The socio-economic consequences of COVID-19 in the Middle East and North Africa

Confronted with COVID-19, high-income Gulf countries have done better than most of their middle- and low-income neighbours; Jordan and Morocco are als

The COVID-19 pandemic has hit already stagnant and macroeconomically fragile economies in the Middle East and North Africa (MENA) through lockdown measures, interrupted supply chains, dramatic declines in tourism revenues and labour remittances, and temporarily low oil prices. In this article, we build on a January 2021 Bruegel Policy Contribution to analyse the scale of the health crisis and its various socio-economic consequences for MENA (see Table 1 for the countries we include), using information and data available at the beginning of May 2021.

COVID-19 in the MENA region

Iran was one of the early victims of the pandemic, with a first wave of fatal cases as early as March 2020. With few exceptions, MENA countries experienced three waves of the pandemic, similarly to Europe. However, a comparative cross-country analysis of infection intensity is difficult due to inadequate diagnostic and reporting systems in some countries.

The relative frequency of testing may provide an indirect measure of the effectiveness of the diagnostic system. The United Arab Emirates (UAE) and Bahrain have been regional leaders, and their testing figures have exceeded those of several advanced economies (Table 1). At the other end of the regional spectrum, the number of tests per million people in Mauritania, Egypt, Algeria, Sudan, and war-affected Syria and Yemen has been low.

Table 1: MENA, COVID-19 basic statistical numbers (as of 10 May 2021)

Source: https://www.worldometers.info/coronavirus/.

Despite data gaps, Table 1 suggests that, on average, there were fewer cases and deaths per million people in MENA than in the United States and most European and Latin American countries. Lebanon, Tunisia, Jordan, Iran, and Palestine recorded the highest numbers of deaths per million inhabitants.

Social and economic support measures

During the pandemic, the percentage of the population in MENA countries receiving social assistance has risen significantly, from around 20% to over 70%. However, the region has also recorded the lowest rise in benefit adequacy. This can be primarily explained by the predominance of untargeted support, mainly subsidies, in many countries throughout the region.

Almost all countries have adopted some form of recovery plan. The International Monetary Fund provides a detailed database of national fiscal responses. In some of the more affluent MENA countries, fiscal support was comparable to advanced economies. As early as March 2020, Qatar announced a package of measures worth around 14% of its GDP. It focused mainly on small and medium-sized enterprises and the sectors most affected by the pandemic (eg tourism, hospitality). Bahrain also introduced a large package, totalling around 6% of GDP in March 2020 which was then further expanded. Most central banks in the region also played a role through monetary expansion.

Some middle- and low-income economies also provided substantial support to their populations and businesses: the package announced at the outset of the pandemic in Iran amounted to 10% of its GDP. Other countries have been more fiscally constrained, able to implement only smaller programmes. Public bodies in several countries established funds to collect donations to finance anti-crisis measures (eg Iraq, Jordan, and Lebanon). International support has been essential in some of the poorer economies in the region (see below on the rollout of new IMF programmes).

These fiscal packages have generally combined measures of immediate budgetary impact, with delayed payments and guarantee funds. The range of measures employed has been varied, although primarily focused on combating the health emergency, fighting unemployment, supporting the most vulnerable and helping businesses survive, especially in hard-hit sectors (such as tourism). In Jordan, a plan to reinstate one year of military service is underway to combat youth unemployment.

Commodity markets and financial shock

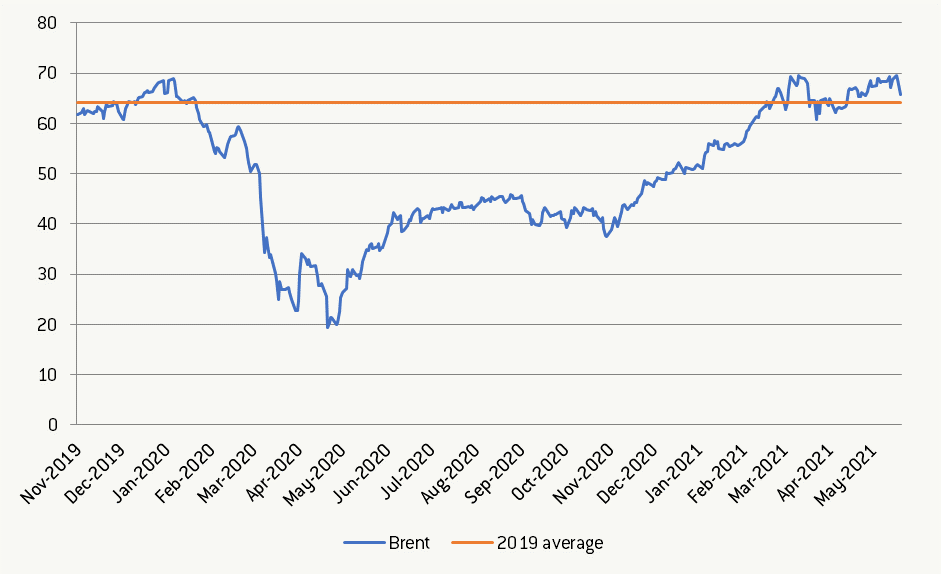

The pandemic-related economic shock in MENA was magnified by the collapse of commodity markets and capital flight from emerging markets. Oil producers were particularly heavily hit by the sudden oil-price fall in March 2020 (Figure 1), driven both by the decrease in global demand and the breakdown of coordination between suppliers within the OPEC+ agreement (in particular, between Russia and Saudi Arabia).

Figure 1: Monthly crude oil prices, $ per barrel, November 2020 – May 2021

Source: Bloomberg.

This coordination was partially reinstated in April 2020, stabilising prices at a level of around $40 per barrel between June and November 2020. Since November 2020, due to partial economic recovery worldwide, oil prices have grown again, achieving their pre-pandemic level (above $60 per barrel) in March 2021.

At the end of February and in early March 2020, the MENA region was hit by capital flight: the IMF estimated portfolio capital outflows of about $6 billion to $8 billion during the early days, numbers that they conceded might be even larger. However, the magnitude of this shock was smaller than in other emerging markets, especially in Latin America and the countries that made up the former Soviet Union. This may be explained by less financial openness in most MENA countries than elsewhere.

After the initial outflow, inflows in the second half of 2020 were $4 billion. By February 2021, cumulative flows since the beginning of the COVID-19 pandemic were positive, although this was reversed with the increase in US longer-term yields in March and April 2021.

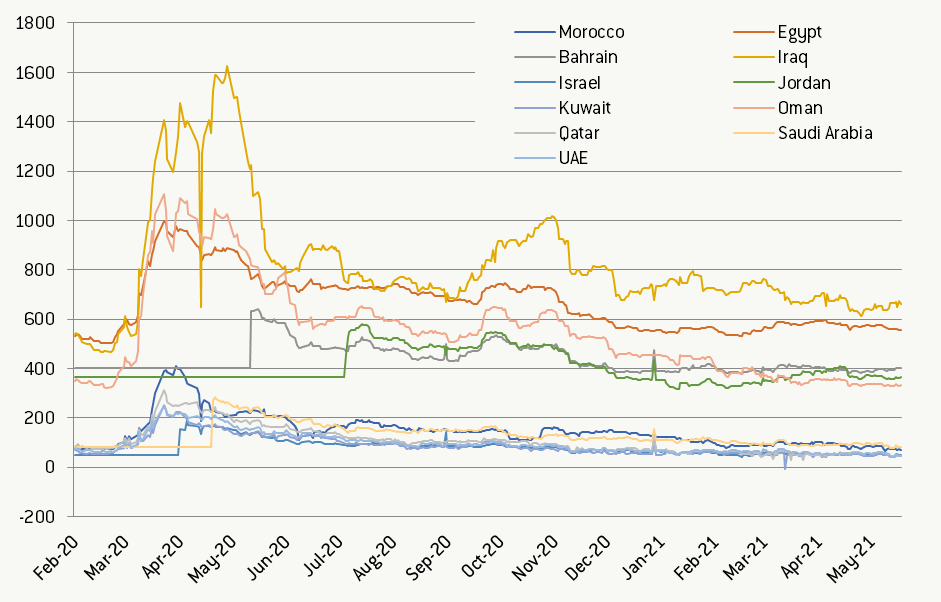

Figure 2 shows the spreads between the dollar-denominated debt and US Treasuries (UST) in selected MENA countries. While spreads widened significantly in the first days of the crisis, market confidence has recovered in most cases, with spreads nearing their pre-COVID-19 levels. This improvement in market sentiment is partly explained by the significant monetary and fiscal policy response in advanced economies, which has loosened global financing conditions. Countries with high credit ratings (oil producers) and lower credit-rated countries such as Egypt have managed to maintain market access, both with dollar-denominated and local-currency bonds. The one obvious exception is Lebanon (excluded from Figure 2 to avoid excessive skew), where the unsustainable sovereign debt situation accumulated over many years leading to default in March 2020. Restructuring has been stalled by a lack of political stability and general economic deterioration.

Figure 2: Spreads between sovereign dollar-denominated debt and UST, basis points, February 2020 – May 2021

Source: Bloomberg. Note: Lebanon excluded as its values were off the scale, between 2500 and 7000 basis points for the analysed period.

Depreciation of MENA currencies has been modest, and they have largely recovered (sometimes even with a positive margin) after an initial fall in March and April 2020. It is worth keeping in mind that most MENA currencies are pegged to the dollar and not all MENA currencies are fully convertible. While data on the changes in international reserves comes with an inevitable delay, reserve levels in the region are generally considered comfortable; these act as a protective buffer against uncertainty and fluctuations in US yields. The recovery of the oil price will also increase the reserves of oil exporters.

IMF assistance

To help address COVID-19-related economic and social consequences, the IMF provided emergency assistance to several MENA countries. Egypt, Jordan, and Tunisia received emergency assistance under the Rapid Financing Instrument. Djibouti and Mauritania have benefited from the Rapid Credit Facility, which includes concessional servicing terms. Because neither of these instruments includes policy conditionality, it is unlikely assistance will trigger structural reforms like the ‘standard’ IMF assistance programmes. Morocco has drawn from its precautionary credit line, the IMF Extended Fund Facility in Jordan has been modified, Mauritania augmented its Extended Credit Facility, and a new Stand-By Arrangement with Egypt was approved.

Region-wide recession

Like in other parts of the world, the economic impact of the COVID-19 in the MENA region has been severe. Only Egypt and Iran recorded positive growth in 2020, other countries suffered from recession (Table 2). On average, net hydrocarbon exporters and importers were affected equally. It is also worth remembering that the 2020 recession followed mediocre growth performance in the second half of the 2010s.

Table 2: MENA: GDP, constant prices, % change, 2019-2021

Source: IMF World Economic Outlook database, April 2021. Notes: red text indicates IMF staff estimates and forecasts; data for Syria is not available.

There are two outliers in Table 2 – Libya and Lebanon. In Libya, profound fluctuations in GDP have resulted from domestic conflict, leading to periodic interruptions in oil production and exports. Lebanon, as mentioned above, has seen a full-blown sovereign debt crisis. Worse, internal political strife has prevented the formation of a stable government to prepare a rescue programme and start negotiations with the IMF.

Trade data confirms the recessional impact of the pandemic (Table 3). In 2020, most MENA countries recorded deep contractions of both imports and exports. Among a few exceptions, Iran's oil exports increased in the second half of 2020, probably by circumventing the United States' oil embargo, explaining the increase in real GDP (Table 2).

Table 3: MENA: Changes in volume of imports and exports of goods and services in 2020 as compared to 2019, %

Source: IMF World Economic Outlook database, April 2021. Notes: red text indicates IMF staff estimates and forecasts; data for Iraq and Syria is not available.

Deepening of fiscal and macroeconomic imbalances

The deep recession, lower general government (GG) revenues, and higher expenditures further deteriorated fiscal balances and debt-to-GDP levels in most MENA economies (Table 4; Figures 3 and 4).

Apart from Egypt, Lebanon, Mauritania and Sudan, GG balances in MENA countries deteriorated in 2020 compared to 2019. In some cases, such as the Gulf countries (except Qatar), Iraq, Libya and Tunisia, this deterioration was substantial. Large fiscal deficits and GDP declines resulted in dramatic increases in gross and net GG-debt-to-GDP ratios (Figures 3 and 4).

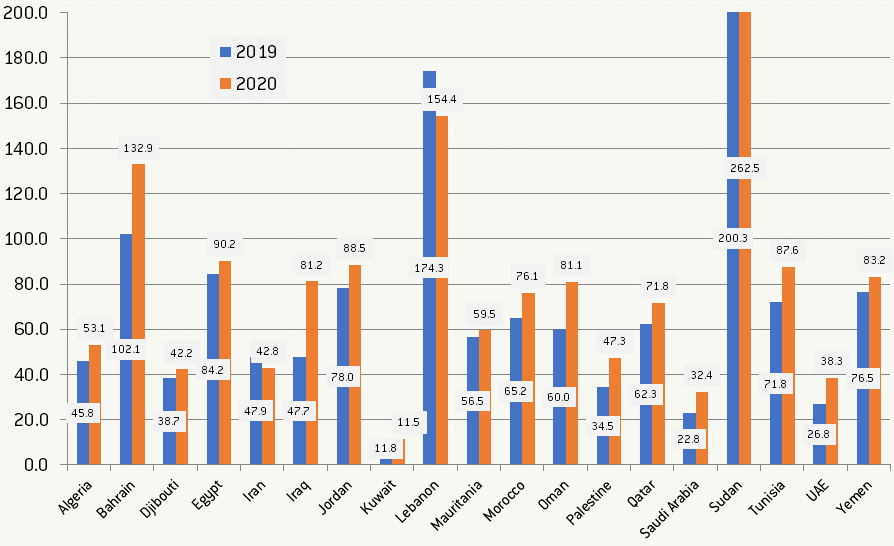

Except for Iran and Lebanon, gross GG debt increased everywhere, often by more than ten percentage points of GDP (Figure 3). In oil-producing Sudan, it reached 262.5% of GDP, in Bahrain 132.9%. In Lebanon, which defaulted in March 2020, it remains at 154.4% of GDP. In Egypt, Iraq, Jordan, Oman, Qatar, Tunisia and Yemen, it exceeds 80% of GDP. We cannot exclude the possibility of new sovereign defaults in the MENA region in the coming years.

Table 4: MENA; GG revenue, expenditure and balance (net lending/borrowing), % of GDP, 2020-2021

Source: IMF World Economic Outlook database, April 2021. Notes: red text indicates IMF staff estimates and forecasts; data for Syria is not available.

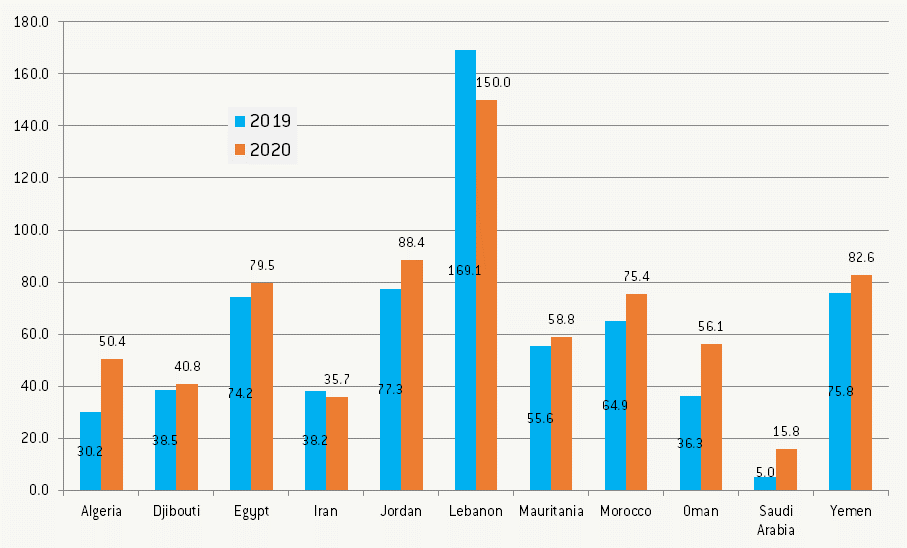

The net debt figures (gross debt minus financial assets correspondent to debt instruments) are only available for some MENA countries. In 2020, net debt also increased in all reported economies except Iran and Lebanon (Figure 4). Only in Oman and Saudi Arabia is the difference between gross and net debt meaningful but decreasing over time, which suggests gradual depleting of their sovereign wealth funds. The lack of net-debt data for other Gulf states means we cannot assess the size of their sovereign assets and their potential depletion.

Current account balances in MENA also deteriorated in 2020. In some countries – Djibouti, Iraq, Kuwait and Libya – this deterioration exceeded ten percentage points of GDP. On the other hand, Egypt, Morocco, Tunisia and Yemen managed to improve their current account balances marginally due to a more significant declines in imports than exports. Only Lebanon recorded a higher improvement of its very high current account deficit (from -26.5% of GDP in 2019 to -14.3% of GDP) at the costs of deep recession (Table 2) and a drastic decline in domestic demand.

Regarding inflation, there was no single trend in the region in 2020. It jumped to very high and high levels in Sudan (269.3%), Lebanon (150.4%), Iran (48.0%), Yemen (45.0%) and Libya (22.3%). However, it was negative in Qatar (-3.4%), the UAE (-2.1%), Bahrain (-1.6%), Morocco and Oman (both -0.9%), and Jordan (-0.3%), that is, in the countries which have their currencies pegged to the dollar. In other cases, inflation remained on a low one-digit level.

Figure 3: MENA: GG gross debt, % of GDP, 2020-2021

Source: IMF World Economic Outlook database, April 2021. Note: data for Libya and Syria is not available.

Figure 4: MENA: GG net debt, % of GDP, 2020-2021

Source: IMF World Economic Outlook database, April 2021.

Uncertain prospects

The April 2021 IMF World Economic Outlook predicts a modest recovery in the region in 2021 (last column of Table 2). Still, all forecasts are subject to frequent corrections and updates, compounded by pandemic-related uncertainty.

The pace of global economic recovery will impact international hydrocarbon prices which are crucial for MENA oil and natural gas exporters. On the regional level, fighting the pandemic (mainly by vaccination) will be the most critical factor determining the speed of opening up of individual economies and the most vulnerable sectors such as tourism. In the longer term, economic recovery will depend on the resolution of regional conflicts, the political ability to reduce fiscal deficits and public debt, a continuation of structural, institutional, and social reforms, and finding a constructive response to the increasing democratic aspirations of MENA societies.

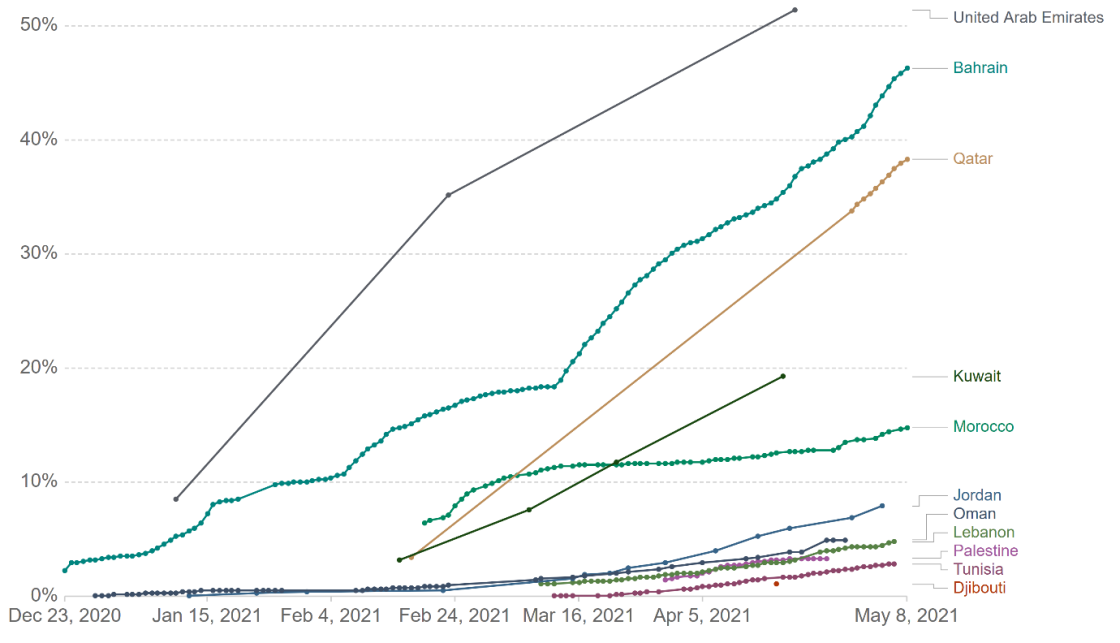

Figure 5 shows the progress of COVID-19 vaccination in the MENA region. The UAE, Bahrain, Qatar and Kuwait lead in the region, with Morocco not too far behind.

Figure 5: MENA: Share of people who received at least one dose of COVID-19 vaccine (up to 8 May 2021)

Source: https://ourworldindata.org/covid-vaccinations. Note: countries with no data and with the share of vaccinated population below 1% are omitted.

While vaccines administered in the MENA region come from various suppliers, Chinese producers play the dominant role. Overall, the region struggles with limited access to vaccines, especially those produced in the US and Europe (BioNTech/Pfizer, Moderna and Astra Zeneca). Some countries, especially those affected by violent conflicts and political disintegration, lack the administrative and logistical capacity to conduct mass vaccination.

Different responses across the region

Overall, our analysis suggests intra-regional differences in response to the COVID-19 pandemic. To a large degree, these reflect differences in the GDP per capita levels of individual countries and the quality and resources of health systems and public administrations. High-income Gulf countries have been doing much better than most of their middle- and low-income neighbours, although there have been some positive exceptions among the latter, for example, Jordan and Morocco.

Acknowledgement

The authors would like to thank Uri Dadush for his valuable comments on a draft of this blog post.

Recommended citation:

Dabrowski, M. and M. Domínguez-Jiménez (2021) ‘The socio-economic consequences of COVID-19 in the Middle East and North Africa’, Bruegel Blog, 14 June

About the authors

Related content

Income inequality hardly changed during the COVID-19 pandemic

Contrary to expectations, there was no widespread increase in either within-country or global income inequality during the pandemic

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

Asia 2024 Outlook

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.