No contagion from Cyprus so far

The Cyprus drama has not destabilised the rest of the eruo area so far, despite the talks about a possible ‘Cyprexit’, i.e. an exit of Cyprus form the

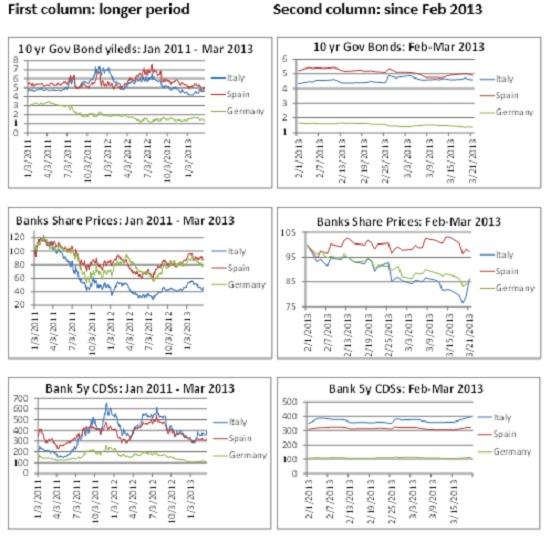

The Cyprus drama has not destabilised the rest of the euro area so far, despite the talks about a possible ‘Cyprexit’, i.e. an exit of Cyprus form the euro area. While government bond yields have increased significantly in Cyprus, they hardly changed in e.g. Italy and Spain: the slight increase earlier this week was less than after the February Italian elections, and in the past two days yields have even declined. Bank shares in Italy and Spain (and also in Germany) fell and the credit default swap (CDS) spreads of banks have increased somewhat, but nothing extraordinary. See the charts at the end of this post.

Why is the market so calm? There are two possible explanations. First, markets may expect that there will be a deal for Cyprus and therefore the country won’t exit the euro area. Indeed there is a very strong case for Cyprus giving in i.e., the parliament should agree taxing deposits above €100,000, as we argued here. Second, even if Cyprus exits the euro area, it is so small and so special (banking system amounting to more 7-times GDP; about 50% of GDP capital shortfall for banks; suspected money-laundering; tax haven and high bank deposit rates) that it won’t have a systemic effect on the rest of the euro area.

Notes: The following banks were included for calculating average bank data:

CDS

ITALY : Intesa Sanpaolo SpA, Banca Monte dei Paschi di Siena SpA, UniCredit SpA, Unione di Banche Italiane SCPA, Banco Popolare SC.

SPAIN : Banco Santander SA, Banco Bilbao Vizcaya Argentaria SA, Banco Popular Espanol SA, CaixaBank, Caja de Ahorros y Monte de Piedad de Madrid.

GERMANY: Deutsche Bank AG, Commerzbank AG, Bayerische Landesbank, Norddeutsche Landesbank, HypoVereinsbank.

SHARE PRICES:

ITALY : Intesa Sanpaolo SpA, Banca Monte dei Paschi di Siena SpA, UniCredit SpA, Unione di Banche Italiane SCPA, Banco Popolare SC.

SPAIN : Banco Santander SA, Banco Bilbao Vizcaya Argentaria SA, Banco Popular Espanol SA.

GERMANY: Deutsche Bank AG, Commerzbank AG.

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

The EU needs a methodology for including reform impacts in fiscal trajectories

Such a methodology, and a governance mechanism for managing associated risks, must be in place before the new fiscal framework kickstarts in September

Real effective exchange rates for 178 countries: a new database

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries