ICT for growth: A targeted approach

The digital Agenda for Europe is a prime example of an initiative to promote EU growth. One of the Europe 2020 strategy’s seven flagship initiatives, it focuses on information and communication technologies (ICTs) as a spur for sustainable and inclusive growth. Several obstacles that keep European businesses and organisations from making greater use of ICT identified, we aim to critically assess these obstacles, and identifying in broad terms the policies that can unlock the highest value for Europe. Four broad technology categories within ICT are identified and their potential economic impact in Europe can be estimated: i) social networks/Web 2.0, ii) cloud computing, iii) machine-to-machine (M2M) communication, and iv) data-driven organisational technology.

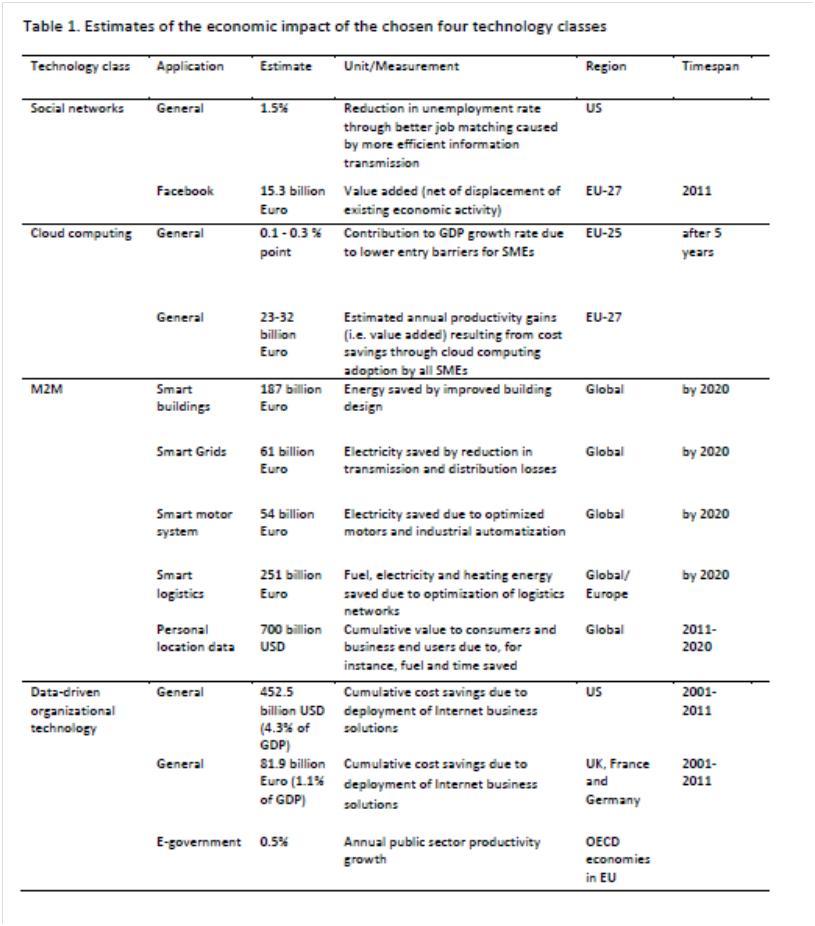

These technology categories combined can be broadly classified as general purpose technologies (GPTs), which have a nontrivial economic impact, but allow analysing the mechanisms leading to productivity improvements. According to Bresnahan and Trajtenberg (1995), who coined the term, GPTs are enabling technologies that provide a platform for subsequent applications, rather than being in themselves complete solutions. A GPT is a technology that exhibits the following features: i) scope for improvement, ii) a range of uses in different sectors, iii) a significant range of uses in most of these sectors, and iv) complementarities with existing and potential new technologies. The total impact of a GPT in any given point in time is much greater than the direct productivity impact of its individual applications. The impact tends to grow substantially over time, eventually reshaping large parts of the whole economy as past examples like electricity, mass production and semiconductors have shown. Clearly, from the perspective of the whole economy, new technologies displace some existing economic activity, the macroeconomic measures that we report, such as the unemployment rate or GDP growth, take the displacement effect into account. This post aims to summarize the most relevant estimates from academic literature and practitioners’ reports of the economic impact of the four technology categories mentioned. Table 1 gives an overview of these estimates and the following sections describe the mechanisms behind and the obstacles facing.

SOCIAL NETWORKS

Social networks on the internet, known also as Web 2.0, can be defined as virtual user communities, the members of which interact, share content and collaborate online. The crucial feature of Web 2.0 is user-generated content as for example Facebook and Wikipedia. By allowing people to create and share knowledge, social networks create economic value in a variety of ways. Most of this value is very difficult to quantify, because it is realised by dispersed communities of often anonymous users, who do not pay any monetary price for it, as exemplified by Wikipedia. The created value by Facebook amounts to €15 billion in Europe in 2011 mainly caused by advertising, gaming applications and additional sales of devices and broadband capacity.

Due to the influence of social networks, a more efficient process of matching employers and employees potentially reduces US unemployment rate from 6.5 percent to 5 percent. Extrapolated, such a drop in unemployment could bring additional GDP growth of 0.13 percent, or €16 billion, to Europe. It seems that there are no obstacles to their future growth and productive use, but the lack of wellfunctioning privacy laws could lead to reluctance to share private information with a large network of online friends, thereby undermining the long run viability of social networks as job-search facilitators.

CLOUD COMPUTING

Cloud computing provides online storage and computing capacity as a service on a pay-perusage basis, particularly attractive for small and medium enterprises (SMEs) avoiding large up-front investment costs. $1.3 billion of venture capital investment in US cloud companies show the potential of cloud computing even in an early stage. Etro (2009) estimates that it could boost European GDP growth by up to 0.3 percent by 2014 due to lower entry barriers for SMEs. Cloud computing can also generate substantial savings on IT infrastructure maintenance for existing companies in virtually all sectors. The value of these savings could be up to €32 billion annually, if all European SMEs adopt cloud computing. More sophisticated applications require faster broadband connections such that investment in fiber optic next-generation networks (NGNs) is, instrumental. The other big obstacles for cloud computing deployment are intellectual property (IP), data security and liability issues. The storage of data in the cloud raises new questions about who actually owns the data and what rights are attached to it.

MACHINE-TO-MACHINE COMMUNICATION

The OECD describes machine-to-machine communication (M2M) as “devices that are connected to the internet using a variety of fixed and wireless networks and communicate with each other and the wider world”. Applications include smart grids, smart metering and smart cities for example. Common to all M2M applications is the collection of data through various sensors and transmission of this data through the internet to a center that automatically processes and responds to the data.

A considerable value could be generated by this category of technologies of some €50 billion of annual energy savings in the EU by 2020. The combined value for Europe of the remaining smart technologies shown in Table 1 – smart motor systems and smart logistics – is estimated by us at €40 billion by 2020. The value generated by automotive M2M technologies and mobile phone location-based services would increase this to $700 billion. Privacy and security is, however, a big concern for personallocation data services. Finally, cellular networks are perceived to be well suited for realising M2M communication, but may soon become a bottleneck for M2M growth.

In general, M2M poses new challenges to wireless spectrum allocation policy, because it may lead to the use of spectrum not foreseen by regulators and further congest the unlicensed frequency bands (OECD, 2012).

DATA-DRIVEN ORGANISATIONAL TECHNOLOGY

We use the term data-driven organizational technology to describe “innovative management techniques, business models, work processes, and human resource practices, which complement and amplify their [i.e. firms’] ICT investment” (Brynjolfsson, 2011). Organisational technologies are usually not considered as GPTs, but there are many examples of organisational technologies that clearly fulfil the GPT criteria including factory systems, mass production and flexible manufacturing.

How does data-driven organisational technology change companies and make them more innovative? Essentially the large amount of data that modern firms collect and store in their ICT systems can enable a shift from intuitive management to more objective data-driven decision making. The fact that US companies have been much more successful in implementing this new organisational technology than EU companies can explain a significant part of the EU-US productivity gap. The productivity statistics suggest that the EU has been slower to invest in ICT, and that the productivity of EU ICT investment has also been lower (Ortega-Argiles, 2012). This raises the question of what the value is of the missed opportunity due to sluggish uptake of data-driven organisational technology in Europe. Assuming that European companies adopt data-driven organisational technology at the same pace as their US counterparts, Europe could achieve an additional 3.2 percent of GDP over a decade – roughly 0.3 percent extra growth each year in conservative estimates. Greater competition in the US markets compared to the European markets is a likely explanation of the observed ICT and ICT-related organisational technology investment gap. Rigid product and labour-market regulations and the lack of European single market, especially the digital market and the market for services, significantly hamper the deployment of data-driven organisational technology and ICT solutions, thereby slowing European growth and contributing to the US-EU productivity gap.

EU POLICY IMPLICATIONS

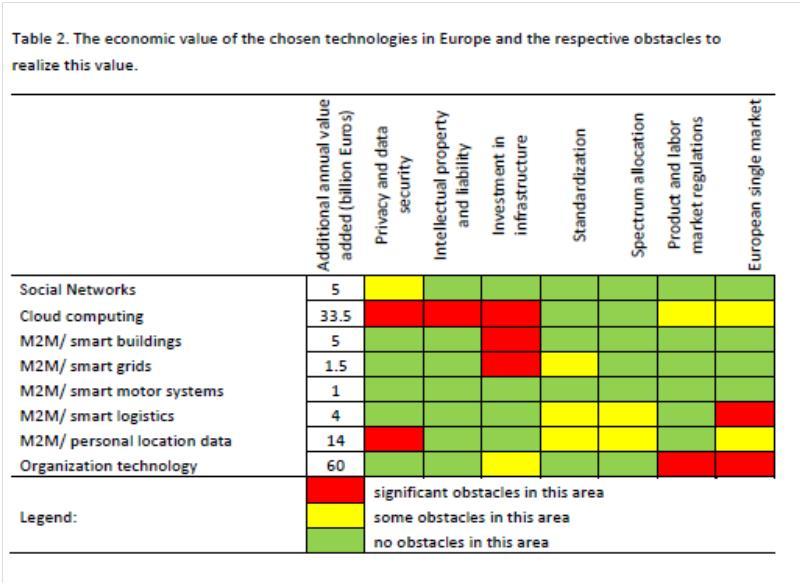

Table 2 puts together various areas of industrial policy that hold back the development of ICT technologies. A significant obstacle is shown in red, a minor obstacle in yellow and no obstacle in green. Assigning obstacles to the red category, means that a given policy area has been rated as a significant barrier in at least two independent studies. Overcoming the obstacles identified in Table 2 call for significant political effort, potentially unlock significant growth quickly, alongside public and private investment in ICT infrastructure, paying off only after a number of years. Table 2 suggests that it is the insufficiently complete European single market that is the greatest obstacle to ICT technologies, in terms of holding back the realisation in the EU of the greatest value (€64 billion annually), followed by restrictive product and labour-market regulations (€60 billion annually), privacy and data security concerns (€47.5 billion annually) and insufficient intellectual property and liability laws, jointly with next generation network (NGN) investment (€33.5 billion annually in each case).

In summary, the policies that can unlock the most growth from the use of ICT are in the areas of product and labour-market regulation and the European Single Market, issues with are subject to a common European strategy in order to allow a widespread adoption of modern data-driven organisational and management practices. Privacy, data security, intellectual property and liability pertaining to the digital economy, especially cloud computing, are also identified as areas for action. Investment in NGN infrastructure will bring further benefits by making the internet ecosystem viable in the long term, and needs to be spurred by proper incentives for the private sector. Very importantly, overcoming obstacles to growth in these critical areas requires political and regulatory effort rather than fiscal stimulus. The GPT character of the analysed ICT technologies suggests, however, that policymakers need to address all the obstacles identified here in order to fully achieve the potential of ICT to spur sustainable long-run growth that goes beyond the immediate gains that we estimate.

REFERENCES

Bresnahan, Timothy F. and M. Trajtenberg (1995) ‘General Purpose Technologies “Engines of Growth”?’ Journal of Econometrics, vol. 65(1): 83-108

Brynjolfsson, Erik (2011) ‘ICT, innovation and the e-economy’, EIB Papers, vol. 16(2): 60-76

Etro, Federico (2009) ‘The Economic Impact of Cloud Computing on Business Creation, Employment and Output in Europe. An application of the Endogenous Market Structures Approach to a GPT Innovation’, Review of Business and Economics, vol. 0(2): 179-208

OECD (2012) ‘Machine-to-machine communications: connecting billions of devices’, OECD Digital Economy Papers, no. 192

Ortega-Argiles, Raquel (2012) ‘The transatlantic productivity gap: a survey of the main causes’, Journal of Economic Surveys, 26(3): 359-419

About the authors

Related content

ICT for growth: a targeted approach

This policy contribution assesses the broad obstacles hampering ICT-led growth in Europe and identifies the main areas in which policy could unlock

Why is Europe lagging on next generation access networks?

Fibre-based next generation access (NGA) roll-out across the European Union is one of the goals of the European Commission’s Digital Agenda strategy,

The idea that Europe’s economic performance is inferior to that of the United States is erroneous

Talks@Bruegel: How the US weaponised the world economy with Abe Newman

How does recent research illuminate the US' influence on global surveillance and control, and what does this imply for international economies?