Why we should not blame the ECB for low returns on German savings

The ECB has lowered its official interest rate several times in the last years and the rate is now at zero. In March of this year, it has in addition

This piece was originally published in Die Welt.

The ECB has lowered its official interest rate several times in recent years and the rate is now at zero. In March this year, it started in addition a large sovereign bond purchase programme. German commentators have been focusing on the negative effect of ECB policy on returns on German savings. Contrary to popular belief, however, the ECB is not the main driver of the decline in interest rates. The debate also ignores the appropriate policy response to the decline in interest rates.

Nominal interest rates have been falling for 30 years now. While in 1980, the US governments’ borrowing costs on a 10 year horizon amounted to around 13%, they declined to 8% in 1990, 5% in 2000 and to only 1.9% in April 2015. A similar picture emerges for Germany, where yields for the same type of bond falling from around 9% in 1980, to 5% in 2000 and now to 0.1%.

So what is behind this dramatic fall in interest rates, observed over the past 3 decades? Two factors are central: firstly the fall in inflation, and secondly the fall in real returns. Turning to the former, inflation rates in the 1980s were at about 3% in Germany; for the 2000s at 1.6% and currently the inflation forecast for the next 10 years is at 1.4% for the euro area. A similar picture emerges for the US.

A large part of the fall in interest rates is due to the falling inflation rates

A large part of the fall in interest rates is thus due to falling inflation rates. This is a success of better monetary policy management. Falling inflation rates do not reduce the return to savers. In fact, what matters for savers is the so-called real interest rate. Put differently, as a saver, I am interested in how many goods I can buy from the interest I receive from my savings, and this is measured by the real interest rate.

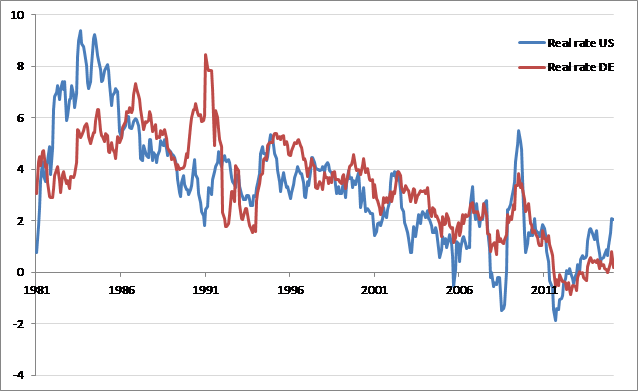

How have real interest rates developed? In both the US and Germany, real interest rates have fallen from levels of about 4% to levels closer to 1% (see graph). With the recent economic upturn, real rates seem to have increased again.

Graph: ex-post real rates (US and DE).

Source: ThomsonReuters Datastream

So what drives this decline in real interest rates? Real rates are determined by a whole set of economic factors, including growth prospects. Ultimately, it is economic performance that drives the return in investments. In a fast growing economy that is still building up its capital stock, real rates should be high as economic growth prospects are high. The opposite is true for an economy in a recessionary environment or an economy with already high capital stocks.

Long-term falling growth prospects are one of the main drivers of low real interest rates

Long-term falling growth prospects are therefore one of the main drivers of low real interest rates. This so-called secular stagnation is explained by demographic developments, increasing capital stocks and an absence of reforms. Moreover, the still rather weak economic outlook in the eurozone is also to be blamed for low returns on savings. Savers will not be awarded a higher interest rate simply because savings are plentiful and investment is low in a recession.

As the reasons behind low real rates are linked to secular stagnation, I would argue that an appropriate set of structural reforms is urgently needed to allow for proper business opportunities and innovation in the industrialized world. This is also particularly important in Germany. German corporations tend to invest abroad rather than in Germany, a development that is shown by the huge current account surplus, and is actually a concern which reflects the weakness of investment opportunities and the lack of demand in Germany. In addition to reform, the demand shortage needs to be addressed with public investment and reduced taxes on low-income households.

The ECB has only reacted to the weak economic situation and has reduced its interest rate to adapt to the weakening economy. The role of the ECB is to achieve the appropriate increase of inflation to its mandate of close but below 2%. Any premature move on increasing the interest rate would hamper the weak economic recovery. The resulting recession would keep investment depressed and returns low.

we have to ask what the right policies should be to address secular stagnation

The discussion therefore has to go beyond blaming the ECB for doing its job. Instead, we have to ask why real interest rates have been falling for so long, and what the right policies should be to address “secular stagnation”. Germany should implement substantial structural policies that increase domestic investment opportunities, thereby redirecting some of the savings to the German economy. It should also increase public investment in order to boost its long-term growth potential. Finally, Germany needs policies that ensure that low income households see their incomes raise and increase their consumption. Only with these changes in place can German savers expect to see their returns rising again.

Related content

The European defence industrial strategy: important, but raising many questions

The European defence industrial strategy helps to focus thinking but has significant flaws

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

The EU needs a methodology for including reform impacts in fiscal trajectories

Such a methodology, and a governance mechanism for managing associated risks, must be in place before the new fiscal framework kickstarts in September

Incorporating the impact of social investments and reforms in the European Union’s new fiscal framework

This paper proposes an approach for quantifying the impact of public investments and reforms on debt sustainability