional insurance mechanisms have been discontinued once the crisis they were created for waned. This is the case with the Vienna Initiative for euro liquidity outside of the eurozone. However, the recent announcement of a euro precautionary swap arrangement between the European Central Bank (ECB) and the Croatian National Bank for the remaining of 2020 is a good sign that countries pegged to the euro might be able to tap euro liquidity from the ECB.[1] In other regions, such as Latin America, the institutional framework to pool reserves is there, such as the Latin American Reserves Fund (FLAR under the Spanish acronym) has never fulfilled its mission.

Beyond self and regional insurance devices, the Federal Reserve has stepped up its existing bilateral swap lines with a selected group of central banks and reinstated those that were set up in 2008 and discontinued after the crisis. It should be noted that only two of the central banks are for emerging economies, Brazil and Mexico[1], with two additional cases depending on how emerging markets are defined, namely South Korea and Singapore. In addition, a repo line was announced for a larger number of central banks to access dollar liquidity by pledging US treasuries. While welcome, it seems clear that the Federal Reserve will not become a lender of last resort of the emerging world, due to well-known moral hazard problems. The best candidate to play that role, albeit in a limited way and under conditionality, is the International Monetary Fund (IMF). Unfortunately, the resources that the Fund has available are some USD 800 billion, which fall far short of the estimated needs for the 100 countries which have already requested financial assistance (around US 2.5 trillion). The needs for systemically important financial institutions are such that there is a huge risk that smaller, but poorer countries, cannot access IMF funding at a time when their debt is increasing. According to the IMF's estimate in the April Fiscal Monitor, the average debt ratio of low-income economies has increased rapidly by 9% within the past 5 years to 43%. This is the reason why the G20 has recently agreed to grant the funding to reduce their debt by USD 20 billion through the International Monetary Fund.

Beyond the short-term: the reshuffling of the global value chain

Beyond the short-term problems of fiscal sustainability and dollar access, Covid-19 will have important structural consequences on emerging economies in a number of directions. First, the way in which the global value chain operates today is being put into question. Supply disruptions, both in the production and export of goods, have generated doubts about the model. In addition, the pandemic has raised questions regarding over-dependence of a particular country, namely China.

China has long been the centre of global value chains and the lockdown transmitting to global production with massive disruptions. Over the last decade, the world has become more dependent on its intermediate goods for exports, meaning the world is more exposed to disruptions from China. In 2003, 8% of global export of manufacturing came from China – and by 2018 it grew to a staggering 19%. Moreover, China's dominance in sectors ranging from machinery, electrical parts, furniture and apparel parts is even higher. At the value chain level, China’s rapid vertical integration means that more of Chinese intermediates are used in the global value chain than in the past. What is key is that its exports of intermediates used by the rest of the world for export inputs have risen significantly since 2003 from 24% to 32% of exports. Apart from the over-dependence of the global value chain on China, China is rapidly integrating its value chain, driven by China’s reduced dependence of foreign intermediates for its reports. More self-reliance or vertical integration, with the world more dependent on its intermediate goods for exports while buying less inputs from the world, means that the world is even more exposed to China.

In light of this significant concentration risk, some governments are starting to advise their companies to re-shore or near-shore their companies away from China back home or elsewhere. Japan announced a supply chain relocation plan of JPY 220 billion to subsidise companies with high reliance over external supply chains to move back to Japan to prevent future production halts. This includes a JPY 23.5 billion subsidy to diversify the external supply chain to Southeastern counties, which is expected to cover mask production, automobiles, electronic equipment and medical supplies industries. The US has also called for moving back production chains with potential tax punishment for those companies not relocating. It is conceivable to think that distance to production will be shortened and that the most important part of production, on a strategic basis, will be redirected to their places of origin.

Such reshuffling of global value chains can be an opportunity for emerging market countries to benefit. Other than nearshoring to ASEAN countries, with Vietnam as the main winner so far, one can think of nearshoring to Mexico for the US and Canada and to Eastern Europe for Northern and Central Europe. Within Asia, Vietnam cannot possibly be the only beneficiary as its size is not large enough. India can capture some of China’s labor-intensive and even medium-tech manufacturing. For medium-tech and capital-intensive manufacturing, Thailand is best positioned thanks to the best in class general business environment and infrastructure. Malaysia and China are also both strong.

Another important change will be the reduction in people to people mobility with a massive impact on certain sectors, such as airlines and tourism. The fear of further contagion has led to stricter border controls or closure as well as policies to restrict movement domestically. This will impact some emerging economies much worse as they are heavily dependent on tourism for sources of income and growth. This is clearly the case with Thailand and the Philippines to a lesser extent. Hospitality is faced with sharp declines in occupancy rates and revenue, with the hardest hit on luxury hotels and first tier cities. Aviation is also hard hit.

Finally, strategic competition between the US and China is only growing as a consequence of Covid-19. Prior to the outbreak of coronavirus, the US-China relationship has featured trade confrontation with rounds of import tariffs being implemented, especially by the US. From trade, competition has moved to technology and the pandemic illustrates a new level of confrontation from diplomatic relations to the role of international organisations during the pandemic. More specifically, President Trump announced in mid-April that the US would halt funding to the World Health Organisation, accusing the WHO of failing to call out a lack of transparency from China and covering up the spread of the disease. On this basis, the chances of coordinated action to address the pandemic more effectively are very low.

Conclusions

All in all, Covid-19 is bound to have severe consequences in the short term but the structural ones may be even more important. After ravaging the Chinese economy in the first quarter, it is now crippling the US and European economies with the potential third wave in emerging markets. Increasingly tighter mobility control has started to take a toll on the infected countries’ domestic demand accompanied by a sluggish external outlook while emerging countries are under more pressure from plummeting oil prices, increasing fiscal vulnerabilities and global dollar shortage. Most importantly, the room for manoeuvre, both domestically and internationally, remains limited. Self and regional insurance are only large enough in Asia. As for the Fed, it can hardly act as international lender of last resort while it massively expands its balance sheet for domestic reasons. The IMF is the right institution to support emerging economies at the current juncture but it needs to be recapitalised as quickly as possible.

In the medium run, Covid-19 will have important structural consequences on emerging economies in a number of directions. First, the pandemic will push for a quick reshuffling of the global value chain away from China. This process has started even before the US-China trade war but it has accelerated since then and Covid-19 cannot but put further pressure in the same direction. Secondly, reduction in people to people mobility will have a massive negative impact in some sectors, especially aviation and hospitality, affecting those emerging economies which are most dependent on tourism. Finally, strategic competition between the US and China will only grow further as a consequence of Covid-19 so that emerging economies may be forced to take side with obviously negative – and potentially massive – economic consequences for them.

[1] It should be noted that Mexico, as well as Canada, have access to one more dollar swap line with the FED in the context of NAFTA but they account to a couple of USD billion and are thus, too small to be paid much attention.

Related content

Asia 2024 Outlook

China’s ‘new productive forces’ risk overcapacity bubble

India's economy can overtake China's if it can stay on track