Has ECB QE lifted inflation?

Euro-area headline inflation has remained close to zero since the ECB stepped up its quantitative easing programmes in early 2015, but this does not m

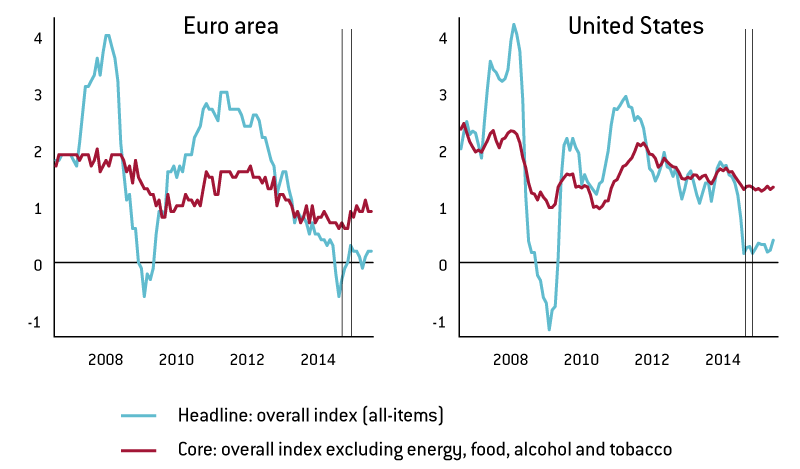

Despite efforts by the European Central Bank (ECB), recent euro-area inflation figures continue to be low, as shown in Figure 1. Headline inflation in the euro-area has remained close to zero since early 2015, when the ECB started its expanded asset purchase programme (EAPP), otherwise known as quantitative easing (QE).

Guntram Wolff has shown that market-based inflation expectations fell from July to September 2015 and remained well below the ECB’s 2% inflation benchmark. Inflation expectations have hardly changed since then.

Figure 1: Headline and core inflation, monthly data, 2007–2015 (% change compared to the same month of the previous year)

Sources: Euro-area: “All-items HICP” and “Overall index excluding energy, food, alcohol and tobacco” from Eurostat’s Harmonised Index of Consumer Prices [prc_hicp_manr] dataset; US: “Personal Consumption Expenditures: Chain-type Price Index” and “Personal Consumption Expenditures Excluding Food and Energy: (Chain-Type Price Index)” from FRED (Federal Reserve Economic Data), Federal Reserve Bank of St. Louis. For the US, we use the price index of personal consumption expenditures because this is the indicator considered by the Federal Reserve as reported by James Bullard. The first vertical line indicates January 2015 when the ECB announced its expanded asset purchase programme, while the second vertical line indicates March 2015 when the programme started.

Some observers may take these developments as evidence for the ineffectiveness of the ECB’s QE, but such a view would be wrong. In this post I show that euro area core inflation, a measure of inflation which disregards price changes for more volatile items like food and energy, as well as its adjusted versions for low energy prices have steadily increased throughout 2015, when we use quarterly data, which filters out short term noise.

Focusing on energy prices is rather obvious. Energy price developments do not really depend on ECB monetary policy measures. Low energy prices impact inflation, and not just because energy products accounts for more than 10 percent of the total consumer basket used to calculate inflation.

Energy has indirect and second round effects on inflation too, and so falling energy prices exert a downward pressure on core inflation. For example, the cost of transportation might fall, but more generally, lower energy prices reduce the costs of all producers, which may then reduce their sales prices in various sectors.

Yet the magnitude of this effect is not clear-cut. The ECB suggested in December 2014 that the fall in oil prices accounted for 0.6 percentage point of the total 0.9 percentage point decline in core inflation from late 2011 to mid-2014 (see Box 3 in the December 2014 Monthly Bulletin).

It is puzzling that oil prices play such a large role, especially when compared to the US: Dae Woong Kang, Nick Ligthart and Ashoka Mody showed that core inflation fell much more in the euro area than in the US, while low oil prices had an impact in both economies.

In order to assess the impact of oil prices on euro-area and US core inflation rates, I use a simple regression model: see the details in the annex. I use this model to calculate an adjusted version of core inflation. The indicator I call ‘core inflation adjusted for energy prices’. I aim to answer the question of what core inflation would be if inflation rate of energy goods was the same as core inflation.

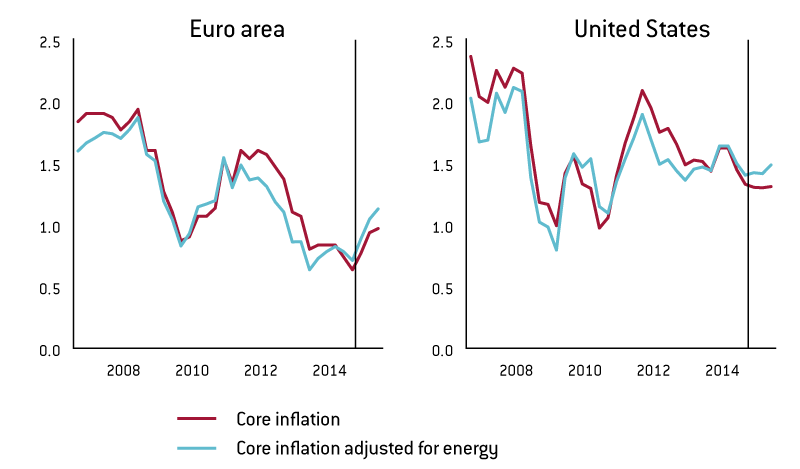

Both actual euro-area core inflation (red line) and the energy-adjusted core inflation (blue line) increased throughout 2015, as shown in Figure 2. Energy adjusted core inflation increased somewhat more than core inflation, suggesting that second-round effects of low oil prices matter, though the quantitative impact is not so large (my estimate for the contribution of oil prices to the fall in core inflation from late 2011 to mid-2014 is also well below the above mentioned ECB calculation).

For the US, I also find that energy-adjusted core inflation is higher than actual core inflation in 2015.

If my simple regression is able to capture the tendencies correctly, then euro area core inflation and its energy adjusted version have increased steadily since early 2015, at least using quarterly figures.

Current and energy-adjusted euro-area core inflation rates are still well below the ECB’s 2% threshold and are also below US core inflation, but my analysis shows that the very low euro area headline inflation rates cannot be used to argue for the ineffectiveness of ECB QE.

Figure 2: Core inflation and its adjusted version, quarterly data, 2007 – 2015 (% change compared to the same quarter of the previous year)

Source: core inflation is from Eurostat/St Luis FED, adjusted core inflation is my calculation (see Annex). The vertical line indicates the first quarter of 2015 when the ECB launched its expanded asset purchase programme.

Annex: the regression

I study the developments of the annual percent change in euro area core inflation defined by Eurostat as an “overall index excluding energy, food, alcohol and tobacco” that I call “core inflation”.

For the USA, I use the annual percent change in ‘Personal Consumption Expenditures Excluding Food and Energy: (Chain-Type Price Index)’.

My aim is to calculate a counterfactual indicator that I call “core inflation adjusted for energy prices”: what would core inflation be if energy goods inflation rate was the same as core inflation?

To this end, I convert the data from monthly to quarterly frequency (to reduce the short-term noise in the data) and estimate a Phillips-cure-type regression for core inflation:

where

is core inflation,

is the unemployment rate,

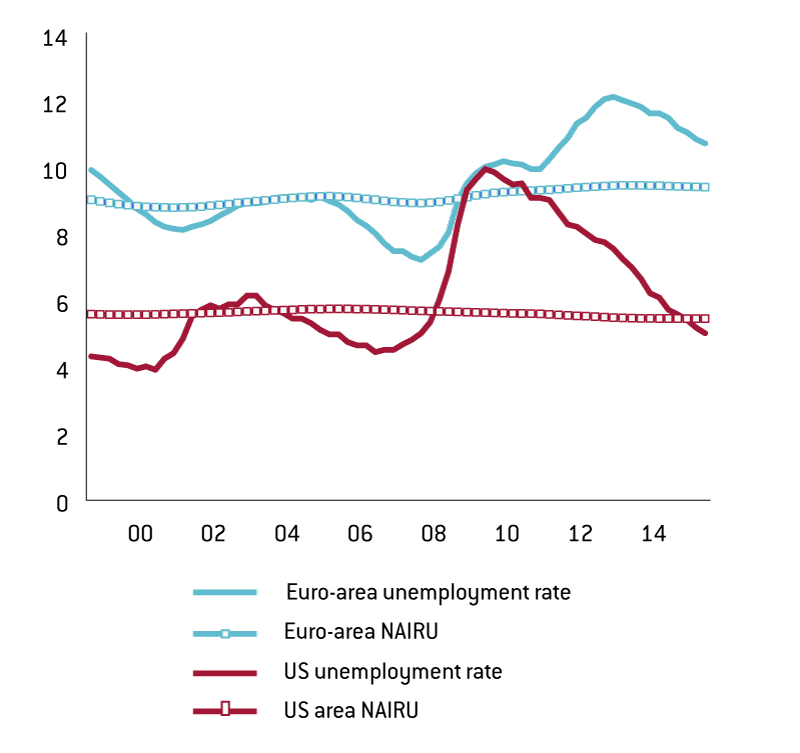

is the so-called non-accelerating inflation rate of unemployment (NAIRU, estimated by the OECD, see Figure 3),

is the inflation rate of energy goods in the consumer price index,

is the error term and

are parameters to be estimated. I allow lagged values up to four quarters (i.e. one year), because it can take time till unemployment and energy prince inflation can influence core inflation, while my general specification allows rich dynamic interactions between the variables.

I estimate this regression on quarterly data between 1999 and 2015. After estimating the regression, I calculate a counter-factual simulation for core inflation by setting the gap between energy and core inflation to zero throughout the sample period.

Starting from the 1999Q1 actual value of core inflation, I iterate the above equation using the estimated values of the parameters, the actual gap between the unemployment rate and NAIRU and the estimated error term (which captures all factors which are not included in the regression).

Certainly, one could use more sophisticated models, yet I believe this simple setup is able to provide useful results.

Figure 3: Unemployment rate and the NAIRU, quarterly data, 1999 – 2015 (%)

Sources: Unemployment rate: Eurostat’s Unemployment rate by sex and age [une_rt_m] database; NAIRU (non-accelerating inflation rate of unemployment): OECD’s Economic Outlook No 98 (November 2015), which is available at the annual frequency: I converted the annual NAIRU estimates to the quarterly frequency.

About the authors

Related content

The European Central Bank’s timid operational framework update

The European Central Bank announced limited changes to its operational framework – which is probably right given current uncertainty

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

The European Central Bank, inflation tolerance and the last mile

A tale of two treatises: the Werner and Delors Reports and the birth of the euro

Focusing on the Werner and Delors Reports, this essay aims to capture key ideas and debates, giving a chronological overview of the EMU process