Should the ‘outs’ join the European banking union?

This paper analyses the banking linkages between the nine ‘outs’ and 19 ‘ins’ of the banking union. It finds that the out countries could profit from

Highlights

- For political reasons, European Union member states’ opinions on joining banking union range from outright refusal to active consideration. The main stance is to wait and see how the banking union develops. The wait-and-see positions are often motivated by the consideration that joining banking union might imply joining the euro. However, in the long term, banking union’s ultimate rationale is linked to cross-border banking in the single market, which goes beyond the single currency.

- This Policy Contribution documents the banking linkages between the nine ‘outs’ and 19 ‘ins’ of the banking union. We find that some of the major banks based in Sweden and Denmark have substantial banking claims across the Nordic and Baltic regions. We also find large banking claims from banks based in the banking union on central and eastern Europe. The United Kingdom has a special position, with London as both a global and European financial centre.

- We find that the out countries could profit from joining banking union, because it would provide a stable arrangement for managing financial stability. Banking union allows for an integrated approach towards supervision (avoiding ring fencing of activities and therefore a higher cost of funding) and resolution (avoiding coordination failure). On the other hand, countries can preserve sovereignty over their banking systems outside the banking union.

1. Introduction

Banking union, which consists of the Single Supervisory Mechanism (SSM) and the Single Resolution Mechanism (SRM), was a reply to one of the root-causes of the European debt crisis: the sovereign-banking loop. The vicious circle linking the solvency of euro-area countries to the solvency of their banks contributed to the crisis. The sovereign-bank loop works two ways. First, banks hold on their balance sheets large amounts of the bonds of their own governments (Merler and Pisani-Ferry, 2012; Battistini et al, 2014). Consequently, a deterioration of a government’s credit rating would automatically undermine the solvency of that country’s banks. Second, a weakening of a country’s banking system could have implications for the government’s budget because of the potential for a government-financed bank bailout, and because of lower tax revenues resulting from the subsequent economic downturn (Angeloni and Wolff, 2012)1.

The euro area fell victim to the sovereign-bank loop because national central banks have given up control over the currency in which their debts are issued, putting the European Central Bank (ECB) in charge. To break the loop, a June 2012 summit of euro-area heads of state and government2 decided to move the responsibility for banking supervision to the euro-area level as a pre-condition for direct bank recapitalisation by the European Stability Mechanism (ESM)3. Moreover, the ECB was substantially exposed to banks because it was forced to provide them with liquidity without having supervisory control. If ex-post rescues are organised at European level, ex-ante supervision should also be moved to European level to minimise the need for such rescues (Goodhart and Schoenmaker, 2009). The essence of banking union is therefore supervision and resolution of banks at supranational level.

While euro-area members have been included in all elements of the banking union by default, the SSM also allows non-euro area EU members to participate. For these countries, an important strategic question is if and when they should join part or all of banking union. On this question, opinions differ (Figure 1). Sweden declared in 2014 that it will not join banking union in the foreseeable future, and has not since changed its view substantially4, remaining the United Kingdom's main ally on this issue. By contrast, Denmark's government said in April 2015 that it wants to become part of the banking union, because it views it as being in the interests of its financial sector (Østergaard and Larsen, 2015)5. In central and eastern Europe, the Czech Republic remains sceptical about eventual participation in the banking union, and Hungary and Poland have also adopted wait-and-see approaches6. Bulgaria and Romania are more positive about joining banking union. In July 2014, Bulgaria said it would seek to join banking union after poor supervision led to the collapse of its fourth biggest lender7. Romania too has embraced the idea of joining banking union from early on (Isarescu, 2013).

These wait-and-see positions are often motivated by the consideration that joining banking union might imply joining the euro. However, we argue that in the long-term, banking union’s ultimate rationale is more linked to cross-border banking in the single market, which goes beyond the single currency. Therefore, the debate about whether to opt in to banking union is not necessarily a debate about joining the full package, eg joining both the euro and banking union.

A system of national supervision and resolution, when confronted with cross-border banking, can result in coordination failures between national authorities, because they do not take into account the cross-border externalities of their supervisory actions (see the Annex for a full overview of the theory of policy coordination). To address these coordination failures, supranational policies are needed (Schoenmaker, 2013). The coordination failure argument is related to the EU single market, which allows unfettered cross-border banking, and thus to the European Union as a whole. Furthermore, banking union encourages further cross-border bank integration, deepening the single market (Asmussen, 2013; Mersch, 2013). It follows that the ultimate rationale for banking union is cross-border banking (Constâncio, 2012; Schoenmaker, 2013). Banking union could therefore be an advantage also for countries outside the euro, which are characterised by a high degree of cross-border banking.

In this Policy Contribution, we document the high level of integration of the banking sectors of the nine banking union ‘outs’ and 19 ‘ins’. We argue that the outs could profit from joining banking union because it would provide a stable arrangement for managing financial stability. Banking union allows for an integrated approach towards supervision (avoiding ring fencing of activities and therefore a higher cost of funding) and resolution (avoiding coordination failure). On the other hand, countries can preserve sovereignty over their banking systems outside the banking union.

2. The European banking landscape

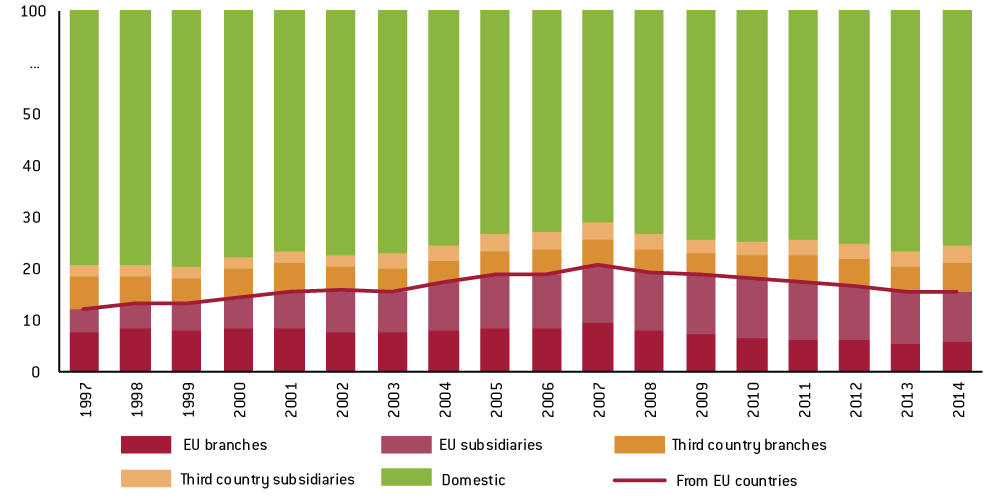

The single market enables banks to establish branches in other European Union countries based on home-country control. Host countries have only some limited powers related to liquidity supervision over cross-border branches. Figure 2 shows the percentage of total banking system assets from branches or subsidiaries of banks headquartered in other European Union or third countries, and thus illustrates the extent of cross-border banking penetration in European banking.

On this measure, cross-border banking within the European Union rapidly increased from 10 percent in 1997 to 20 percent in the run up to the global financial crisis. Interestingly, Figure 2 also shows that while branches were more present in 1997, the cross-border expansion in the 2000s was mostly done through subsidiaries. Cross-border penetration from EU countries started to decline in 2007. This trend continued through the start of the European sovereign debt crisis in 2010-11. The geographical breakdown of cross-border banking activity reflects a retrenchment on the back of the global financial crisis. Moreover, banks that received state aid were often pressured by national authorities to maintain domestic lending, cutting down on foreign lending. More recent data for 2014 suggests that the cross-border deleveraging process is bottoming out. Cross-border penetration from third countries was more stable at about 8 percent throughout the period, but also declined temporarily after 2007.

Figure 2: Cross-border penetration in European banking

Source: Bruegel based on ECB data. Note: Share of assets held by branches and subsidiaries headquartered in other EU countries and third countries over total banking assets in the European Union. The share is calculated for the aggregated EU-28 banking system.

2.1 The banking union area

The deeper rationale for the banking union is cross-border banking in the single market. We expect therefore that a genuine banking union market will develop when cross-border banking groups can transfer excess capital and liquidity across the group, and supervision is done at the consolidated level.

The international orientation of a country’s banking sector can be captured by dividing its cross-border banking activities into outward and inward banking claims. Outward banking refers to the exposure of a country’s multinational banking groups to other countries, beyond their domestic market, while inward banking is defined as the banking claims from abroad on the country in question.

In terms of outward banking, splitting the assets of the largest banks into the assets held in the home country, in the banking union countries, in the rest of Europe and in third countries, allows us to gauge the potential for coordina- tion failure between national authorities in crisis management.

Our basic source for the geographical split of assets is banks’ annual reports. When information on the geographical segmentation of assets is not available, we use the segmentation of credit exposures of the loan book, the most important asset class, as a proxy. Further information on credit exposure is available in the European Banking Authority’s published stress test results for 2014. The full methodology for measuring geographic segmentation is described in Schoenmaker (2013). Under the new Capital Requirements Directive (CRD IV), financial institutions must disclose, by country in which they operate through a subsidiary or a branch, information about turnover, number of employees and profit before tax. This extra information allows us to refine the geographical split at country level.

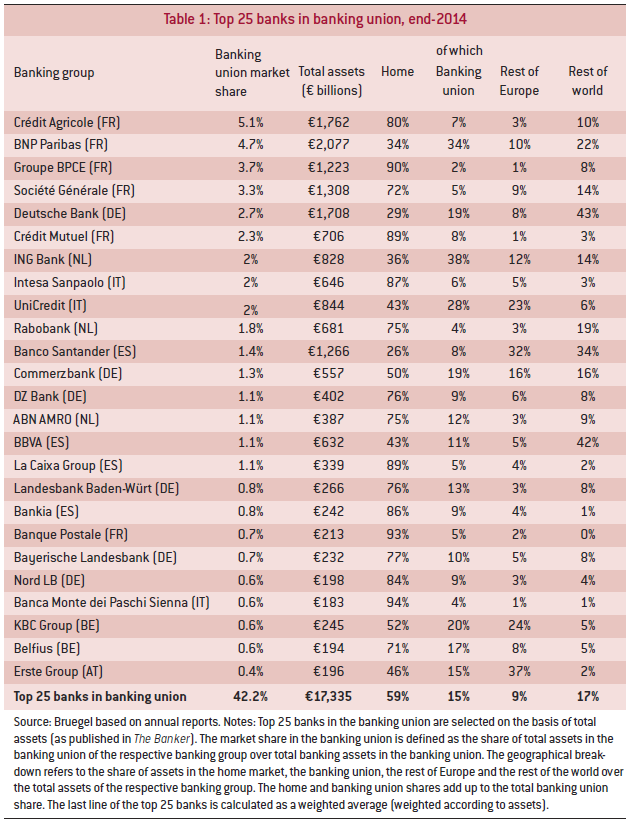

Table 1 shows the top 25 banks in the banking union by end-2014. In terms of assets, 74 percent of assets are held within the banking union area (the columns home and banking union combined), 17 percent in the rest of the world, and only 9 percent of assets are held in other European countries. While 59 percent of assets were held with the respective home countries before entry in the banking union, this ‘home’ percentage increased to 74 percent when the home base expanded to the banking union area. Only a few banking union area banks have substantial activities in other EU countries. Examples are UniCredit with 23 percent, KBC Group with 24 percent and Erste Group with 37 percent (all three mainly in central and eastern Europe) and Banco Santander with 32 percent (mainly in the United Kingdom).

2.2 Outward banking

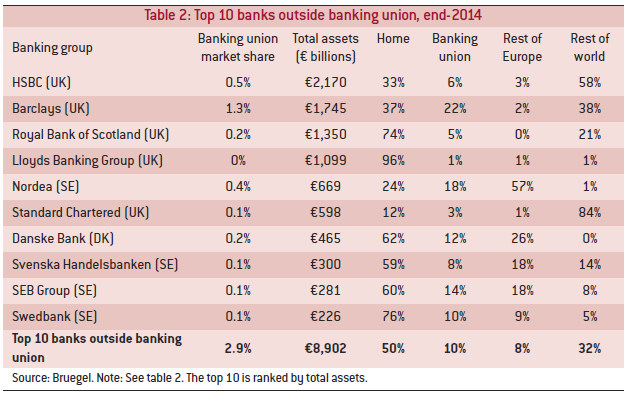

Table 2 shows the geographical segmentation of the top 10 banks outside the banking union. Overall, these banks hold 50 percent of their assets in their home country, 10 percent in the banking union market, 8 percent in other European countries and 32 percent in the rest of the world. On a bank level, Barclays (UK) holds 22 percent of its assets in the banking union, mainly in Italy (5.1 percent), Spain (3.7 percent), Germany (3.4 percent) and France (2.9 percent)8. Nordea (Sweden), SEB Group (Sweden) and Danske Bank (Denmark) have assets amounting to 18 percent, 14 percent and 12 percent respectively in the banking union (in particular Finland and the Baltics)9. These three banks are pan-Nordic banks.

This indicates that the countries outside banking union (especially the Scandinavians) are characterised by a large share of outward banking claims on banking union as well as other European countries. If all of the ‘outs’ were to join banking union, the potential increase in assets brought under consolidated supervision would be the 10 percent of assets held in the banking union and the 8 percent of assets held in other European countries that are not yet part of the banking union.

In countries characterised by an extensive share of outward banking, the resolution of these multinational banks poses an important challenge. Mervyn King’s famous quote that “banks are international in life, but national in death” captures best what is at stake (quoted in Turner, 2009). In the case of multinational banks, if supervision and resolution are national, the home-country authorities only take the domestic share of a bank’s business into account when considering a bank rescue, without paying much attention to the cross-border externalities of their actions (Schoenmaker, 2011; Zettelmeyer, Berglöf and De Haas, 2012). In this context, the eventual burden sharing will be contentious between the home and the host country, inducing outcomes that are both inefficient and detrimental for systemic stability (Goodhart and Schoenmaker, 2009). While the SRM is a complicated coordination mechanism involving the European Commission and the national finance ministers in addition to the Single Resolution Board, the SRM Regulation mandates a banking-union wide perspective for the resolution of banking-union banks (Schoenmaker, 2015). This banking-union wide mandate should prevent the splitting of banks along national lines in the resolution process. Article 6(1) of the SRM Regulation forbids discrimination against entities on national grounds.

2.3 Inward banking

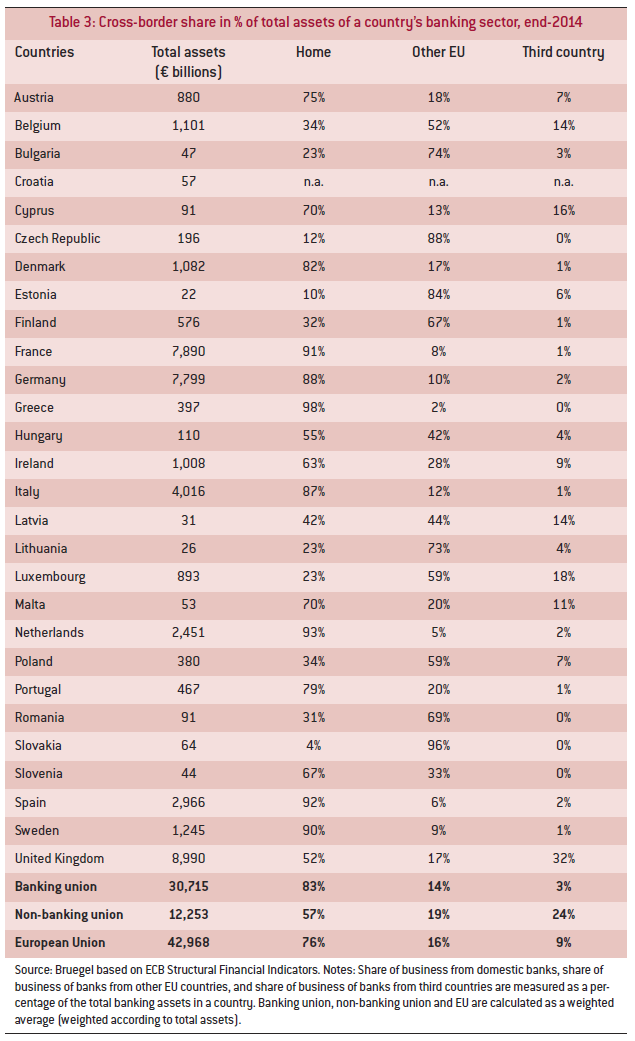

Moving from outward to inward banking, Table 3 shows foreign-owned assets in EU countries as a percentage of the total assets of that country’s banking sector, domestic and foreign-owned. It emerges that the extent of inward claims coming from the European Union is actually higher in the banking-union outs (19 percent) than in the ins (14 percent).

In the non-banking union countries, the cross-border share in total assets of a country’s banking sector is particularly high in some central and eastern European countries, where the share is between 45 and 90 percent. By contrast, Sweden and Denmark report only moderate inward claims of around 10 and 18 percent, respectively. The United Kingdom is a special case. It is the only EU country with more claims from banks in the rest of the world (32 percent) than from banks headquartered in the rest of the EU (17 percent). Major US and Swiss (investment) banks form a substantial part of the share coming from the rest of the world. These banks use their London offices as a springboard to conduct business across the EU. This reflects the importance of London as an international financial centre.

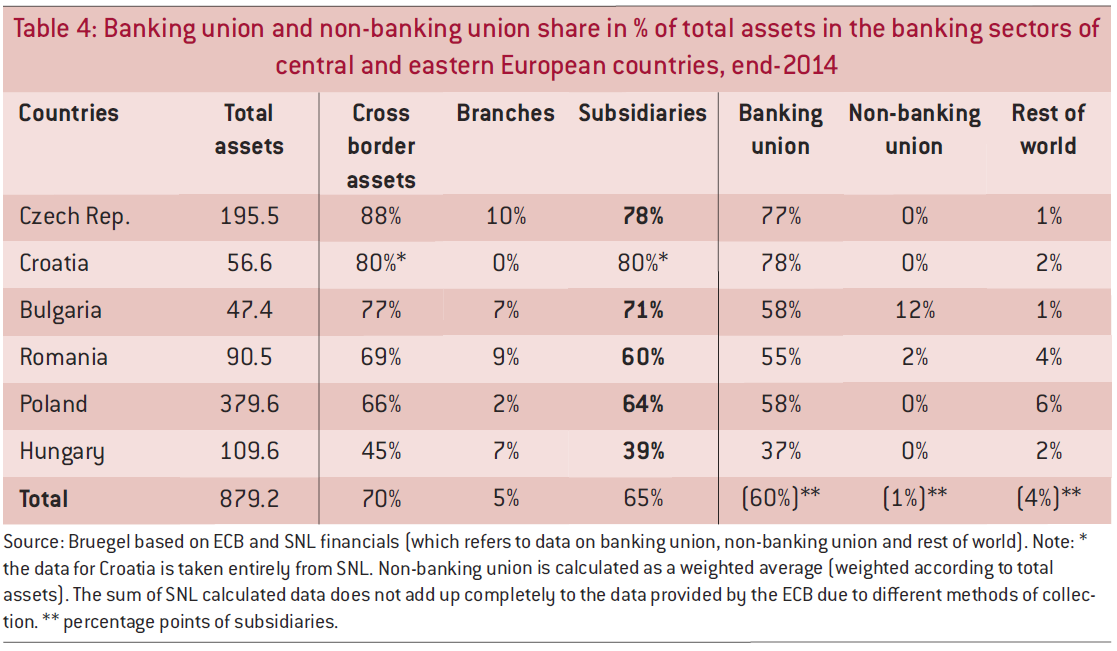

Looking more closely at the outs of central and eastern Europe (in our case Bulgaria, Croatia, Czech Republic, Hungary, Poland and Romania), Table 4 shows a further breakdown of their banking assets owned by banks of other countries according to the location of their headquarters: in the banking union, the non-banking union area or the rest of the world. On aggregate, the banking sector in these central and eastern European countries is characterised by 70 percent cross-border claims, with 65 percent operating as subsidiaries and only 5 percent as branches. The subsidiaries can be broken down further into whether their parents are located in the banking union area or outside. Of the subsidiaries, the great majority (60 percentage points) have their parent bank located in the banking union area, compared to 1 percentage point coming from the non-banking union area and 4 percentage points from the rest of the world.

A look at the country level confirms the significance for these countries of claims from the banking union area: with 77 percent and 78 percent respectively, the Czech Republic and Croatia report by far the greatest share of foreign-owned subsidiaries from the banking union area, followed by Bulgaria, Romania, and Poland with shares of 55 to 58 percent. Hungary has slightly lower claims, with 37 percent coming from the banking union area. On aggregate, more than half of the banking assets of all outs from central and eastern Europe, except Hungary, are held by subsidiaries of banks headquartered in the banking-union area.

During the financial crisis, supervisors tightened restrictions on intra-group cross-border transfers, limiting the ability of multinational banking groups to re-allocate capital and liquid assets from subsidiaries with an excess to those in need of capital and/or liquidity. Hence, stand-alone subsidiaries tend to have higher capital and liquidity, which translates into a higher cost of capital for the host country (IMF, 2015).

Moreover, though the Vienna Initiative was successful in coordinating policy during the recent financial crisis (see the Annex), banking union membership could replace such ad-hoc arrangements. First, this would allow consolidated supervision, as opposed to sub-entity stand-alone supervision. Darvas and Wolff (2013) note that in the central and eastern European countries, national authorities had a hard time addressing credit booms through national supervisory action, because banks indulged in supervisory arbitrage. Similarly, national authorities had difficulties in preventing massive withdrawals by western European banks; coordination through the Vienna Initiative was in the end decisive to maintain the lending capacity in the region. In the case of banking-union membership, these issues could be more easily addressed. Second, membership would give more regulatory certainty in times of crisis, because it can be seen as a permanent ‘lock-in’ coordination tool for all the participating countries, avoiding ad-hoc measures.

3. Conclusions

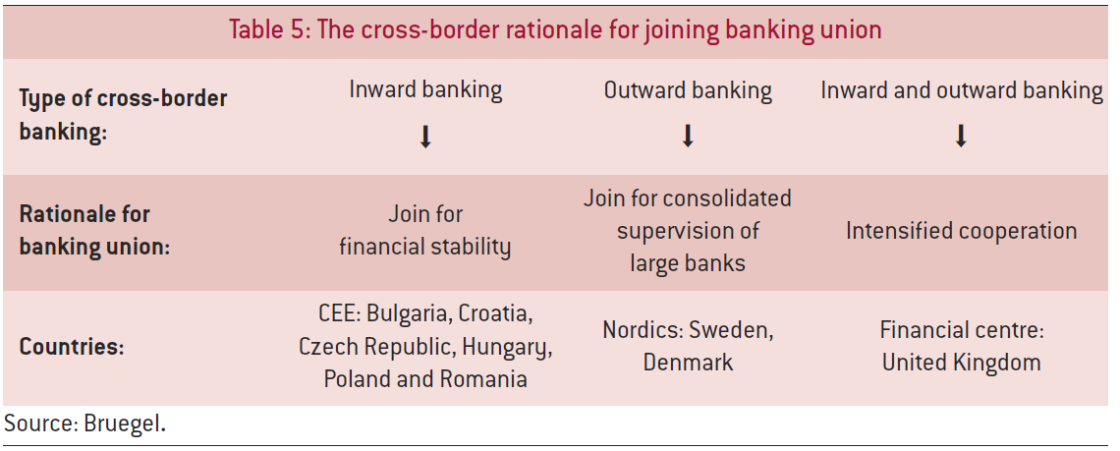

In summary, Denmark and Sweden are characterised by extensive outward banking towards the banking-union area, while inward banking from the banking union is particularly important for the six outs in central and eastern Europe. Taken together, this indicates that the outs might benefit from banking union membership (see Table 5). That leaves the United Kingdom, which as an international financial centre has more outward banking towards the rest of the world than the banking union. Nevertheless, banking union is also important for London’s position as gateway to Europe for international banks. Moreover, London is host to the wholesale operations of the major European banks.

The outs, in particular Denmark and Sweden and those in central and eastern Europe, could join the SSM and the SRM on a bilateral basis, which would be advantageous given their large shares of outward and inward banking. The SSM and SRM Regulations explicitly allow for this opting in. The outs, except for Sweden and the United Kingdom, have already signed up to the intergovernmental agreement on the Single Resolution Fund. For Denmark and Sweden, joining banking union would increase the effectiveness and efficiency of the supervision and resolution of the larger European cross-border banks allowing supervision and resolution at the consolidated level. For the outs in central and eastern Europe, the banking union would be a more stable arrangement for managing financial stability and maintaining lending capacity than the ad-hoc Vienna Initiative. Finally, for the United Kingdom, joining banking union would also be beneficial, but there is strong political opposition. Given the strong banking linkages with the banking union, intensive cooperation between the Bank of England and the ECB is necessary for the effective management of financial stability.

Therefore, the benefit of the outs joining banking union would be enhanced supervision and resolution. By joining, the outs would also gain seats at the table at the Supervisory Board of the ECB and at the Single Resolution Board, as well as some safeguards for non-euro area opt-ins, such as the reasoned disagreement procedure and the exit clause10. However, an opting-in country has more limited influence in the decision-making process within the SSM compared to a euro-area country, because the former has no seat in the Governing Council of the ECB. The Governing Council is the highest decision-making body within the SSM. Also, liquidity provision by the ECB is not automatic (IMF, 2015).

There would still be misalignments between supervision and burden sharing. Nevertheless, joining the ESM for indirect and direct bank recapitalisation should also be made feasible on a bilateral basis. During the Irish banking rescue in 2010, the western European outs, the United Kingdom, Denmark and Sweden, joined the rescue package by providing bilateral loans, following the ECB capital key, because some British banks were exposed to Ireland and thus benefited from enhanced financial stability in Ireland (Gros and Schoenmaker, 2014)11. This is a good illustration that burden sharing between the euro-area coun

tries can be widened if and when needed.

Finally, the current wait-and-see approach is a response to the short track record of banking union so far. The SSM has had one year of operation, while the Single Resolution Board started its mandate in January 2016, and has not yet handled a resolution case. The experiences of the ins with the Single Supervisory Mechanism and the Single Resolution Mechanism, for better or worse, will shape the willingness of the outs to join.

References

Please see the PDF version of this publication for the full references.

Annex: The theory of policy coordination

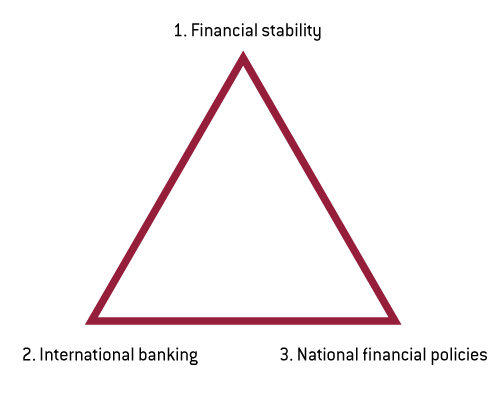

Financial stability is a public good. A key issue is whether governments can still produce this public good at the national level with today’s globally operating banks. The financial trilemma states that (1) financial stability, (2) international banks and (3) national financial policies are incompatible (Schoenmaker, 2011). Any two of the three objectives can be combined but not all three; one has to give. Figure 3 illustrates the financial trilemma. The financial stability implications of cross-border banking are that international cooperation in banking bailouts is needed.

Figure 3: The financial trilemma

Source: Schoenmaker (2011).

Financial stability is closely related to systemic risk, which is the risk that an event will trigger a loss of economic value or confidence in a substantial portion of the financial system that is serious enough to have significant adverse effects on the real economy. Acharya (2009) defines a financial crisis as systemic if many banks fail together, or if one bank’s failure propagates as a contagion, causing the failure of many banks. Such a linked failure of banks arises from the correlation of their asset returns and the externality is a reduction in aggregate lending and investment.

The 2007-09 financial crisis illustrated the financial trilemma, with the handling of Lehman Brothers and Fortis as examples of coordination failures (Claessens, Herring and Schoenmaker, 2010). During the attempt to rescue Fortis, cooperation between the Belgian and Dutch authorities broke down despite a long-standing relationship in ongoing supervision. Fortis was split along national lines and was subsequently resolved by the respective national authorities at a higher overall fiscal cost.

Rodrik (2000) provides a lucid overview of the general working of the trilemma in an international environment. As international economic integration progresses, national policies must be exercised over a much narrower domain, and global federalism will increase (eg in the area of trade policy). The alternative is to keep the nation state fully alive at the expense of further integration. The domestic orientation of the financial safety net is a barrier to cross-border banking, because national authorities have limited incentives to bail out an international bank. This is visible in the results of Bertay, Dermirguc-Kunt and Huizinga (2011), who find that an international bank’s cost of funds raised through a foreign subsidiary is higher than the cost of funds for a purely domestic bank.

How can the financial trilemma be solved? The literature on international policy coordination proposes two main solutions. The first is to develop supranational solutions (Obstfeld, 2009). In this case, national financial policies will be replaced by an international approach for supervision and resolution. Participating countries have to share the burden in case of a bank bailout, resulting in a loss of sovereignty, which is politically controversial (Pauly, 2009). The EU banking union members have chosen this approach. The second is to segment national markets through restrictions on cross-border flows, through prudential tool such as ring fencing (Eichengreen, 1999)12. In the case of international banks, the segmentation can be done through national regulations, which favour a network of fully self-sufficient, stand-alone national subsidiaries, as opposed to a network of branches (Cerutti et al, 2010). The banking union outs have adopted the latter approach, safeguarding national sovereignty.

During the crisis, national ring fencing activities happened across the euro area (and beyond), for example in Germany, where the regulator BaFin banned Italy’s UniCredit from transferring excess capital in the form of dividends from its German subsidiary back to its Milan headquarters. BaFin feared that the transfer could leave German depositors exposed to supporting UniCredit13. Arguably, with the establishment of the banking union, ring fencing – as a crisis response – should occur less, because the ECB is the supervisor of both the parents (including the branches) and the subsidiaries in the participating member states, and the Single Resolution Board (SRB) is the resolution authority for the banking group. The ECB and SRB have a banking union-wide mandate and thus take into account all of a bank’s activities within the banking union. This reduces the need for ring fencing in the case of the resolution of a cross-border banking group.

However, coordination failures can still occur when the parent bank or one of its subsidiaries operates outside the banking union.

National interests

Herring (2007) states that cross-border coordination fails when national interests do not overlap, which might arise because of one of three different asymmetries. First, there could be supervisory asymmetries, with the supervisory authorities differing in terms of staff skills and financial resources. Second, there might be an asymmetry in accounting, legal and institutional infrastructure. Third, different national resolution regimes might prompt non-coordinated behaviour in the case of cross-border bank resolution. The key issue in overcoming these asymmetries in national interests is whether the banks are systemically important in either or both countries (see Table 6).

Only when a major bank’s activities are systemic in the home and host countries, is there potential for coordination (see case a), which is, for example, the case for the Vienna Initiative. The Vienna Initiative in 2009 was successful in coordinating international stakeholders operating in central and eastern Europe in order to avoid massive capital retrenchment at the height of the financial crisis14. De Haas et al (2012) show that even though foreign and domestic banks all curtailed credit during the crisis, banks that signed the Vienna Initiative were more stable lenders to the region than banks that did not participate. Here, the banking problems in both the home and host countries were systemic and the relevant authorities thus had a common interest in addressing the banking problems. Nevertheless, coordination is not always achieved in case a. For example, there was a coordination failure in the case of Fortis, cited above (Schoenmaker, 2013).

In the intermediate cases (cases b and c in Table 6), the potential coordination failure is linked to the extent of inward or outward banking. Inward banking is defined as the banking claims from abroad on the country in question, while outward banking captures the exposure of multinational banking groups to other countries, beyond the domestic market.

Implications for banking union

Focusing on the EU banking union outs, from a host-country perspective, a high level of inward banking indicates a high share of systemically important banks in the host country, which might or might not be systemic for the home country (cases a and b). This limits the capacity of the host authority to manage the stability of its financial system, including the lending capacity to its economy. From a home-country perspective, a high level of outward banking indicates major international banking groups, which are systemic for the home country, and might be systemic or non-systemic for the host countries (cases a and c). This poses challenges for the home authority to manage the stability of its international banks and thereby its financial system, especially in the case of cross-border resolution.

About the authors

Related content

A brown or a green European Central Bank?

The European Central Bank portfolio is skewed towards the brown economy, reflecting a bias in the market.

The European Central Bank’s timid operational framework update

The European Central Bank announced limited changes to its operational framework – which is probably right given current uncertainty

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

A new integrated-value assessment method for corporate investment

To contribute more to the green transition, companies should start to make investment decisions based on integrated-value assessment.