Decentralised finance: good technology, bad finance

Given the importance of digitalisation, it is fair to ask whether these digital decentralised services will become established and normalised.

Executive summary

- The emergence of cryptocurrencies/crypto assets has allowed the provision of a new form of financial services, including payments and loans, known as decentralised finance (DeFi). Crypto assets currently represent only about 1 percent of total global financial assets and it is unlikely, in its current form, that DeFi will become a substitute for the traditional financial system, for three reasons.

- First, while decentralisation is very innovative, in practice the technology required to replace the role of intermediary is slow and costly in terms of energy use. This has led some crypto networks to adopt more centralised solutions to the problem of verification.

- Second, the automaticity behind the transactions does not allow for any legal recourse. If something goes wrong, there is no way to stop or reverse a transaction once it has been initiated. It is very difficult to imagine DeFi scaling up without the ability to challenge outcomes.

- Third, and perhaps most importantly, DeFi is for the most part self-referential. Crypto assets are exchanged for other crypto assets without being employed in activities that stimulate economic growth by creating jobs or facilitating investment. It is not likely for DeFi to grow enough to replace traditional finance unless it helps growth.

- Nevertheless, the technology that enables DeFi and crypto assets, distributed ledger technology (DLT), is very innovative and has managed to remove the intermediary without compromising the safety and finality of financial transactions. Hence, it is likely that the technology behind crypto assets and DeFi will feed into the mainstream and offer efficiency gains.

1. Introduction

The main objectives of the traditional financial system in its entirety (banks, other financial institutions and investors) are to support efficient capital allocation decisions and to finance productive activity: activity, in the sense that it finances growth through job creation and investment; productive, in the sense that the activity financed is profitable and therefore sustainable.

The emergence of cryptocurrencies has introduced an important innovation into the financial system, which, traditionally, has acted as an intermediary connecting investors, seeking returns on their savings, and borrowers, who seek funding for their projects. Cryptocurrencies enable the removal of intermediaries without compromising the safety and finality of financial transactions. This marks a revolution in how transactions are settled between any two parties. As cryptocurrencies have become more popular and established, crypto financial services, like lending, have also emerged. Given the increasing importance of digitalisation, it is fair to ask whether these digital decentralised services will become established and normalised. Answering that question requires an examination of whether and how the crypto world contributes to the main objectives of the financial system: reducing search costs and financing growth.

This paper explores this question. We identify the economic value of crypto assets as they form the backbone of all decentralised finance (DeFi) activities. We then describe DeFi activities and discuss how they differ from traditional finance. We also describe the opportunities and risks DeFi creates, with reference to distress episodes seen in 2022. As DeFi expands and takes more space in the financial system, regulators will want to ensure that it is subject to the same rules that govern the financial system.

While there is certainly space for DeFi to function and evolve, given that there is demand for it, it will not replace the traditional financial system for three reasons. At best it will be a small component of the whole system, and by the time regulation catches up, it will also not be all that different.

First, the elimination of intermediaries is not sustainable. The innovative technology used, known as distributed ledger technology (DLT), primarily blockchain, is an algorithmic way of verifying and settling transactions between two parties. In other words, it is a way of removing the intermediary from any transaction. No single agent acquires and maintains monopoly power through intermediation, or enjoys exorbitant rents. In this respect, DLT reduces costs and improves efficiency in transactions.

But the intermediary in traditional financial systems also plays an important role in reducing transaction costs and asymmetries for the parties that transact 1 Grassi et al (2022) summarised the finance literature on the very well-established role of intermediaries. . Through technology, DLT can solve some of the problems of information asymmetries and search costs, but it also introduces new transaction costs in the form of a very high processing time of transactions (compared to near instantaneous card transactions, for example) and very high energy consumption. The industry is aware of these costs and is looking for solutions. But these solutions all converge on creation of trusted centralised nodes that verify and settle transactions quickly and with little energy use. In other words, there is a reversion to a more centralised structure, thus negating the very innovation promised by DLT.

Second, DeFi does not allow for legal recourse and therefore lacks formal accountability. Following the previous point, the direction of travel is towards creation of ‘trusted’ nodes to carry out verification processes. But trust is not built without good governance structures. While the algorithms used are transparent and automatic, they do not hold any party to account as the protocols 2 A protocol consists of code that determines a set of rules that define how users can share data. used have no recourse to the legal system. To which legal jurisdiction would these transactions be subject, given that they occur across borders? Which party could be held accountable when the system is anonymised and private? These are difficult problems to solve. Establishing accountable parties, such as decentralised autonomous organisations (DAOs), could be part of the solution. But notions of trust, customer knowledge and the safety net of the possibility of legal recourse are crucial for financial transactions to function smoothly. It is thus difficult to imagine how, without such trust mechanisms, DLT can scale and match the size of the traditional financial system.

Third and perhaps most important, the vast majority of activities that happen in the context of DeFi are self-referential in that one crypto asset is exchanged for another, but is not used to finance productive activity (BIS, 2022) 3 See also US Treasury (2022), which offers evidence on the use of stablecoins to facilitate transactions within the crypto ecosystem. . The only time when crypto assets contribute to the creation of value-added is when they are exchanged for public currencies and are put back into the traditional financial system. Similarly, when crypto assets lose their value, they represent a loss to the real economy equal to the fiat currency value that was used to purchase them. This is an important reason to doubt that DeFi, in its current form, will become a significant and sustained part of the whole financial system.

This does not mean that DeFi does not offer opportunities that can be of value added in the system. DeFi offers the chance to understand how financial services could benefit from efficiency gains and, therefore, how to incorporate DeFi services into the mainstream, while protecting their legitimacy and stability within a regulated system.

2. A brief introduction to crypto and its economic relevance

Crypto relies on an innovative technology called distributed ledger technology (DLT) to store information in a secure way using cryptography. DLT is a digital infrastructure that records transactions. Any transaction is accessed, validated and recorded by those participating in the ledger. This is innovative in that the anonymity of those who transact is maintained and because there is no need to audit transactions, because many parties verify and store them. This is how the middleman is made redundant 4 See also Makarov and Schoar (2022): DLT is “an alternative architecture of storing and managing information where no single entity has full control over all the states and transactions, or any subset of them. Instead, multiple parties (validators) hold their own copies of states and jointly decide which transactions are admissible”. .

Blockchain is a form of DLT in which all transactions are recorded and organised in digital blocks that are linked together. Simply put, blockchain can be seen as a database of transactions, made up of a chain of information blocks, which is spread across various computers (‘nodes’). Not relying on a single server system makes the network more resilient to hacks or shutdowns. Additionally, blockchain is in principle immutable, meaning that once the information on a transaction is validated and stored in a block, it cannot be changed or deleted.

Blockchain networks can be implemented in different ways in terms of who can validate the transactions and who can observe the records. In permissionless blockchains, anyone can validate transactions, while in permissioned blockchains, only a pre-approved group of validators can validate transactions. In the latter case, the group is approved by a coordinating body. Additionally, ledgers can be made private or public. When ledgers are public, everyone can access fully the information stored on the blockchain. When the blockchain is private, only authorised parties can access it. Permissionless blockchains tend to be public, whereas permissioned blockchains are typically private. Validators are compensated in the form of transaction fees – paid in cryptocurrency – when the task is performed.

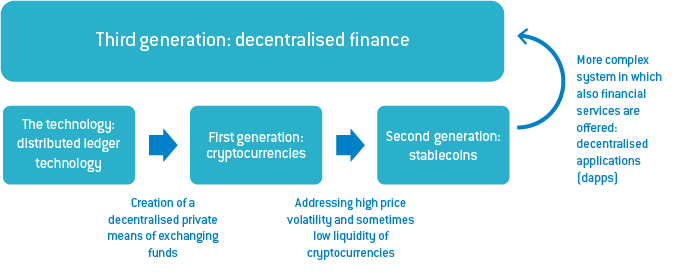

Figure 1: Crypto evolution

Source: Bruegel.

The technology was used to create the first – and still most widely known – cryptocurrency, the Bitcoin, in 2008. Since then, crypto has evolved into a much more complex environment, with a variety of assets and services offered (Figure 1). The first generation of cryptocurrencies was very volatile, a bug that the second generation, called stablecoins (see below), aimed to correct. The availability of both types allowed, in the third wave of crypto evolution, the provision of financial services, now called decentralised finance.

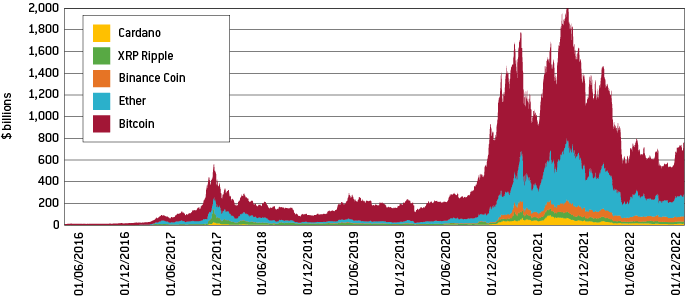

A central feature of cryptocurrencies, and therefore of the financial services provided, is that the identity of those participating in transactions is hidden behind the respective cryptographic digital signature. This element, along with the fact that no central authority governs it, differentiated cryptocurrencies from traditional ways of sending money and started attracting enthusiasts. Other cryptocurrencies have emerged, but Bitcoin remains the most widely used, followed by Ether (Figure 2).

Figure 2: Top 5 cryptocurrencies by market capitalisation ($ billions)

Source: Bruegel based on CoinGecko. Note: Data from 1 June 2016 to 20 February 2023.

Despite being denominated ‘cryptocurrencies’, many prefer the term crypto assets, since so-called cryptocurrencies do not fulfil simultaneously the three main attributes of money: being a measure of value, a store of value and a medium of exchange (Claeys et al, 2018). The price volatility of cryptocurrencies, reflecting supply and demand forces rather than underlying economic fundamentals, undermines value predictability, making crypto unattractive as a store of value.

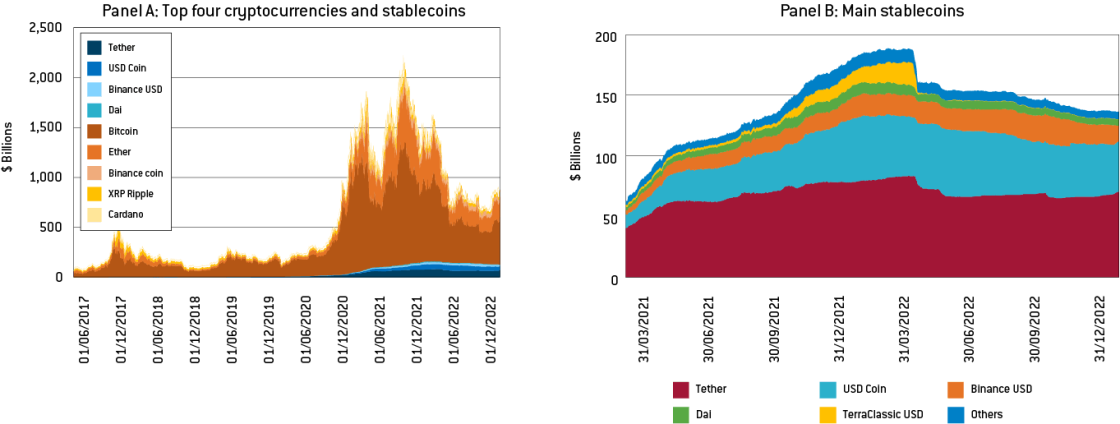

To overcome the high price volatility and sometimes low liquidity of cryptocurrencies, stablecoins started to emerge as a more reliable alternative. There are two main types of stablecoins: asset-backed and algorithmic (BIS, 2022). Asset-backed stablecoins are pegged to an asset, which can be, for instance, a fiat currency – usually the US dollar – or gold, government bonds or cryptocurrencies. To maintain the peg, a centralised intermediary should manage and ensure a sufficient level of the underlying reserves. This entity also coordinates redemptions and creation of the stablecoin. The first to be created was Tether, launched in 2014. It is pegged to the US dollar and keeps public records on the level of reserves maintained to keep the peg. Algorithmic stablecoins rely on algorithms to balance supply automatically, to maintain the relative value to the chosen anchor. However, they do not provide a credible peg as they do not have traditional reserves (such as sovereign currencies or other assets).

Although still representing a small fraction of total crypto assets, stablecoins have increased in importance steadily, accounting for about 21 percent of the total by November 2022 5 According to the market dominance measure of coinmarketcap.com on 22 November 2022. . Despite the large number of stablecoins already in the market, there are clearly two big players, which together account for almost 82 percent of stablecoins by market capitalisation (Figure 3), and they are almost exclusively dollar-backed (around 94 percent of stablecoins’ market capitalisation). The provision of DeFi services was enabled by the existence of stablecoins, but was also a key driver of the increased popularity of stablecoins. Interest in stablecoins also stems from their hedging properties against the volatility of crypto assets (Kakinuma, 2023).

Figure 3: The cryptocurrencies and stablecoins market

Source panel A: Bruegel based on CoinGecko. Notes: Orange refers to cryptocurrencies, blue to stablecoins. Data from 1 June 2016 to 20 February 2023. Source panel B: Bruegel based on DeFi Llama. Data from 31 March 2021 to 20 February 2023.

A new generation of crypto innovation started after the launch of the Ethereum network in 2015. Ethereum is a decentralised permissionless blockchain that runs on the native cryptocurrency Ether. Importantly, the Ethereum blockchain (unlike other popular platforms such as Bitcoin) allows users to build decentralised applications (dapps) on its network, making it highly interoperable and, hence, the ideal space for decentralised finance (DeFi) to develop. So, while relying on the same underlying technology and still using cryptocurrencies as the means of entry and participation, DeFi represents an expansion of the initial concept to a more complex system in which financial services have started to be developed and offered.

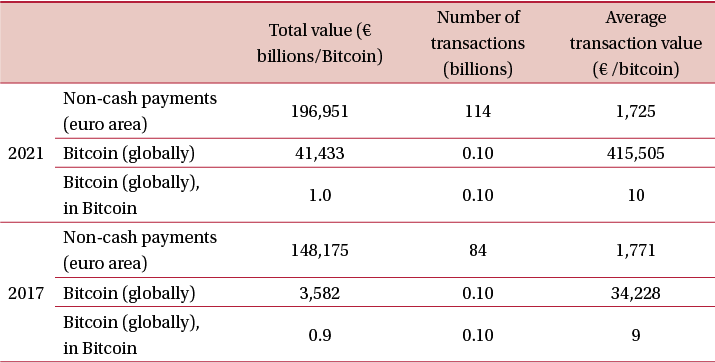

Despite its increasing relevance, the crypto market still represents a small fraction of the total financial system. According to the European Central Bank, the value of all crypto assets represents less than 1 percent of total global financial assets (Panetta, 2022). Crypto also represents only a small component of the total value of payments. Table 1 shows this for the euro area. Importantly, the increase in the total value of Bitcoin transactions from 2017 to 2021 was primarily driven by an increase in the value of Bitcoin against the euro, not by an increase in the volume of transactions. This can be seen by comparing for each year the second and third rows in Table 1, in which we report the total value of Bitcoin transactions in euros and in Bitcoin, respectively. In fact, Bitcoin total transactions increased only from 900 million to 1 billion Bitcoins, while the conversion to euros shows a more dramatic increase.

Table 1: The popularity of euro vs bitcoin

Source: Bruegel based on ECB SDW and Tradeblock.com.

3 What does DeFi involve and why is it innovative?

Peer-to-peer transactions done via DLT are different to transactions in the traditional financial system in that they are decentralised and non-custodial. In other words, peer-to-peer transactions sidestep intermediaries – decentralisation – and function in a non-custodial manner, with users having full control over the private key that unlocks their assets, with no need to go through third parties.

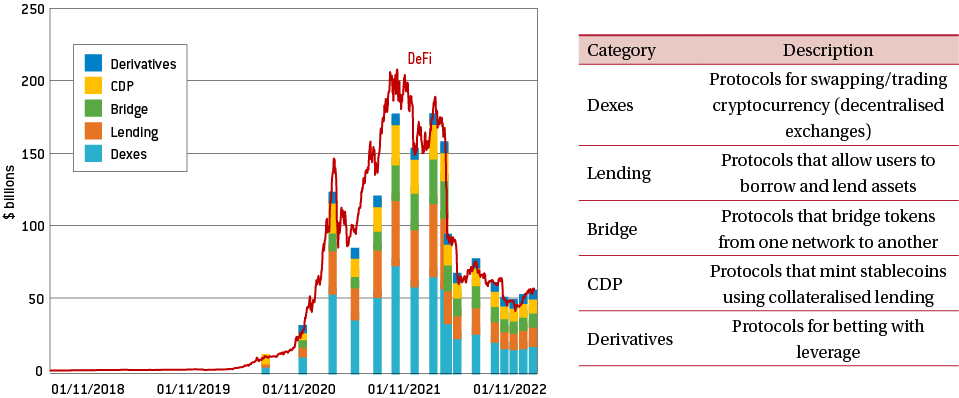

DeFi, like the traditional financial system, offers a variety of services. Figure 4 shows different service types and their current valuations. These services range from platforms for exchanging crypto assets (Dexes) and protocols for lending and borrowing (Lending), to protocols for linking networks of crypto assets (Bridges) and protocols to mint stablecoins from collateralised lending (Collateralised Debt Position, CDP). Exchanges were originally the most popular service, but lending and borrowing are increasing in significance.

Unlike the traditional system, the only criteria for being able to participate in DeFi is to own crypto assets. In traditional finance, by contrast, say in the case of granting a loan, an assessment needs to be made by the issuing authority that may ex post exclude participation for some. It is for this reason that DeFi supporters claim that its services provide equal access rights.

Figure 4: Decentralised finance, total value locked ($ billions)

Source: Bruegel based on DeFi Llama. Notes: Total value locked refers to reserves locked in smart contracts embedded in the various services, not to transaction volume or market capitalisation. In the chart, DeFi total value locked-in includes borrowed coins in lending protocols. Selected services represent the top five in terms of total value locked. Data from 1 November 2018 to 20 February 2023.

The backbone of this new decentralised system consists of smart contracts, which are self-executing deterministic contracts stored on a blockchain. In other words, smart contracts are computer programs that automatically execute agreements between two parties, when certain clearly pre-defined conditions are met. Smart contracts thus reduce the room for interpretation or subjectivity. The automaticity of these contracts eliminates the need for an intermediary: if both parties agree to the conditions specified, then as soon as they are fulfilled, the contract will be triggered, and the transaction executed. Smart contracts can even act as custodians of crypto assets, which will only be released when and to whom the contract conditions stipulate.

As smart contracts are done via DLT, they are encrypted and therefore very secure. Furthermore, transparency, clarity and predictability make them quick and efficient. These factors combined generate sufficient trust for demand to be generated, and have underpinned the proliferation of a multitude of financial applications, including trading, lending and asset management, in an ecosystem devoid of traditional intermediaries such as brokerages, centralised exchanges and banks.

Crypto lending is a major part of the DeFi ecosystem. Decentralised loans are an interesting DeFi application because they ignore the basic elements that enable lending in traditional finance, such as trust relationships and detailed information on the borrower. Loans in the DeFi environment are divided into two types: collateralised loans, and non-collateralised lending known as flash loans.

For collateralised loans, the collateral needed is held in a smart contract for the duration of the loan, and is only released back to the borrower as soon as the loan is fully repaid. Typically, the collateral requested amounts to between 120 percent and 150 percent of the loan value granted, in the form of crypto assets (Aramonte et al, 2022). In other words, in order to borrow one Bitcoin, the borrower must pledge between 1.2 and 1.5 Bitcoins as collateral. There are two reasons why so much collateral is required. First, and in contrast to traditional bank lending, the lender has no information on the creditworthiness of the borrower (eg through credit scores). Second, a dearth of regulation, problems of illiquidity and propensity for margin calls induced by crypto volatility collectively cloud the DeFi space with systemic risk.

Flash loans, meanwhile, are uncollateralised. These loans, as the name suggests, are instantaneous transactions. A borrower demands a loan to use in an activity that generates profit. If the profit generated is sufficient to pay the loan fees, the loan is granted and paid back instantaneously. If however the activity for which the borrower uses the funds fails to earn a profit, the loan is cancelled. This all happens in the same instant with one execution order in the smart contract.

The structure of flash loans thus dovetails well with yield mining, in which investors attempt to take advantage of minor discrepancies across markets. However, because users can borrow any desired amount of capital without putting up collateral, flash loans have grown into a popular instrument for market manipulation and deception. In April 2022, for instance, Beanstalk Farms, a DeFi project, suffered a $182 million loss 6 Sidhartha Shukla, ‘DeFi Project Beanstalk Loses $182 Million in Flash Loan Attack’, Bloomberg, 18 April 2022, https://www.bloomberg.com/news/articles/2022-04-18/defi-project-beansta…. from attackers exploiting a lapse in its smart contract code.

In terms of market dynamics, after a period of meteoric growth, which saw DeFi go from a market (measured by total value locked; see Figure 4) of $11 billion in November 2020 to over $200 billion in November 2021, the market for decentralised finance has more recently grown more sluggishly. By the end of February 2023, the DeFi industry had a value of around $57 billion (Figure 4). A key reason for this market volatility is that DeFi applications deal in cryptocurrency and are therefore affected by their volatility trends.

4. DeFi: an opportunity masked with risks

By aiming to be decentralised, DeFi brings significant innovation to the financial world. The elimination of the middleman in a way that does not jeopardise the safety and finality of transactions is perhaps the most important innovation it brings. The fact that the Bitcoin protocol, the very first cryptocurrency created, continues to be traded shows that there is both demand for and sufficient trust in the value that crypto assets create.

The DeFi ecosystem is also conducive to the development of innovation: code is open-source and protocols are interoperable, enabling developers to easily build off existing software. This design structure fosters continuous development of programs and greater competition among industry players. Smart contracts are one of the most game-changing features of DeFi. Their transparent, deterministic and self-executing nature can help bypass the transaction fees, permission structures and delays associated with traditional intermediaries.

Nevertheless, there are limitations to these innovations.

4.1 How smart are smart contracts?

The characteristics of smart contracts make them automatic in nature and therefore much less prone to manipulation. However, a great deal of due diligence is required upfront, since once executed there is no way to reverse out of a contract. Consequently, smart contracts should be written should and be as complete as possible. For instance, if there is no provision in case of a mutual mistake, there will be no way of cancelling the smart contract, even when the parties realise there was a mistake.

In this respect, the claim that smart contracts are more efficient and carry no legal costs is negated by the rise of ex-ante costs in the form of thorough due diligence and the need to consider an exhaustive amount of scenarios for contracts to be complete. In conditions of low uncertainty, such contracts may be easier to design and execute. However, when uncertainty is high, the exact costs may be high and the range of unanticipated events large.

This would assume that everyone participating in DeFi markets can create and/or meticulously screen smart contracts for any mistakes or intended tricks. Smart contracts require knowledge of both coding and financial products/transactions in a blockchain environment, which implies a high level of financial and digital literacy. To make DeFi accessible for everyone and non-discriminatory, there would need to be a way for less-literate participants to operate in this environment. The advantage of equal access that crypto proponents advocate may therefore be more theory than practice.

A way to overcome these barriers is by finding ‘trusted intermediaries’ that have the knowledge to handle smart contracts (Makarov and Schoar, 2022). But if trusted intermediaries are needed for this market to be attractive, in what sense have smart contracts and the crypto ecosystem really done away with middlemen?

More importantly, the automaticity and anonymity of smart contracts prevents legal recourse. The need to anticipate and prepare for all possible contingencies is both limiting and vulnerable to uncertainty. In fact, according to contract theory, contracts cannot be complete by definition, given the prohibitively high costs of foreseeing every possible scenario (Bolton and Dewatripont, 2004). Hence, the importance of recourse to the legal system, should an unanticipated scenario materialise. The lack of ex-ante structures to allow for the possibility of the unknown is the one feature that may prevent widespread participation and fail to develop further trust in such markets. The lack of legal recourse is perhaps the main impediment to DeFi development.

4.2 Can sustained and sustainable growth be ensured?

Additionally, scaling up such markets requires some big obstacles to be overcome. DeFi protocols rely almost exclusively on the Ethereum network. As more transactions take place, the network faces bottlenecks that reduce transaction speed and the liquidity available. For comparison, Ethereum can currently handle around 30 transactions per second 7 See ‘What’s Ethereum 2.0? A Complete Guide’, Worldcoin, 29 November 2022, https://worldcoin.org/articles/whats-ethereum-2-0. , while Visa has the capacity to handle 65,000 transactions per second 8 See VISA factsheet: https://www.visa.co.uk/dam/VCOM/download/corporate/media/visanet-techno…. . These bottlenecks increase what are known as ‘gas’ fees (transaction fees), with the possibility that certain users will be priced out of DeFi services altogether. Ethereum has announced for future release a change from a proof-of-work (PoW) infrastructure, as used by Bitcoin, to a proof-of-stake (PoS) infrastructure. Along with this migration to a new consensus mechanism, which will enable a higher volume of transactions to be processed, while reducing the energy needed to do so, other features being rolled out or planned could improve the potential for scalability, even though reaching large-scale processing will still take some years 9 Marc Arjoon, ‘How Ethereum will Scale to One Million Transactions Per Second’, CoinShares, 9 August 2022 https://coinshares.com/research/ethereum-1million-tsp. .

Congestion is not the only problem with PoW protocols. They are also very energy-intensive, since multiple validators around the world are working towards solving first the problem that will lead to the validation of the transaction. The first to get to the solution gets the reward for validation, but the remaining validators are not compensated for the energy power they have invested. Makarov and Schoar (2022) argued that that energy consumption in 2021 for PoW activities exceeded the annual energy consumption of Norway or Ukraine. PoS blockchains promise a more sustainable and scalable alternative since it only chosen validators verify the transactions. The criteria for choosing validators is based on their staked coins. While for PoW structures the incentives are created by rewarding the fastest solvers, in the case of PoS, the incentives to behave in a timely and non-malicious way work via the validators’ coins that are at stake – and which they could lose – for the transaction validation. However, PoS is self-reinforcing. The big players (with higher stakes) get even bigger as they do their work as validators and receive compensation in the form of payment.

There is a conflict between the growing pledges of institutional investors to align their portfolios with environmental and social sustainability criteria and the high energy consumption of cryptocurrencies (Gschossmann et al, 2022). Unless crypto adapts, environmental considerations will reduce their popularity. It is also worth noting that the move from PoW to PoS implies a convergence on fewer validators, and therefore the reintroduction of a more centralised system.

4.3 A solution to financial inclusion?

On a global scale, decentralised finance has the potential to reach populations currently excluded from the financial system. With an internet connection and a crypto wallet, any individual can trade, receive a loan, send a cross-border payment, earn interest on an asset or execute other financial transactions that might otherwise require going through a traditional intermediary. For countries with high degrees of financial exclusion and that rely heavily on remittances, digital access to financial services can be very useful. However, in practice, major obstacles remain before the crypto ecosystem can be the solution to financial exclusion.

First and foremost, financial literacy is of crucial importance for people in navigating and understanding the inherent risks of participation in crypto markets. While it is true that DeFi could help people obtain loans when they have been rejected by a bank, the potential for losses is unquestionably higher. In this respect, access to crypto assets may be as much a curse as a blessing. This is true both for developing and developed countries. For instance, the White House plans to task the National Science Foundation in the United States with “social-sciences and education research that develops methods of informing, educating, and training diverse groups of stakeholders on safe and responsible digital asset use” 10 See The White House, 16 September 2022: https://www.whitehouse.gov/briefing-room/statements-releases/2022/09/16…. .

Second, the ecosystem is not fraud-proof. A report from the analytics firm Elliptic showed that in 2021, more than $10 billion was lost in DeFi thefts and scams 11 Taylor Locke, ‘Over $10 billion was stolen in DeFi-related theft this year. Here’s how to protect yourself from common crypto scams’, CNBC, 14 December 2021, https://www.cnbc.com/2021/12/14/common-defi-crypto-related-scams-and-ho…. . Even for a matter as simple as an individual forgetting their private key – the unique code needed to access a crypto wallet – there are no direct means of recourse. From the perspective of a consumer, there are currently inadequate safeguards against disputes, hacks and scams. Coupled with the lack of legal recourse, this points to the high standards of technical competence required for an individual to navigate the DeFi ecosystem. Consequently, DeFi services may ultimately exclude many individuals, or put those without a crypto background into positions of serious risk.

Third, the DeFi system is relatively expensive. In order to compensate for the lack of information on pseudo-anonymous market participants, DeFi must rely on extremely high collateralisation (Aramonte et al, 2022). As a consequence, lending is inaccessible to those who do not already possess sufficient crypto assets. Specifically, borrowers must be willing to collateralise crypto assets worth more in value than the amount they seek to obtain through a loan. It is thus hard to imagine a small business owner or struggling family accessing the lending services offered by decentralised finance.

4.4 A risk to financial stability

Despite representing a small fraction of the financial system (Table 1), the crypto ecosystem can still pose risks to financial stability. ECB Executive Board Member Fabio Panetta (2022) has argued that although accounting for only 1 percent of the global financial system, crypto assets are still bigger than the sub-prime market before the global financial crisis.

A developing and expanding crypto universe means that its weight in total financial transactions and assets owned will also increase. Additionally, it may become more interconnected with the traditional financial system if users participate in both markets and develop cross-market financial products. More interaction means that if there are episodes of great devaluation in the crypto markets, the wealth of investors could be severely affected and have negative effects for the financial system. Section 5 describes case studies that made this very apparent. In addition to this wealth channel, a worsening of market sentiment in crypto markets could also propagate to financial markets. This means that the crypto market could be an additional variable authorities will have to monitor, eventually having to be factored-in when making financial-stability assessments.

The collateral requirements of DeFi may also encourage procyclicality. When the crypto market is running hot, more assets are placed as collateral, fuelling more lending and speculation. However, when the crypto market is bearish, collateral requirements become harder to fulfil, leading to shortfalls in investment activity. In essence, the DeFi industry is inextricably tied to the health of the broader crypto marketplace, exposing it to constant risk. 12 France’s finance minister, Bruno Le Maire, among others, has compared crypto markets to the wild west.

5. Recent distress episodes: a wild west?

Use of Bitcoin began in 2008. However, only in the last half decade have cryptocurrencies and other crypto innovations gained more traction. The evolution of crypto markets has seen significant turbulence, with the failures of some initiatives that appeared both promising and robust. Despite episodes of heightened volatility, the ‘old’ Bitcoin has been resilient to turbulence and remains the most widely used cryptocurrency.

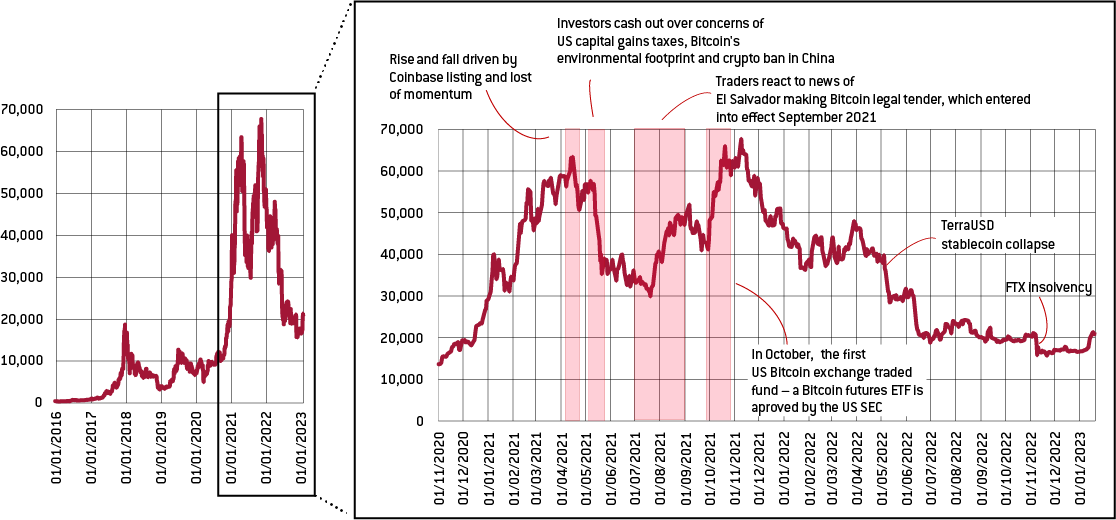

Bitcoin rose steadily in value in 2020, reached a record value in 2021, decreased almost steadily in 2022 and since Q4 2022 has fluctuated within a narrower range between $15,000 and $20,000. Figure 5 shows that Bitcoin was particularly volatile during 2021. Its price fluctuated from around $30,000 at the beginning of 2021 to almost $70,000 in November 2021, an all-time high. As the supply of Bitcoins is based on a fixed algorithm, its inherent volatility derives from fluctuations in demand, which is vulnerable to social media and new announcements. Figure 5 attempts to link some sudden shifts in the Bitcoin price to such announcements. Interestingly, Bitcoin does not seem to be so reactive to monetary policy or macroeconomic announcements, unlike other assets, such as equity indices or commodities (Benigno and Rosa, 2023). Hence, the sensitivity of Bitcoin’s price appears more related to crypto-specific news rather than general policy or economic announcements.

For the first time in Bitcoin’s history, its price against the dollar decreased for four consecutive quarters during 2022. There were various episodes of collapses in relatively new crypto areas: stablecoins and DeFi-related activities. Below, we explore some of these episodes.

While Bitcoin remains the most popular crypto asset, its volatility makes it unattractive for financial transactions. To keep transactions relatively stable and predictable, decentralised finance has turned to stablecoins, which function as a medium of exchange in crypto markets, allowing users to transfer cryptocurrencies into more stable assets without leaving the blockchain ecosystem. It is still unclear, however, how reliable stablecoins really are. As stablecoins and DeFi become more widely used, also with increasing connections to traditional financial services, regulators are growing increasingly concerned about how stablecoins are backed and how exchange trading platforms are managed. Recent distress episodes, in which various parts of DeFi collapsed, demonstrate the importance of good-quality reserves as a basis for enabling financial activity.

Figure 5: Evolution of Bitcoin’s price ($)

Source: Bruegel based on Bloomberg (Bitcoin price against $).

The example of FTX is very indicative in this sense. FTX was a decentralised crypto exchange (dex) platform, equivalent to a traditional stock exchange. Dexes typically hold clients’ assets for extended periods, to facilitate their trading activity. In November 2022, a report written by CoinDesk, a crypto news site, revealed that a bulk of the company’s positions and assets were not held in fiat currency or other cryptos, but in its own native crypto, called FTT. The lack of sufficient diversification in the underlying assets raised concerns about the viability of the company. In response, investors sought to retrieve deposits worth $5 billion, in a classic bank run, which FTX could not cover. On 11 November 2022, FTX filed for bankruptcy, with only $900 million worth of sellable assets against $9 billion of liabilities. This collapse exposed many financial institutions to losses, exposing the links between DeFi and traditional finance. Lack of due diligence in the form of absent corporate controls and poor risk analysis were highlighted as causes of this bankruptcy, and emphasised the need for regulation 13 Laurence Fletcher and Joshua Oliver, ‘Hedge funds left with billions stranded on FTX’, Financial Times, 22 November 2022, https://www.ft.com/content/125630d9-a967-439f-bc23-efec0b4cdeca. .

In May 2022, TerraUSD, the third largest stablecoin, algorithm-backed, was also the first to collapse, raising doubts about how stable such crypto assets can be. But it was not the quality of reserves that generated distress. The TerraUSD stablecoin did not proclaim to be stable because it had the backing of credible collateral assets. Instead, it was an algorithm that adjusted the supply of the currency in an arbitrage trading strategy with a sister cryptocurrency (Luna). This was done automatically by maintaining a nominal peg to the dollar. In that respect, TerraUSD promised to provide stability by just managing the currency peg to the dollar, but without any dollar (or other real-world) assets. At the same time, to attract new users/investors, it offered a deposit rate of 20 percent. For as long as the peg held and the sister cryptocurrency generated enough profits, the system was viable. But as soon as confidence in the sustainability of the peg started to crumble, which it did in May 2022, the peg broke and the system collapsed 14 See Box A of Chapter III of BIS (2022) for a good description of the financial engineering behind TerraUSD-Luna and dollar peg. .

The collapse of TerraUSD spilled over to Tether, the largest stablecoin, which initially saw a collapse in its price and a big outflow of funds, which in turn led to breaking its peg with the dollar. Tether’s reluctance to reveal the quality of its reserves led investors to lose confidence in its ability to support the peg to the dollar, forcing it to break. Furthermore, concerns about the activities behind the world's biggest crypto exchange 15 Tom Wilson, Angus Berwick and Elizabeth Howcroft, ‘Special Report: Binance's books are a black box, filings show, as it tries to rally confidence’, Reuters, 19 December 2022, https://www.reuters.com/technology/binances-books-are-black-box-filings…. , Binance, have led to the opening of investigations by the US Department of Justice. These examples show that concerns over the activities of crypto companies are not exaggerated. Less demand and participation in the market is becoming evident, resulting in more crypto platforms shutting down 16 Vildana Hajric and Isabelle Lee, ‘First NFT ETF Is Closing as Once-Hot Crypto Trend Fizzles’, Bloomberg, 31 January 2023, https://www.bloomberg.com/news/articles/2023-01-31/defiance-digital-rev…. .

6. Regulation steps in to protect and legitimise

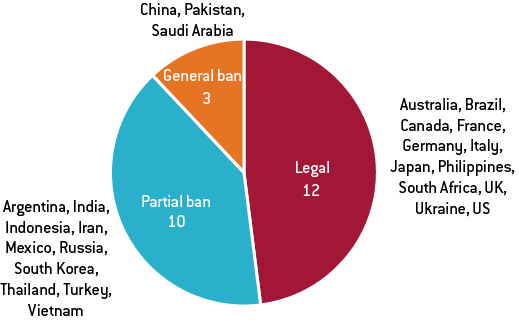

Some countries have prohibited crypto transactions and trading, while others have introduced partial bans in the form of prohibitions on only one or a combination of activities, such as the use of crypto as a means of payment, trading or facilitation by financial institutions (Figure 6). In jurisdictions where crypto is allowed, regulation typically targets entry points to the market, mainly the exchanges, and imposes anonymity and privacy rules. But as the examples in section 5 illustrate, other risks also need to be managed, not unlike the way that regulation manages traditional financial markets. By managing risks, regulation will help legitimise the industry, foster its development and promote crypto innovation.

Figure 6: Legal status of cryptocurrencies in 25 countries

Source: Bruegel based on the Atlantic Council Cryptocurrency Regulation Tracker. Notes: The Tracker includes 25 countries: the G20 countries plus five countries with the highest rates of cryptocurrency adoption.

The decentralised and borderless nature of crypto markets makes them naturally challenging to regulate. Decentralisation alongside anonymisation make it hard to hold someone accountable. As such, some “recentralisation” of DeFi could help regulatory authorities (OECD, 2022). An example of how centralisation is achieved without compromising the decentralised nature of DeFi is via decentralised autonomous organisation (DAO) governance structures, in which only those holding governance tokens can participate and vote on the network’s governance.

Given the borderless nature of crypto activities, regulators should aim for overarching frameworks across countries. The international Financial Stability Board has made an initial proposal for a framework on international regulation of crypto-asset activities, highlighting the “principle of ‘same activity, same risk, same regulation’: where crypto-assets and intermediaries perform an equivalent economic function to one performed by instruments and intermediaries of the traditional financial sector, they should be subject to equivalent regulation” 17 Financial Stability Board, ‘FSB proposes framework for the international regulation of crypto-asset activities’, press release, 11 October 2022, https://www.fsb.org/2022/10/fsb-proposes-framework-for-the-internationa…. . The Organisation for Economic Co-operation and Development has also put forward the Crypto-Asset Reporting Framework (CARF), which provides a basis for standardised exchange of information between jurisdictions on crypto transactions for tax purposes. However, coordination at the global level is still limited and is advancing at different speeds. We describe a few examples of how this is done.

Regulating crypto assets and activities means addressing a fundamental characteristic of crypto– anonymity. To address concerns about money laundering and financing of terrorism, disclosure of identities has been a key point across jurisdictions. For instance, in the United States, since March 2013, cryptocurrency exchanges are classified as ‘money service businesses’ and, accordingly, fall are under the rules of the US Bank Secrecy Act. This means that these services must document the identity of their customers and perform anti-money laundering checks. Similarly, in the European Union, a revision of the 2015 Transfer of Funds Regulation ((EU) 2015/847) will extend to crypto assets the obligation to collect information on the senders and recipients of transfers to crypto funds 18 For the status of the revision, see https://www.europarl.europa.eu/legislative-train/theme-an-economy-that-…. . In the United Kingdom, cryptocurrency exchanges must also comply with anti-money laundering and countering the financing of terrorism (AML/CFT) obligations, and have to register with the Financial Conduct Authority.

To ensure similar treatment to other financial activities there have also been developments in crypto taxation. In the US, guidance on taxing transactions using ‘virtual currencies’ has been around since 2014. But a new provision in the Infrastructure Investment and Jobs Act, in November 2021, additionally requires cryptocurrency exchanges to record information on every purchase or sale of cryptocurrency on their platform and to report it to the US Internal Revenue Service for tax purposes. This provision started applying to trades conducted in 2023, with repercussions for the 2024 tax-filing season. In the UK, taxation depends on the activities and parties involved, but there are provisions indicating the application of standard capital gains tax rules to crypto gains and losses. In India, the government introduced, from April 2022, a 1 percent tax deductible at source on all digital-asset transfers above certain thresholds, and a 30 percent flat tax on ‘virtual digital assets’ gains or income.

The EU Markets in Crypto-Assets (MiCA) 19 Not adopted at time of writing; for its status, see https://www.europarl.europa.eu/legislative-train/theme-a-europe-fit-for…. regulation will set EU-wide rules, overcoming current legal fragmentation across member states and creating a single EU market for crypto assets and activities. Crypto-asset service providers will be required to seek authorisation to offer services in the EU, and will then be supervised by the European Banking Authority. MiCA also covers stablecoins (in the regulation under the names “asset-referenced tokens” and “e-money tokens”) with rules on reserves, redemption plans and consumer guarantees.

Central banks meanwhile have plans to issue their own central bank digital currencies (CBDCs). With the expansion of privately provided cryptocurrencies and financial services, central banks are fearful of the possibility that these private currencies will displace public fiat money and therefore their ability to manage the monetary system. While private digital money is still very small, central banks want to understand the technology behind DLT and the opportunities it could offer in relation to publicly issued money. As many as 98 countries are now at some stage of CBDC exploration, with about 40 central banks at an advanced phase, ie development or pilot 20 https://www.atlanticcouncil.org/cbdctracker/. . Among those in the development phase are the ECB and Bank of England, while an example of advanced stage of piloting is People’s Bank of China. Some countries, where financial exclusion is a significant feature of the system, are already using a CBDC as a way of providing digital payments. Examples include the Bahamas, which has been using the Sand dollar since October 2020, the first CBDC to be launched, and Nigeria with its eNaira, which came into operation in October 2021.

7. Conclusions

The emergence of DLT allowed for the creation of the first digital currency, Bitcoin. Importantly, it provided technology that was secure enough to finalise transactions without any intermediary. The ability for two strangers to transact digitally, quickly and automatically, using a means that can then be converted to real value in fiat currencies was a major novelty.

Also, the macroeconomic environment in which cryptos were created was conducive to risk-taking. As interest rates were very low for a prolonged period, stakeholders were keen to take on risk and to explore new ideas, in particular those promising high returns. In this context, for a while it looked like cryptocurrencies might be real competition for traditional fiat currencies.

As interest rates are now rising and expected to stay high, the appetite for a search for yield, the motive for seeking risk, is also diminished. But more importantly, as our examples demonstrate, financial services that operate in a ‘wild west’ are vulnerable to fraud and bound to lead to abrupt losses. The rules and regulations that govern the traditional financial system have been adopted for good reasons. Also, the claim of decentralisation, doing away with the middleman is increasingly impractical, and the system is now reverting to being centralised around trusted nodes, trusted ‘middlemen’.

Financial regulators have from the start taken a keen interest in the technology and the potential place of crypto assets. However, not rushing to regulate them from the start reflected their inability to categorise them. Were they currencies or were they assets? Are exchanges neutral platforms or do they themselves add risk to the system? With time, consensus has emerged on what type of products crypto assets are, and how the infrastructure around them needs to be monitored to protect the consumer. And even though crypto still represents only a small component of the entire financial system in value terms, policy still needs to monitor how they function, since small components can have amplified effects, as they did in the 2008 sub-prime crisis.

Regulation will also help solve the problem of lack of legal recourse. No system is fool-proof and the DeFi market is no different. Being able to attribute accountability and therefore resolve disputes is necessary for the legitimisation and healthy development of DeFi.

But perhaps the most important limitation of DeFi, in its current form, has to do with how it provides (or not) societal added value. Financial intermediation has the clear purpose of financing productive activities. By contrast, the crypto environment is self-referential. Crypto assets are traded between themselves in search of yield, but not necessarily in search of added value. They are not used to finance productive activities and they only really do so when they are converted into fiat money. For DeFi to challenge the current financial system it will have to bring together borrowers and lenders in ways that produce value added.

Nevertheless, the technology behind them does offer opportunities for efficiency gains that can be exploited, even within the traditional financial architecture. This is also the reason why central banks are taking a keen interest in understanding how they can apply this technology to traditional fiat money. In the years to come, blockchain technology can be expected to be integrated into the financial system, helping increase its efficiency.

References

Aramonte, S., S. Doerr, W. Huang and A. Schrimpf (2022) ‘DeFi lending: intermediation without information?’, BIS Bulletin 57, Bank for International Settlements, available at https://www.bis.org/publ/bisbull57.htm

Benigno, G. and C. Rosa (2023) The Bitcoin–Macro Disconnect, Staff Reports Number 1052, Federal Reserve Bank of New York, available at https://www.newyorkfed.org/research/staff_reports/sr1052

BIS (2022) BIS Annual Economic Report, Bank for International Settlements, available at https://www.bis.org/publ/arpdf/ar2022e.htm

Bolton, P. and M. Dewatripont (2004) Contract Theory, The MIT Press, available at https://mitpress.mit.edu/9780262025768/contract-theory/

Claeys, G., M. Demertzis and K. Efstathiou (2018) ‘Cryptocurrencies and monetary policy’, Policy Contribution 10/2018, Bruegel, available at https://www.bruegel.org/policy-brief/cryptocurrencies-and-monetary-policy

Grassi, L., D. Lanfranchi, A. Faes and F.M. Renga (2022) ‘Do we still need financial intermediation? The case of decentralized finance – DeFi’, Qualitative Research in Accounting & Management 19(3): 323-47, available at https://doi.org/10.1108/QRAM-03-2021-0051

Gschossmann, I., A. van der Kraaij, P.-L. Benoit and E. Rocher (2022) Mining the Environment – Is Climate Risk Priced into Crypto-Assets? European Central Bank, available at https://www.ecb.europa.eu/pub/financial-stability/macroprudential-bulletin/html/ecb.mpbu202207_3~d9614ea8e6.en.html

Kakinuma, Y. (2023) ‘Hedging role of stablecoins’, Intelligent Systems in Accounting, Finance and Management 30(1): 19–28, available at https://doi.org/10.1002/isaf.1528

Makarov, I. and A. Schoar (2022) ‘Cryptocurrencies and Decentralized Finance (DeFi)’, Working Paper 30006, National Bureau of Economic Research, available at https://doi.org/10.3386/w30006

OECD (2022) Why Decentralised Finance (DeFi) Matters and the Policy Implications, Organisation for Economic Co-operation and Development, available at https://www.oecd.org/finance/why-decentralised-finance-defi-matters-and-the-policy-implications.htm

Panetta, F. (2022) ‘For a Few Cryptos More: The Wild West of Crypto Finance’, speech by Fabio Panetta, Member of the Executive Board of the ECB, at Columbia University, available at https://www.ecb.europa.eu/press/key/date/2022/html/ecb.sp220425~6436006db0.en.html

US Treasury (2022) The Future of Money and Payments - Report Pursuant to Section 4(b) of Executive Order 14067, US Department of the Treasury, available at https://home.treasury.gov/system/files/136/Future-of-Money-and-Payments.pdf

About the authors

Related content

The European Central Bank’s timid operational framework update

The European Central Bank announced limited changes to its operational framework – which is probably right given current uncertainty

The European Central Bank, inflation tolerance and the last mile

Climate change, the next big financial threat

A warming planet poses new risks to European sovereign debt. How can the continent protect itself?

Next steps for the European Anti-Money Laundering Authority

At this invitation-only event Raluca Pruna discussed the state of the legislation to create an EU Anti-Money Laundering Authority