Asset-backed securities: The key to unlocking Europe's credit markets?

Direct European Central Bank intervention in the market for asset-backed securities (ABS) has the potential to become, under certain conditions, a mec

The European market for asset-backed securities (ABS) has all but closed for business since the start of the economic and financial crisis. ABS (see Box 1) were in fact the first financial assets hit at the onset of the crisis in 2008. The subprime mortgage meltdown caused a deterioration in the quality of collateral in the ABS market in the United States, which in turn dried up overall liquidity because ABS AAA notes were popular collateral for inter-bank lending. The lack of demand for these products, together with the Great Recession in 2009, had a considerable negative impact on the European ABS market.

The post-crisis regulatory environment has further undermined the market. The practice of slicing and dicing of loans into ABS packages was blamed for starting and spreading the crisis through the global financial system. Regulation in the post-crisis context has thus been relatively unfavourable to these types of instruments, with heightened capital requirements now necessary for the issuance of new ABS products.

And yet policymakers have recently underlined the need to revitalise the ABS market as a tool to improve credit market conditions in the euro area and to enhance transmission of monetary policy. In particular, the European Central Bank and the Bank of England have jointly emphasised that:

“a market for prudently designed ABS has the potential to improve the efficiency of resource allocation in the economy and to allow for better risk sharing... by transforming relatively illiquid assets into more liquid securities. These can then be sold to investors thereby allowing originators to obtain funding and, potentially, transfer part of the underlying risk, while investors in such securities can diversify their portfolios... . This can lead to lower costs of capital, higher economic growth and a broader distribution of risk” (ECB and Bank of England, 2014a).

In addition, consideration has started to be given to the extent to which ABS products could become the target of explicit monetary policy operations, a line of action proposed by Claeys et al (2014). The ECB has officially announced the start of preparatory work related to possible outright purchases of selected ABS1.

In this paper we discuss how a revamped market for corporate loans securitised via ABS products, and how use of ABS as a monetary policy instrument, can indeed play a role in revitalising Europe’s credit market.

However, before using this instrument a number of issues should be addressed:

First, the European ABS market has significantly contracted since the crisis. Hence it needs to be revamped through appropriate regulation if securitisation is to play a role in improving the efficiency of resource allocation in the economy.

Second, even assuming that this market can expand again, the European ABS market is heterogeneous: lending criteria are different in different countries and banking institutions and the rating methodologies to assess the quality of the borrowers have to take these differences into account. One further element of differentiation is default law, which is specific to national jurisdictions in the euro area. Therefore, the pool of loans will not only be different in terms of the macro risks related to each country of origination (which is a ‘positive’ idiosyncratic risk, because it enables a portfolio manager to differentiate), but also in terms of the normative side, in case of default. The latter introduces uncertainties and inefficiencies in the ABS market that could create arbitrage opportunities.

It is also unclear to what extent a direct purchase of these securities by the ECB might have an impact on the credit market. This will depend on, for example, the type of securities targeted in terms of the underlying assets that would be considered as eligible for inclusion (such as loans to small and medium-sized companies, car loans, leases, residential and commercial mortgages). The timing of a possible move by the ECB is also an issue; immediate action would take place in the context of relatively limited market volumes, while if the ECB waits, it might have access to a larger market, provided steps are taken in the next few months to revamp the market.

We start by discussing the first of these issues – the size of the EU ABS market. We estimate how much this market could be worth if some specific measures are implemented. We then discuss the different options available to the ECB should they decide to intervene in the EU ABS market. We include a preliminary list of regulatory steps that could be taken to homogenise asset-backed securities in the euro area. We conclude with our recommended course of action.

The European ABS market: evolution and current size

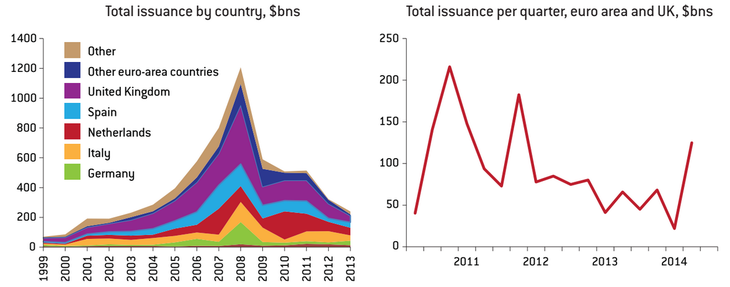

The ABS market peaked in Europe before the crisis, with a total of $1.2 trillion in new ABS issuance in 2008. By 2013, total new issuance was only $239 billion (Figure 1). Demand for these assets plummeted after 2008 because of the deterioration in the rating of the collateral behind the various types of ABS, leading to a major market price correction of ABS products.

Figure 1: New issuance in the EU ABS market, 1999-2013 (2014Q2)

Source: SIFMA (July 2014).

Moreover, the freeze in European inter-bank lending reduced demand for these assets as collateral for repurchase (repo) agreements (in other words, agreement to sell an asset and buy it back at a later date). In particular, after the start of the financial crisis in 2007-08, the ECB progressively tightened the rating and structural requirements for ABS it would accept as repo collateral, with the result that using ABS as repo collateral became expensive, in particular compared to covered bonds. Hence, after 2008, the amount of eligible ABS declined by 38 percent while covered bonds increased by 14 percent, until in mid-2012 covered bonds overtook ABS as delivered repo collateral for the first time since 2007.

A final blow to the ABS market during the crisis came from the insurance sector. Insurance funds, traditionally large buyers of ABS products, were also negatively impacted by the introduction of more restrictive regulation in response to the crisis, and consequently limited their ABS purchases.

Country-by-country, the smallest players in the market (eg Belgium and Ireland) saw a decrease in new issuance of more than 95 percent from the peak, while, among the main issuers, new issuance in Italy, the Netherlands and Spain dropped by about 73 percent. In Germany, the decline was 80 percent. It is interesting to look at the United Kingdom: here, new issuance represented almost a third of total European issuance on average until 2008, but after the peak, UK flows dropped by 90 percent, with new issuance in 2013 representing less than 20 percent of the European total. Considering this change in the UK’s role in the structured product market, new issuance in the euro area rose to 73 percent of total European new issuance in 2013, from 63 percent in 2008. However, in volume terms, euro-area issuance was slashed from $766 billion to $175 billion.

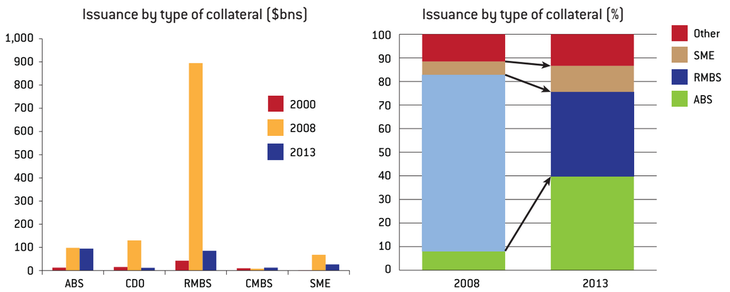

Interestingly, the collateral behind the ABS products also varied during the crisis, with the collapse in the issuance of Real Mortgage Backed Securities (RMBS) and European Collateralised Debt Obligations (CDOs), with issuance of both dropping by 90 percent between 2008 and 2013 (Figure 2). The composition of overall issuance thus changed, with a (relative) increase in ABS with consumer credit as collateral, and a marginal increase in ABS backed by loans to small and medium-sized enterprises.

Figure 2: Breakdown of ABS issuance per type of collateral, various years

Source: SIFMA (July 2014).

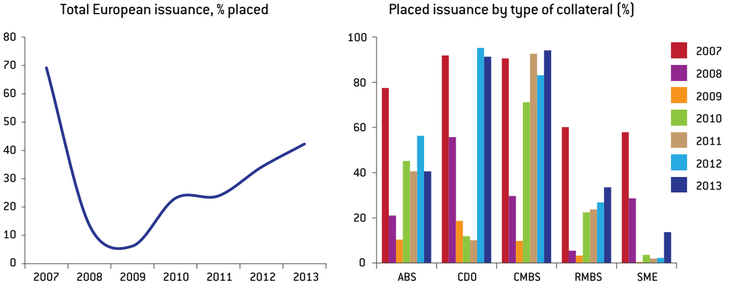

Another indication of the reduction in the liquidity of this product is the amount of new issuance placed on the market relative to ABS retained by originators, such as banks that package securitised products (Figure 3). Before the crisis, almost 70 percent of new issuance was placed on the market, and the remainder retained by originators. After 2008, the share of new issuance placed on the market dropped to below 10 percent, signalling virtual market refusal of these securities. More recent figures point to a market placement rate of about 40 percent, though at much lower overall volumes.

Figure 3: Retention rate of ABS products, various years and type of collateral

Source: SIFMA (July 2014).

However, originator retention rates vary by type of instrument. Despite the dramatic reduction in issuance of CDO and Commercial Mortgage Backed Securities (CMBS), currently around 90 percent of their new issuance is placed on the market, probably because of demand from specialised investors, who could no longer find these securities on the market. By contrast, there is weaker market demand for RMBS, generic ABS (car loans, leases, etc) and SME ABS. In particular, almost all new SME ABS are retained on banks’ balance sheets, with only 10 percent placed on the market.

What is the potential for an increase in the size of the ABS market?

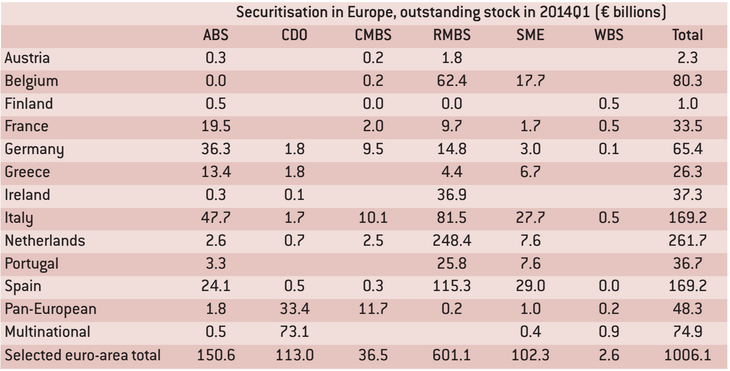

The outstanding amount of European securitisation, at the end of 2013, was approximately €1 trillion, of which roughly half was placed on the market (Table 1 on the next page). For comparison, at its peak in 2008, the overall outstanding amount of the ABS market reached more than €2.2 trillion. About 60 percent of the market (€637 billion) is made up of mortgage-backed securities (residential and commercial), followed by standard ABS (car loans, leases, etc) with a volume of €150 billion, and SME ABS for €102 billion. CDOs stood at €113 billion.

Table 1: Total outstanding amount of EU securitised products

Source: SIFMA data Q1-2014.

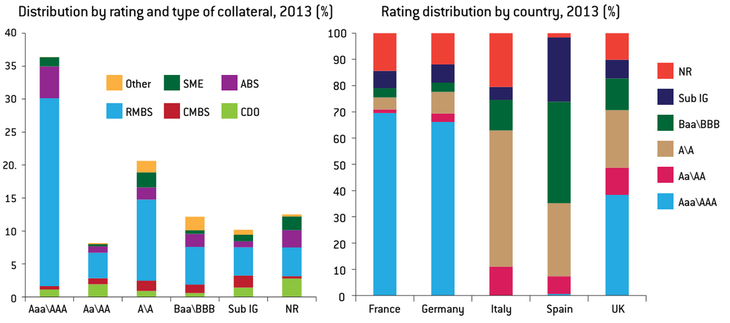

The quality of these securities varies in terms of collateral type, with about 77 percent of the amount outstanding rated above BBB, and therefore eligible for collateral transactions with the ECB3 (Figure 4). The highest presence of high-rated securities is in France and Germany, while Italian and Spanish ABS are more concentrated in the ‘single A’ category, in line with the evolution of the sovereign ratings in these countries. In terms of collateral type, SME ABS are the lowest quality, probably due to the heterogeneity of the collateral and the deterioration of companies’ balance sheets during the crisis. Moreover, in the case of SMEs the quality of financial information reported in balance sheets is in general less regular and accurate, an issue that also impacts negatively on the rating, because it implies a more negative assessment of the probability that loans will be repaid. From 30 to 40 percent of SME ABS are currently estimated to be sub-investment grade or not rated. Italy and Spain are also the countries with the main outstanding volumes of SME ABS.

Figure 4: Rating of ABS products per type of collateral and country, 2013

Source: SIFMA

Given these figures, what potential for growth does the ABS market have overall, on the basis that potential ECB purchases could create sufficient demand to revitalise the market?

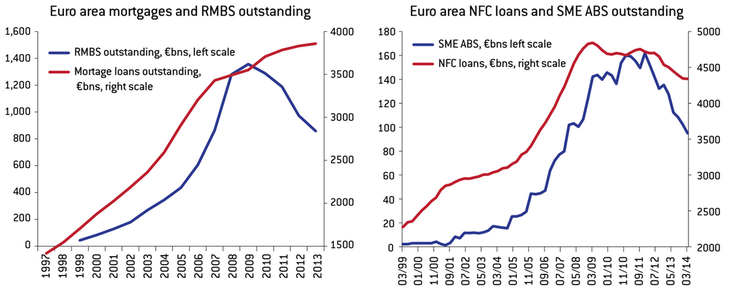

Looking at the markets for collateral, data from monetary financial institutions shows (Figure 5) that the outstanding amount of mortgages for house purchases (thus secured lending) stabilised at about €3.8 trillion in 2013 in the euro area, while the outstanding amount of bank loans to non-financial corporations (NFC) in the euro area reached about €4.2 trillion. Figure 5 also compares the trend in the mortgage market to that in the RMBS market (left panel), and NFC loans to SME ABS (right panel).

In both cases, there has been an evident fall in volumes of both types of securitised product, with SME ABS performing relatively worse. The reason is the contraction of credit demand coupled with bank deleveraging, leading to a contraction of NFC loans, compared to relative stability in the volume of mortgage loans outstanding. Hence, collateral for SME ABS operations has been squeezed relatively more compared to RMBS. Moreover, one has to consider the negative regulatory impact on capital requirements associated with the issuance of this type of product.

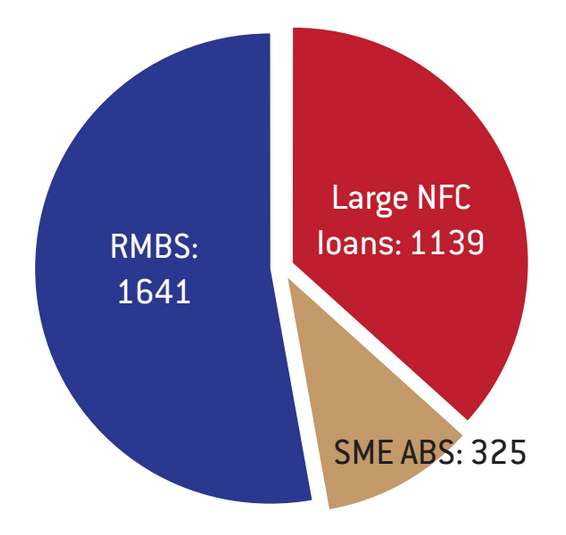

The question is, then, how much of these outstanding volumes of loans to NFCs or mortgage loans worth €8 trillion could be translated into new issuance of RMBS and SME ABS. In line with Batchvarov (2014), we make estimates on the basis of mortgage loans to households and loans to non-financial corporations, for the countries that represent 80 percent of the total portfolio of outstanding loans in the euro area (Germany, France, Italy, Spain, Ireland and Portugal). The share of SME loans in total NFC loans, as estimated by the OECD (2013), varies between these countries. Applying these shares to the euro area, the implied euro-area SME ABS share is approximately 25 percent of total outstanding NFC loans.

On the basis of the conservative assumption that only 50 percent of the €8 trillion of existing loans is ultimately eligible for securitisation (eg for reasons of maturity or loan characteristics), we then introduce a different haircut so that the securitised products attain an investment grade rating (to be eligible as a collateral for the ECB). Unlike the standard assumption of a homogeneous 10 percent haircut for subordination for all categories of assets (Batchvarov, 2014), we apply a more prudential and differentiated haircut for the three main categories of assets selected, as retrieved from updated statistics for these securities (SIFMA): 35 percent for SMEs loans, 30 percent for ABS backed by loans to large corporations, and 15 percent for mortgages.

Based on this, we estimate a maximum amount of securitisation of roughly €3 trillion (compared to €4 trillion estimated by Batchvarov, 2014), broken down as shown by Figure 6 on the next page. It should be noted that SME ABS would represent the smallest fraction (about 10 percent) of this market.

Figure 6: Estimates of potential ABS market for the euro area (€ billions)

Source: Bruegel.

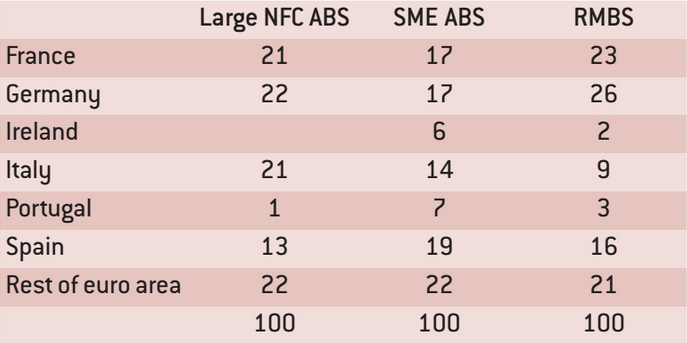

Table 2 on the next page shows that the estimated breakdown of the potential overall ABS market by country will vary according to the size and composition of each country’s underlying market for collateral5: Germany, France and Italy would each represent almost 20 percent of the total NFC-loan ABS, while in terms of SME ABS, Spain would count for a fifth of the whole amount, with Germany and France accounting for about 17 percent each. The role of Germany is also significant in the RMBS market, representing about 26 percent of the outstanding amount, followed by France, Spain and Italy.

Table 2: Potential availability of ABS per country (%), est.

Source: Bruegel estimates based on MFI data (March 2014) and OECD

The revival of the ABS market: the options

Our estimates show that the euro-area securitisation market has the potential to build significant volume and to be sufficiently liquid for use in possible non-conventional monetary operations. However, a number of trade-offs must be considered relating to the timing of ABS market measures, and the underlying size of the market at that moment: the earlier that measures are taken, the more restricted will be the type of ABS product that can be targeted for direct purchase (eg SME ABS only), reducing the impact of potential ECB operations on credit markets.

These trade-offs arise because the current securitised products on the market differ in terms of underlying characteristics, ie collateral type and thus rating, borrowers’ quality and geographic distribution, loans’ residual maturity, frequency of repayment, cost of credit, type and amount of interest (fixed or variable), prepayment rates and possible credit enhancements built into the structure6. Because of these heterogeneous characteristics, only a fraction of existing ABS products are ‘ready to use’, if ever, by the ECB. Moreover, within the existing range of products, there are different implications of the ECB targeting for direct purchase only SME ABS rather than RMBS. Undertaking specific regulatory steps aimed at standardising the characteristics of securitised products in different countries might allow the full activation of the estimated €3 trillion in potential ABS market volume, but reaching such a figure would require time for implementation.

In the following sections we detail the ECB’s options.

Option 1: Act small and fast

Option 1 would involve the direct purchase of very simple (‘plain vanilla’) existing ABS products with corporate credit exposure7. By pursuing this option, the ECB could act immediately, but would have a limited direct impact on credit markets. Existing ABS products limited to SMEs loans amount to €102 billion (Table 1). If the lease component of generic ABS is included, one could add a further €15 billion8. With respect to these figures, the volume of securitised products available for immediate use with a rating above investment grade is 60 percent of SMEs ABS and 50 percent of the lease components. As a result, with these constraints, the maximum theoretical size of the ABS market for immediate ECB intervention is about €68 billion. This is probably not enough to generate a direct impact on credit conditions in the euro area.

This does not imply, however, that there is no role for an ABS market backed only by corporate credit exposure, even in its current form. In the wake of the crisis, origination of ABS products has been subject to the introduction of stricter regulations on capital requirements for insurance companies, and on risk-weighted assets for banks (see Annex 1 for a summary of ABS capital requirements/risk weights)9. Within the current set of rules, therefore, any type of non-conventional monetary policy under which ABS assets are purchased will ultimately free up capital in banks’ balance sheets. This is particularly true for SME ABS, since their average rating is low and therefore the capital absorption for senior tranches below AAA is huge and greater than capital absorbed by the loans themselves. Consequently, ECB intervention in the ABS market, even if potentially limited in size, could magnify the effects on credit origination of the ECB's targeted longer-term refinancing operation (TLTRO), announced in June 2014, although the exact additional magnitude of these effects is hard to predict.

Option 1 could thus be a way of solving the trade-off for the ECB: intervening immediately in the relatively small (at its current volume) ‘plain vanilla’ ABS market, but limiting the scope of the operation to an ‘indirect’ vehicle through which the effects of the TLTRO could be magnified.

Option 2: Act large and slow

Option 2 essentially implies reviving, deepening and integrating the euro-area ABS market so it can be used as a new tool for non-conventional monetary policy. The ECB and the Bank of England (2014b) point at improving the regulatory environment for ABS products to better differentiate the necessary prudential requirements for relatively simple, robust and transparent ABS products (eg consumer finance ABS, RMBS and SME ABS) from more complex and potentially illiquid instruments. By revamping this market, these instruments could be used effectively as a ‘direct’ vehicle through which non-conventional monetary operations could be run. Clearly, the trade-off here is that developing the latter would require a number of changes to underlying regulation, and would thus take time.

To achieve a high-quality, simple and transparent European ABS product, two areas of regulatory change should be developed: one on collateral rules, for the corporate loan market in particular; the other on ABS product characteristics, ie the format to be applied to various types of ABS10.

Collateral rules

Regarding the rules on collateral, two issues should be addressed:

1 More selective regulation on capital requirements

ABS are a tool that could provide more flexibility to financial institutions to achieve better capital ratios throughout the system, and to reduce leverage ratios, since securitisation, when sold by originators, would enable reductions in risk weighting. Changes in ABS risk weighting could lead to high-quality, simple and prudently-structured securitisation products receiving more consistent regulatory treatment across financial legislation11. In particular, regulators could work to reduce the discrepancy between regulatory treatment of ABS and collateral12.

During 2013, progress was made on financial regulation, but further steps are necessary as part of the implementation of the Capital Requirements Directive IV to clarify whether and to what extent ‘European’ ABS would count as regulatory liquidity, the future risk weights they will have for securitisation in the banking and trading books and the extent to which their rating would be correlated with the sovereign credit rating of the originating country13.

As far as insurance regulation is concerned, in relation to the Solvency II directive (which is to enter into force in 2016), the European Insurance and Occupational Pension Authority (EIOPA) is also examining regulatory capital requirements for insurers’ ABS investments, in order to reduce capital requirements for insurance companies.

2 More transparent and available information on collateral

In order to stimulate further the market for ABS, especially for SME loans, common guidelines on a minimum level of information to be reported in SME balance sheets should be agreed, in line with the ECB eligibility requirement that loan-level data should be publicly available. Balance sheets thus produced should be made available to originators, in order to increase transparency and comparability of collateral. At the same time, rules on standardised rating methodologies for securitised products should be enforced within the Single Supervisory Mechanism.

The homogenisation of company reporting, to also encompass non-listed companies, will enable analysis of the performance of individual companies in European countries, and will facilitate access to credit at the same cost for companies within the same sector in different countries. In addition, steps towards the coordination of default laws in different countries should also be undertaken, to reduce uncertainty for bondholders in case of defaults.

ABS product characteristics

Two issues also need to be addressed in terms of the format of securities:

1 Common guidelines on ABS structure

The risks of ABS are embedded not only in the type of underlying collateral that is securitised, but also in the way collateral is sliced and packaged (see Box 1 for an overview of the basic elements constituting an ABS product).

A common structure for each type of collateral would ease the origination process and imply that the spread between different bonds in each rating category would depend only on differences between collateral characteristics (such as geographical distribution, maturity or the legal framework applying to default). Common structure could tremendously boost market liquidity. Also, the cost of creating the instruments should decrease, as pan-European banks will be able to leverage the size of their loan pool across European markets. With a common structure, the rating framework should become more homogeneous as well, cutting the cost of providing ratings and making the European ABS market much more similar to the US market. Ratings will become more closely related to collateral characteristics and less to the sovereign rating of the originator, and monitoring by rating agencies during the life of the product will focus more on collateral evolution. A straightforward way of achieving this result would be to build on the idea, already hinted at by the ECB, that only an ABS format with a ‘plain vanilla’ structure would be eligible for purchase by the ECB.

2 Common guidelines on the setup of SPVs within national borders

Another key factor in the underlying heterogeneity of the securitisation process is also related to the different role that the ‘Special Purpose Vehicle’ (SPV) might acquire (see Box 1). The SPV is a unique entity the role of which is the acquisition of an identified pool of assets. The SPV is the holder of the collateral within the securitisation. The owner of the SPV, whether it is the originator or a pool of originators, bears the risk of the SPV. A possible guideline is that an originator could establish only one SPV for all the transactions of the same type to be issued, instead of one SPV for each transaction. In the case of a single SPV for all transactions, since the vehicle is immediately available, transaction costs will diminish and the process of securitisation will speed up.

In cases in which a group of originators considers creating a common SPV for the ABS market (whether or not specialised by type of collateral) the risk will be borne by the owners of the SPV. A Banque de France initiative to re-start the securitised SME loan market has worked along these lines.

The creation of a joint SPV within national borders allows for sharing of set-up and operating costs. Standardised legal documentation used by the originators will also reduce costs and operational frictions, and make the SPV a very efficient credit claims mobilisation tool. Whether such a set-up is legally compatible with each country's legal framework, and whether such a choice could be more efficient from the market point of view, are however open questions. The answer in part would depend on the risk weighting assigned to the shareholders of the SPV.

Another reason for the creation of a joint SPV is that, once a common ABS structure with the same collateral type is defined ex ante, there will be less flexibility or creativity in the structuring phase, so that certain type of collateral, if available in volumes that are insufficient to respond to the structuring requirements (such as over- collateralisation criteria), could not be used. While in the past the lack of assets to create credit enhancement in the form of over-collateralisation was compensated for by other forms of internal or external credit enhancement, the absence of this choice in the new system could place a limit on the participation of small and medium players in the ABS market, because of lack of collateral. The problem could however be circumvented through the creation of an SPV at national level, or jointly created by small originators. This would stimulate more consolidation of the banking sector within countries.

In summary for option 2, we can conclude that, under the Single Supervisory Mechanism headed by the ECB, there is ample room to refine all the existing regulation, as we have discussed, in order to create a large pan-European market for simple, robust and transparent ABS products. However, it is also clear that, because of the time it will take to implement the necessary regulatory changes, these developments might only be relevant for the next business cycle, unless this process is accelerated.

Option 3: Act bold

If direct outright purchases in the ABS market are really meant to significantly enhance the functioning of the monetary policy transmission mechanism within the next few months (ie working immediately, and not just as potential amplifiers of the TLTRO), there is a third alternative to the fast/small versus slow/large options we have analysed. A further option, already suggested by Claeys et al (2014), is the direct purchase of RMBS.

An RMBS purchase programme would have a much greater impact on the economy, given the size of the market already at current volumes, ie €601 billion (Table 1), which becomes some €500 billion of targetable products once the minimum rating eligibility criteria are applied15 .

On top of the size of the market, the argument for RMBS purchases also stems from the potential limited impact that the purchase of SME ABS (option 1) might have in terms of the ECB objective of combating the risk of deflation within the cycle. Even assuming that new loans stimulated by the TLTRO and SME ABS purchases ultimately foster the transfer of central bank liquidity directly to the productive sector of the economy, thus restarting credit markets in the euro-area periphery, part of this additional liquidity might have a muted effect on demand. This could happen because companies face a restructuring phase to increase productivity. Therefore, the additional liquidity companies will receive might be used partly for capital expenditure, helped by low rates, and partly for consolidation within sectors, both within or between countries, with a muted effect on employment.

In other words, intervention aimed at increasing the flow of credit to the economy (TLTRO and direct purchase of SME ABS) might have positive effects on demand, and thus consumer prices, only later in the cycle, ie they might not be immediately successful in countering deflation.

Nevertheless, considering that in Europe a relatively low share of households’ wealth is invested in the stock exchange, but a relatively high share is invested in the housing sector, intervening with outright purchases in an ABS market in which RMBS are also considered might have a larger, more immediate effect in revitalising the demand side of the economy, and therefore putting a floor on the trend of declining inflation within the euro area. In this sense, RMBS purchases would not only act as a mechanism to unlock credit markets in the euro area, but would rather be closer to a form of quantitative easing.

In fact, the improvement in banks’ balance sheets would be marginal (given the lower capital absorption of these instruments), while clearly a careful assessment should be made of the need to minimise the impact of RMBS purchases on house prices (and the ensuing wealth effects for households) in the euro area, in order to avoid new bubbles, or to stop the correction of existing ones. While the monitoring exercise now routinely carried out as part of the Excessive Imbalance Procedure can be deployed to avoid such a risk, the fiscal implications of these actions should nevertheless be carefully assessed.

Conclusions

Our evidence shows how direct ECB intervention could turn ABS products into one of the mechanisms that could unlock credit markets in the euro area.

A number of trade-offs arise in terms of the speed and efficacy of the actions that the ECB could take. Acting immediately on existing ABS products (SMEs and corporate-backed eligible ABS) is likely to produce little direct effect, given the small relative size of the targetable market, estimated at some €68 billion. However, an indirect and not necessarily insignificant effect can arise through this action, through the freeing up of capital on banks’ balance sheets, and thus the possibility to exploit on a larger scale (as more loans can be granted with the same amount of capital) the opportunities available through the new TLTRO programme.

Working on the improvement of the regulatory environment for ABS products might revamp a market that can be conservatively estimated at some €3 trillion for the euro area (€1.6 trillion in RMBS and €1.4 trillion in corporate-backed ABS, of which about €300 billion in SMEs ABS), but these actions require time for implementation.

Finally, resorting to the purchase of existing RMBS can achieve the target of an intervention that is both immediate and sizeable in terms of targetable instruments (we estimate a volume of about €500 billion). The characteristics of euro-area credit markets especially favour this option if, notwithstanding a revamped flow of credit to the economy, deflation risks remain critical over the next few months. However this option is closer to a form of quantitative easing and has implications for fiscal policy, and thus should be considered with care.

On the basis of the above, we recommend parallel actions to be taken by the European institutions at the same time. In particular:

- From a regulatory point of view, the resolution of the ongoing uncertainty about the selective treatment of ABS products in terms of capital requirements in the context of the implementation of the Basel III agreements for banks and insurance companies, should take priority over other pending issues;The European Commission and the ECB should start work on a common set of guidelines on data availability and reporting for collateral (loans), and on the definition of a simple and transparent ‘European’ ABS format (structure/set-up of the SPV);

- In the near future, the ECB should start a programme of direct purchases of SME ABS (our option 1), while monitoring the indirect effects this might have on the TLTRO. If deflationary risks persist, notwithstanding positive developments in the credit market, the ECB should also consider purchases of RMBS.

About the authors

Related content

COVID-19 financial aid and productivity: has support been well spent?

In the EU, this support has prevented the emergence of unemployment and has kept average employment high.

EU recovery plans should fund the COVID-19 battles to come; not be used to nurse old wounds

In its proposed Recovery Fund, the European Commission uses allocation criteria mainly linked to infection rates and past economic performance. To fos

Remaking Europe: the new manufacturing as an engine for growth

Europe needs to know how it can realise the potential for industrial rejuvenation. How well are European firms responding to the new opportunities for

The knowns and unknowns of the European competitiveness debate

Micro-economic features of economic systems can have a major impact on national performance. Policymakers should therefore reconfigure their scoreboar