Is Greece destined to grow?

There is much talk about the impasse between Greece and its official lenders in their bail-out negotiations, so I thought I would write about somethin

Greece’s pre-crisis growth model was clearly unsustainable. It was characterised by widespread state control, inefficient public administration, corruption, excessive increases in public sector employment and wages, large increases in private sector wages well over productivity growth, and insufficient structural reforms. This model led to very unfavourable business conditions, which was reflected in Greece being ranked 108th out of 181 countries in the World Bank’s Ease of doing business indicator in 2008. Major vulnerabilities emerged, such as the -16.5% GDP current account balance in 2008, the -74 % of GDP net international investment position and the huge budget deficit and public debt. In 2008, the budget deficit was 10 % of GDP, which increased to 15% in 2009, by far the largest values in the EU, despite that economic contraction in these two years was not particularly large in Greece (GDP growth was -0.4% in 2008 and -4.4% in 2009). Public debt climbed to 127 % of GDP in 2009 and was on an exploding path. Clearly, the Greek crisis which erupted from late 2009 onwards was self-inflicted.

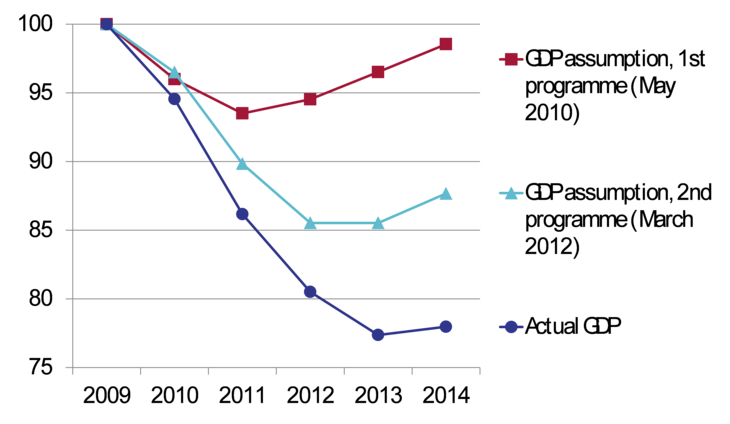

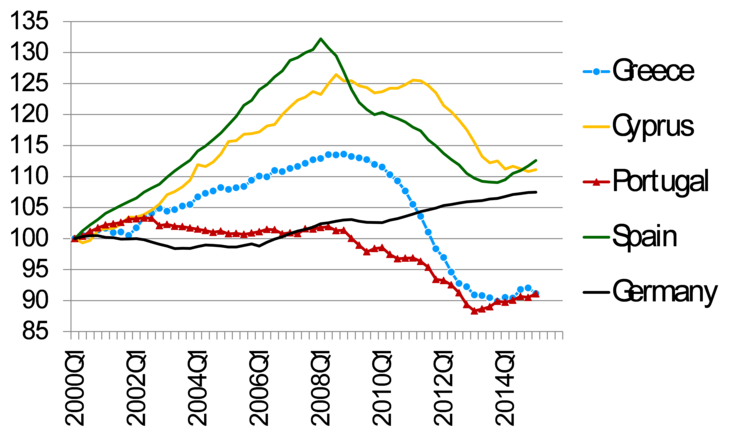

After 2010 the collapse of the Greek economy accelerated. GDP fell much more than was foreseen in the adjustment programmes (Figure 1). The big question is whether all of this collapse was inevitable given the unsustainable character of the pre-crisis growth model of Greece, or if the two Troika programmes exacerbated the output fall. In my assessment, some elements of the programmes worsened the situation (as I argued here), but instead of elaborating what went wrong, let me focus on the economic adjustments of the past five years, in comparison to Cyprus, Portugal, Spain and Germany.

Figure 1: GDP at constant prices (2009 = 100), 2009-2014

Source: Programme documents, AMECO database May 2015.

Greece has made significant progress, but there is still a long way to go.

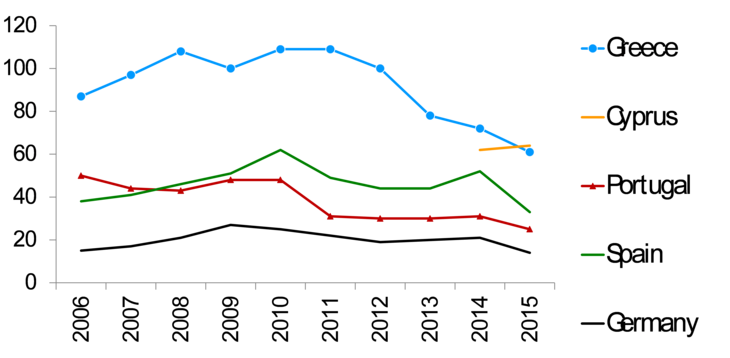

In some aspects Greece has improved a lot. In the ease of doing business indicator, Greece’s ranking has risen from 108th in the world in 2008, to 62nd in 2015 (Figure 2). Greece has made significant progress, but there is still a long way to go.

Figure 2: World Bank ease of doing business ranking, 2006-2015

Source: World Bank. Note: 1=most business-friendly regulations. Data from 153 countries in 2006, and 189 countries in 2015. Cypriot data was reclassified in 2014 and therefore we do not show earlier values.

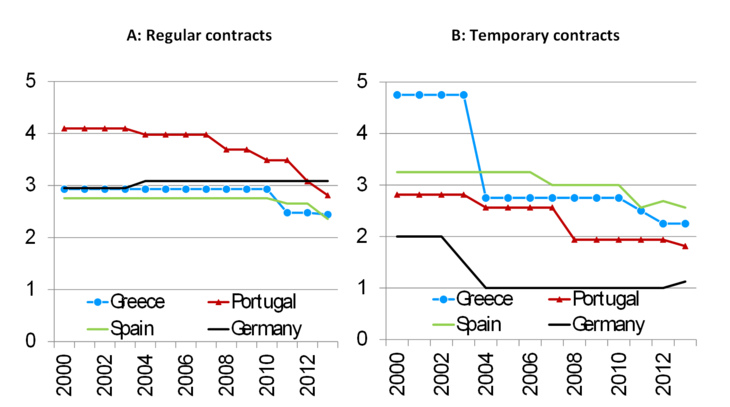

According to the OECD, labour markets are now more flexible in Greece than in Germany, concerning regular contracts (Panel A of Figure 3), which account for 73% of Greek employment. There has been some easing in the regulations for temporary labour contracts too (Panel B of Figure 3).

Figure 3: OECD index of strictness of employment protection, 2000-2013

Source: OECD. Note: for regular contracts, version 2 of the indicator is used, while for temporary contracts version 1 (in the absence of version 2). Version 3 is available for both indicators, but only for 2008-2013.

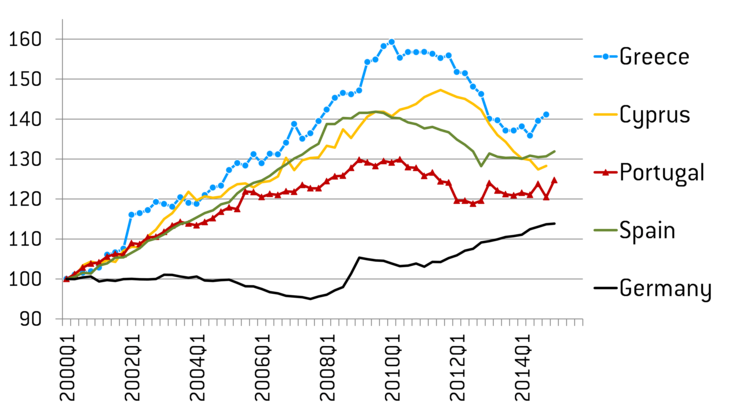

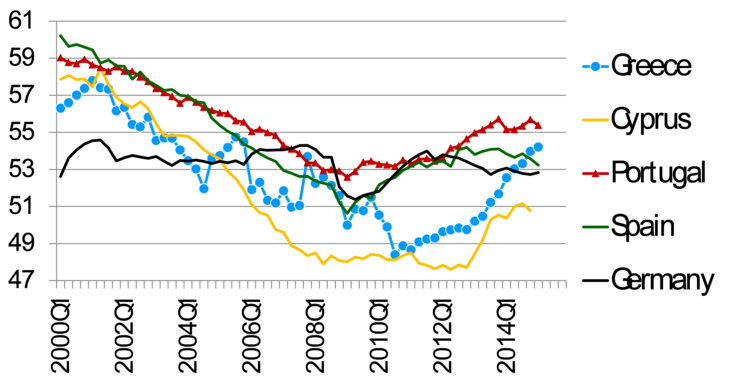

There has been a sizeable adjustment in unit labour costs (ULC) in Greece, though not all pre-crisis divergences have been corrected (Figure 4). Unit labour costs matter: as I indicated here, there is a quite close association between ULC-based real exchange rates and export performance. This was true especially before the crisis (when Greece fit very close to the regression line), though the association has become somewhat weaker in the post-2008 period, when Greece is an outlier: exports have not grown as much as the relationship would have predicted.

Figure 4: Unit labour cost developments (2000Q1=100), 2000Q1-2015Q1

Source: updated dataset by Darvas, Zsolt (2012b) 'Compositional effects on productivity, labour cost and export adjustment', Bruegel Policy Contribution 2012/11

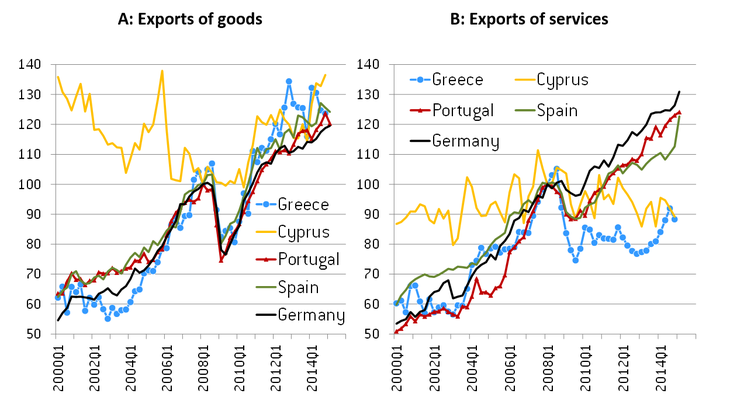

Figure 5 shows export developments separately for goods and services: at current prices, goods exports developed almost the same way as goods exports from Germany, Portugal and Spain (panel A of Figure 5) – in fact, Greece even did slightly better. This is very good news. The bad news is that Greek (and also Cypriot) services exports underperformed compared to Germany, Portugal and Spain (Panel B of Figure 5). The Bank of Greece (see page 65) concluded that weaknesses in exports of services were primarily related the prospect of Grexit, in particular the negative impact of uncertainty on tourism, and the decline in the international freight market on shipping.

Figure 5: Exports at current prices (2008Q1=100), 2008Q1-2015Q1

Source: Eurostat.

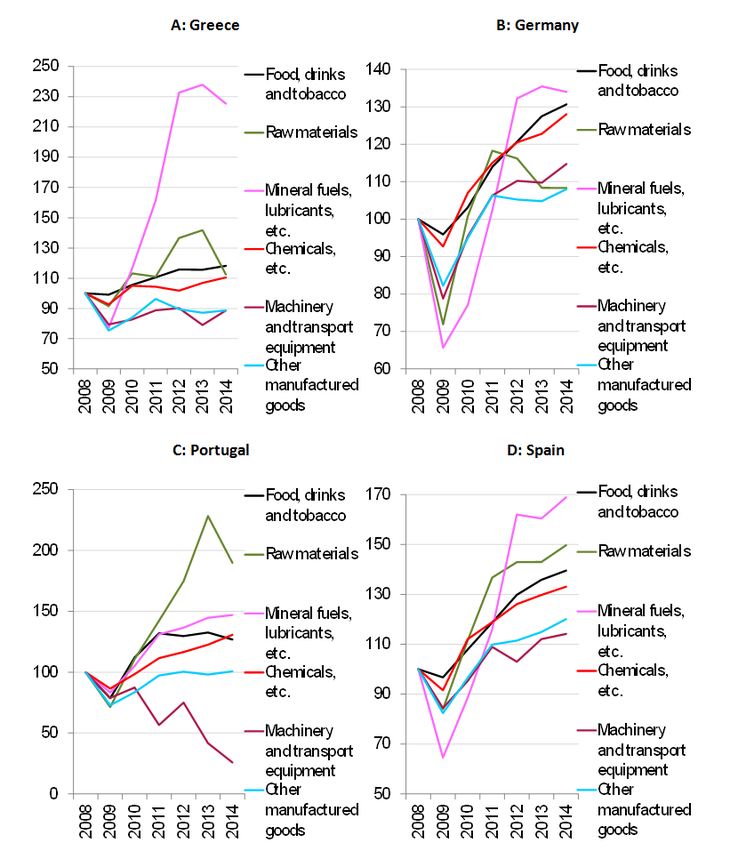

While there is some good news about Greek goods export dynamics, our evaluation must be nuanced, for three reasons:

· First, at constant prices Greek export dynamics are somewhat worse.

· Second, the composition of goods exports shows that the category “Mineral fuels, lubricants and related materials” is the primary driver of export growth (Figure 6), an industry which is characterised by low value added. While this category recorded the fastest growth in Germany and Spain too, in these two countries export growth is much more broad-based than in Greece.

· Third, Böwer, Michou and Ungerer (2014) estimate, using gravity models, that Greece exports a third less than regular international trade patterns would predict.

Figure 6: Exports of goods by type (2008=100), 2008-2014

Source: calculation using Eurostat data.

Böwer, Michou and Ungerer (2014) also conclude that weak institutions can explain much of the missing Greek exports puzzle. This implies that continued structural reforms should significantly boost exports.

The benefits of further reforms for GDP growth are highlighted by the calculations of Varga and in’t Veld (2014), who found that by closing half of the gap in structural reform indicators relative to 3 best performers, Greek GDP would rise 4% in 5 years and 18% in 20 years.

There continue to be major obstacles to growth, like the complexity of regulatory procedures

Clearly, despite progress with some of structural reforms in Greece in the past five years, there continue to be major obstacles to growth, like the complexity of regulatory procedures, enforcing contracts, state control, barriers to FDI and trade facilitation, and so on. Addressing these obstacles is difficult, yet their presence also implies that their elimination offers the prospect of growth.

Further good news concerning economic adjustment comes from the share of the tradable sector (defied as agriculture, manufacturing, trade, transport, tourism and ICT) in the private economy, whose decline reversed in 2010 and is now higher than in Germany (Figure 7). The increase in the share of the Greek tradable sector from 2010 was the consequence of a smaller fall of the tradable sector in 2010-12 than the fall of the non-tradable sector, while the tradable sector stabilised in 2013 and started to grow in 2014, when the non-tradable sector continued to shrink.

Figure 7: Share of tradable sector in private sector (%), 2000Q1-2015Q1

Source: calculation using Eurostat data.

Tradables: A: agriculture, forestry and fishing, C: Manufacturing, G-I: Wholesale and retail trade, transport, accommodation and food service activities, J: Information and communication.

Non-tradables: B, D, E: non-manufacturing industry, F: Construction, K: Financial and insurance activities, L: Real estate activities, M-N: Professional, scientific and technical activities; administrative and support activities, R-U: Arts, entertainment and recreation; other service activities; activities of household and extra-territorial organizations and bodies.

Not considered: O-Q: Public administration, defence, education, human health and social work activities.

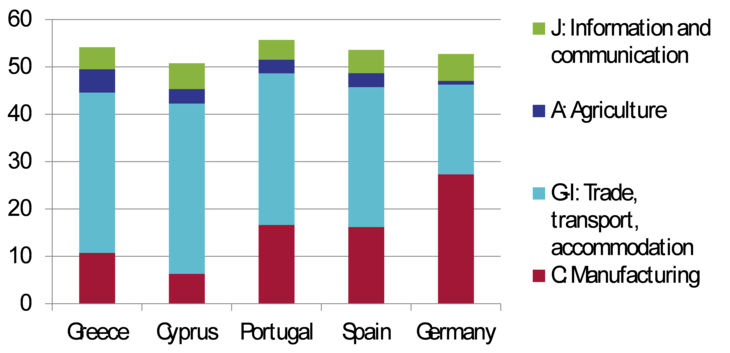

In Germany, manufacturing accounts for about half of the tradable sector, while the share of manufacturing is much lower in southern euro-area countries (Figure 8). This should not be a problem; for example Germany may have an advantage in designing and producing cars, while Greece may have an advantage in attracting visitors to seaside resorts.

Figure 8: Composition of the Tradable sector (% share in private sector), 2014Q4

Source/notes: see Figure 7.

Finally, let me note that following a dramatic collapse in employment, whereby far fewer people are employed in Greece (and also in Portugal) now than in 2000, job creation has resumed since early 2014 (Figure 9). This implies that the economy may have hit bottom in 2013 and absent suppressing factors like the uncertainty about Greek membership in the euro area and financial obstacles, the economy may rebound from its depressed state.

Figure 9: Employment (2000Q1=100), 2000Q1-2015Q1

Source: Eurostat.

Greece is destined to grow if a comprehensive and credible agreement is reached with the creditors and reforms continue

Is Greece destined to grow? If a comprehensive and credible agreement is reached with the creditors and reforms continue, then my answer is yes, for the following reasons:

- Transition to a new growth model has already started,

- Structural reforms have already been implemented,

- The continuation of structural reforms offers major improvements in exports and growth,

- The large fall in unit labour costs helps export performance,

- Only minor further fiscal adjustment is needed,

- The economy has likely reached the bottom in 2013 and deep recessions have been generally followed by quick recoveries,

- The euro-area and global environment is now more supportive than in the past.

Yet my positive assessment is conditional on a comprehensive and credible agreement, which would eliminate the risk of Grexit not just for now, and also on continued structural reforms, which seem politically difficult. If the agreement is not sufficiently comprehensive and credible, then uncertainty will continue and growth may not resume.

And if there is no agreement at all, then Greece will likely exit the euro area, which would lead, in my view, to further major falls in GDP, unemployment increases and paradoxically to fiscal tightening. Tax revenues would plummet due to collapsing GDP, and therefore even if the Greek government completely stopped servicing its debt, revenues would not be sufficient to maintain current expenditures. For lenders, a Grexit would likely mean writing down official loans to Greece and ECB lending to Greek banks. A Grexit would also make the euro area more vulnerable: whenever public finances of another government would come under stress, markets may also bet that country will exit the euro area as well.

The time has now come to find a wise and fair agreement.

This post is based on my presentation I gave on 3 June 2015 in Athens at the conference ”A New Growth Model for the Greek Economy”, organised by the Economic Chamber of Greece, the Greek Parliamentary Budget Office, the National and Kapodistrian University of Athens, the Democritus University of Thrace and the University of Peloponnese.

I thank Pia Hüttl and Allison Mandra for their help in data collection.

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

ΕΥΡΩΕΚΛΟΓΕΣ ΚΑΙ ΤΟ ΜΕΛΛΟΝ ΤΗΣ ΕΥΡΩΠΗΣ

Είναι γεγονός ότι οι τωρινές εκλογές λόγω της ανάπτυξης των κομμάτων του λαϊκισμού είναι κάπως διαφορετικές από τις προηγούμενες. Αλλά πιστεύω ότι όλε

After the ESM programme: Options for Greek bank restructuring

With the end of the Greece support programme, authorities now have scope to focus on the legacy of NPLs and excess private-sector debt. Two wide-rangi

A new statistical system for the European Union

Quality statistics are essential to economic policy. In this essay, Andreas Georgiou demonstrates the existence of fundamental risks inherent in the E