Who pays for the EU budget rebates and why?

A complex system of EU budget revenue corrections has been developed since the mid-1980s. I quantify their impacts: which countries pay and benefit fr

The question of ‘rebates’, or revenue corrections, is one of the hot topics of the discussion about the next seven-year EU Multiannual Financial Framework (MFF). Since the mid-1980s, a complex system of corrections has been built up. This includes several different types of corrections with hard-to-justify rates of reductions, necessitating burdensome computations and retroactive revisions.

As a Commission staff working document notes (see page 10), rebates are not included in EU treaties, but resulted from political compromises, as concluded by the Fontainebleau European Summit in June 1984: "any Member State sustaining a budgetary burden which is excessive in relation to its relative prosperity may benefit from a correction at the appropriate time". The Fontainebleau Summit concluded a correction to the UK’s contribution (“UK rebate”) and a reduction to the German contribution to the UK rebate (“rebate on the rebate”). These precedents gave rise to a number of other corrections mechanism too (see e.g. a brief summary at the Commission webpage and a longer account by Alessandro D'Alfonso).

The list of rebates and other corrections

UK rebate: Since 1985, the UK has been entitled to a financial rebate of about 66% of its net contribution to the EU budget of the previous year. While the basic concept of the UK rebate has remained the same, the formula to calculate it has been amended many times, making the calculations demanding, and led to a complicated system of rebates. The UK rebate is adjusted retroactively up to three years later, as new information becomes available (see Box 2 in our paper for the current rebate formula). In 2014-2018, the UK rebate averaged €5.6 billion a year.

Rebates on the UK rebate: In principle, the cost of the UK rebate is divided among the other EU member states in proportion to their share in EU's Gross National Income (GNI) (excluding the UK), but there are exceptions. In 1985-2001, Germany paid only two-thirds of its normal share in the UK rebate, while since 2002, Austria, Germany, the Netherlands and Sweden pay only one-quarter of their normal share in the UK rebate. In 2014-2018, a GNI-based distribution of the UK rebate would have implied a 0.044% of GNI extra contribution from the remaining 27 member states. But these four countries pay only 0.011% of their GNI for the UK rebate and thereby the remaining 23 member states pay 0.065% of their GNI to compensate for the lower payments of the four countries.

Reduced call rate for the value added tax (VAT) based contributions: In the 2007-2013 MFF, Austria, Germany, the Netherlands and Sweden benefited from temporary corrections in the form of reduced call rates for the VAT-based resource ranging between 0.1% and 0.225%, instead of the standard 0.3% rate applied to all other Member States. For the 2014-2020 MFF, Austria lost its privileged status and only Germany, the Netherlands and Sweden benefit from a 0.15% call rate, half of the call rate on the other 25 countries, which remained 0.3%. There is “capping”: VAT base to which the call rate is applied cannot exceed 50% of the GNI of the member state. And before capping and applying the call rate, the VAT base is harmonised across EU member states, which is “based on a complex methodology”, involving “unwieldy computations” and calculations that are “cumbersome and generate onerous administrative work”, as argued by a Commission staff working document.

Lump-sum reductions to GNI-based contributions: In the 2007-2013 MFF, annual reductions were granted to the Netherlands (€605 million a year in constant 2004 prices) and Sweden (€150 million a year in constant 2004 prices) to their GNI-based contributions. In 2014-2020, measured in 2011 prices, Denmark pays €130 million less a year, the Netherlands pays €695 million less a year and Sweden pays 185 million less a year. Austria also benefitted from reduced GNI-based contributions in 2014 (€30 million), in 2015 (€20 million) and in 2016 (€10 million) – perhaps to sweeten a bit its drop-out from the VAT-based reductions.

Correction related to security and citizenship opt-outs: Denmark, Ireland and the United Kingdom are exempt from financing specific parts of security and citizenship policies, for which they have an opt-out in the Amsterdam Treaty, with the exception of the related administrative costs. On average over 2014-2018, Denmark received €10 million annually, Ireland €6 million and the UK €75 million.

Unlike the UK rebate, the other corrections are financed by all member states, including those benefiting from the reductions, based on their share in EU GNI.

I also note (but do not analyse in this blog post) that there is a so-called ‘hidden rebate’ related to customs duties. The EU is a customs union with a common foreign trade policy, so it is sensible that customs duty revenues go to the EU budget. Yet member states retain 20 percent of customs duty revenues as ‘collection costs’, which is excessively high and benefits those countries that have well-located seaports, like Belgium and the Netherlands.

This is so ad hoc and non-transparent

Perhaps the first reaction that anyone can have after reading this list is that these corrections are so ad hoc. As recalled by Alessandro D'Alfonso, the European Court of Auditors have long highlighted that these correction mechanisms do not just compromise the simplicity and transparency of the financing system of the EU budget, but have various shortcomings (see here, here and here). These include:

- the absence of defined criteria to assess objectively whether a budgetary burden is excessive and when a Member State qualifies for a correction;

- the lack of a monitoring mechanism to establish whether a Member State benefiting from a correction still qualifies for it,

- the lack of a monitoring mechanism to establish whether other Member States that do not receive a correction now qualify.

Quantifying the rebates

In a paper on the net contributions to the EU budget that we will publish in a few days, I calculate the total impact of these corrections in the actually executed budgets of 2014-2018. Figure 1 shows the results both in euros and as a share of national GNI.

In terms of euros, France pays the most, €2.08 billion a year, for all these corrections, followed by Italy (€1.54 billion) and Spain (€1.02 billion). The main beneficiary is the UK with €5.08 billion a year, followed by the Netherlands (€0.92 billion), Germany (€0.75 billion) and Sweden (€0.32 billion). As a share of GNI, 22 EU countries contribute by close to 0.09% of their GNI to these corrections, to benefit the UK (0.22% of GNI), Netherlands (0.13% of GNI), Sweden (0.07% of GNI), and Germany (0.02% of GNI). Austria and Denmark are net contributors to the adjustments with about 0.035% of GNI, since these countries benefit from only some of the corrections.

Regressivity contradicts the Fontainebleau principle

These corrections also make national contributions (the sum of VAT-based and GNI-based contributions adjusted by the rebates) to the EU budget regressive, as pointed out by the Monti report on the future financing of the EU. That is, richer member states benefitting from rebates contribute less to the EU budget as a share of GNI than poorer member states.

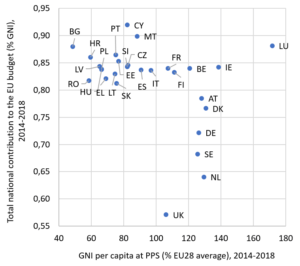

Figure 2 shows that most EU countries contribute about 0.85% of the GNI to the EU budget in the form of national contributions, but the six countries benefitting from sizeable rebates contribute significantly less – and these countries belong to the more affluent nations in Europe, also having relatively low public debts. Do Austria, Denmark, Germany, the Netherlands, Sweden and the UK suffer from an excessive budgetary burden in relation to their relative prosperity as established by the Fontainebleau principle? Well, if I was asked which EU country suffers from an excessive budgetary burden in relation to its relative prosperity, I would probably say Greece or Italy, not the six countries benefiting from sizeable rebates.

Figure 2: GNI per capita vs national contributions to the EU budget, 2014-2018

The real purpose is the reduction of net contributions

Countries benefiting from rebates are also the largest net contributors to the EU budget. Figure 3 shows the ‘operating budgetary balance’ (OBB), which is calculated by the Commission for the implemented annual EU budgets (see the definition of OBB on pages 72-73 of the EU budget financial report). Figure 3 shows the actual net contributions in 2014-2018 and my hypothetical calculations for net contributions in the absence of rebates, for all EU countries which were net contributors in 2014-2018.

In principle, the EU budget should provide truly European public goods that benefit every European country, in which case there would not be a rationale for rebates. But in practice, this is not the case. In particular, there are serious concerns with the European value added of the EU’s largest spending item, Common Agricultural Policy (CAP), from which e.g. France benefits a lot (see our discussion with Guntram Wolff here). The second largest EU spending item, cohesion policy, has a pan-European rationale, but it needs to be made more efficient and more efforts are needed to fight its improper use (see our work with Catarina Midões and Jan Mazza here).

If the largest net contributor member states believe that a big share of the EU budget is redistributed to countries for spending which do not constitute European public goods, or there are risks for their proper use, the attempt of reducing net contributions is understandable. But if that’s the case, it has to be acknowledged. And there has to be a transparent algorithm for calculating corrections since the current ad hoc system leads to some anomalies. For example, why does Sweden get more reductions than Germany (as a share of GNI) when both countries would have the same net contribution in the absence of reductions? Or why does the Netherlands get so much more reductions than Germany and Sweden (as a share of GNI), which lead to an even lower correction-adjusted net contribution for the Netherlands than for Germany and Sweden?

Clearly, the best solution would be to reform EU budget spending to provide only European public goods, in which case all rebates should be fully eliminated. But if such a reform of EU spending is politically impossible, then at least the rationale for the rebates should be spelt out clearly and a transparent correction system built on clear principles should replace the current ad hoc, non-transparent, complicated and regressive system of rebates.

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

The EU needs a methodology for including reform impacts in fiscal trajectories

Such a methodology, and a governance mechanism for managing associated risks, must be in place before the new fiscal framework kickstarts in September

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

Broader border taxes: a new option for European Union budget resources

The purpose of this paper is to review the Commission’s proposal and to contribute new ideas for ‘genuine’ own resources