Greece budget update - October

The Finance Ministry of Greece has published the preliminary budget execution bulletin for September, covering the first 9 months of the year. It reve

While it has to be stressed that the targets considered in the budget execution bulletins are still those from the old 2015 budget (not the new targets under the new programme), this development is nevertheless an interesting reversal of previous tendencies.

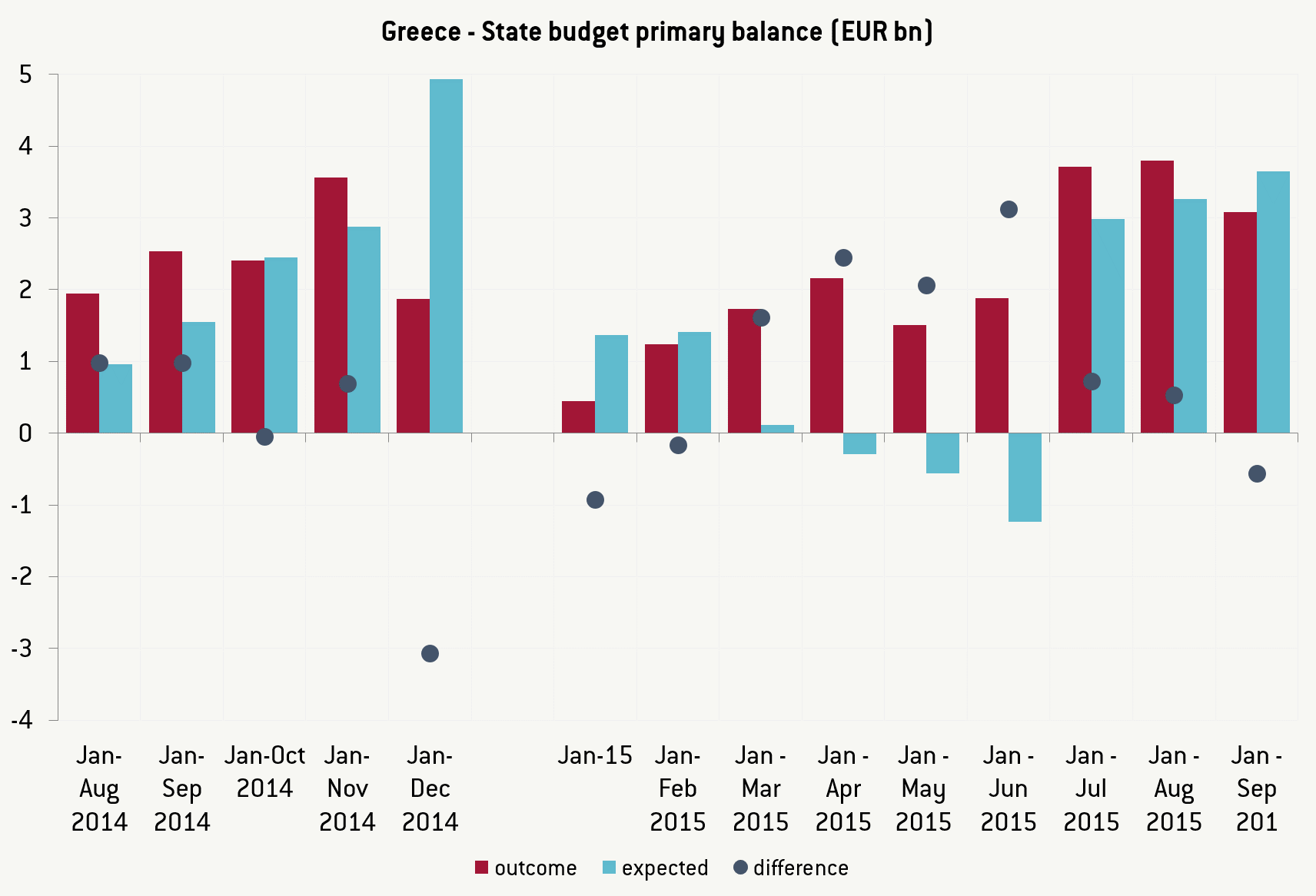

The cumulated state budget balance for the first 9 months of the year presented a deficit of 1.9 billion, against a target deficit of 1.4 billion. The state budget primary balance for January - September 2015 remains in surplus, but came in at 3.1 billion against a target surplus of 3.6 billion. Primary surplus overperformance had already eased in July and August, but September has shown the worst reading of primary surplus against the target since February (figure 1).

{kind=link}

Source: Ministry of Economy and Finance, Greece

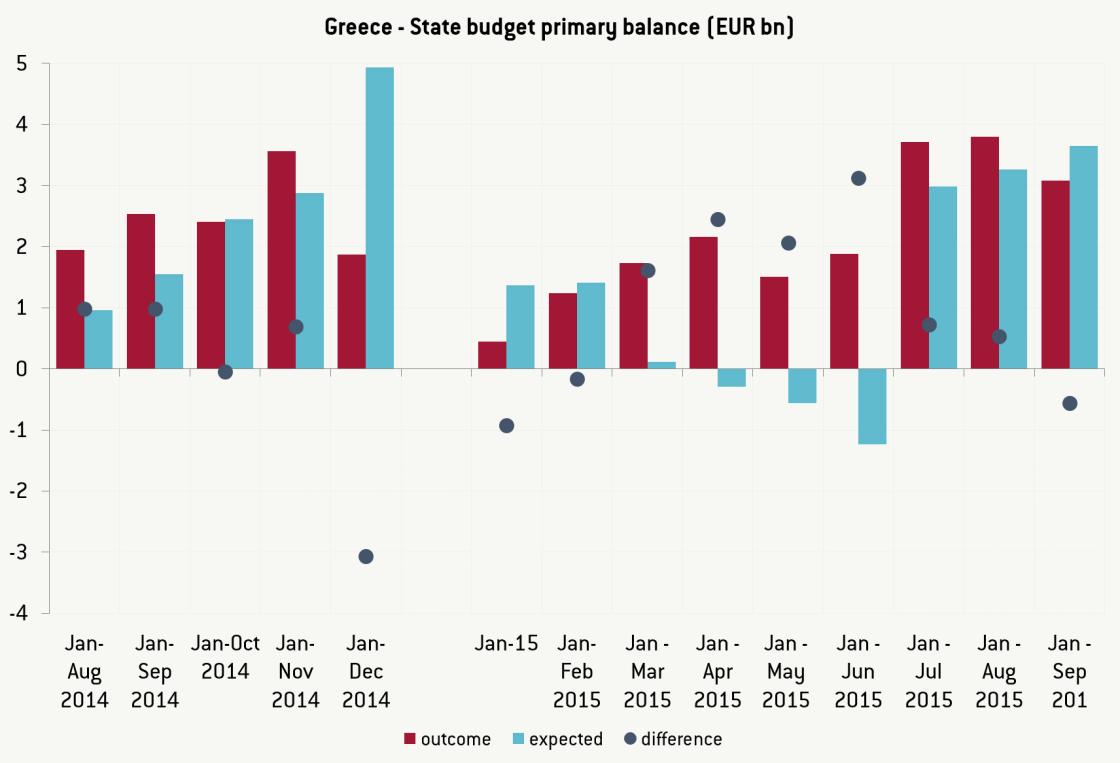

Revenues for the month of September fell back below expectations, reaching 3.5 billion euros, i.e. 762 million or 18% lower than the monthly target. On a cumulative basis, total revenues for the period January-September 2015 stood at 34.3 billion euro, against a target of 39.2 billion. This means that cumulative revenues for the first nine months of the year are currently 4.9 billion below target, and that the significant shortfall observed in July is still weighing on the revenue side. The preliminary statement once again refers to missed ANFA (holdings by National Central Banks’ in their investment portfolio) and SMP (securities market programme) revenues, as well as to non-assessment or receipt of ENFIA (the new property tax) as explanation for part of the shortfall.

{kind=link}

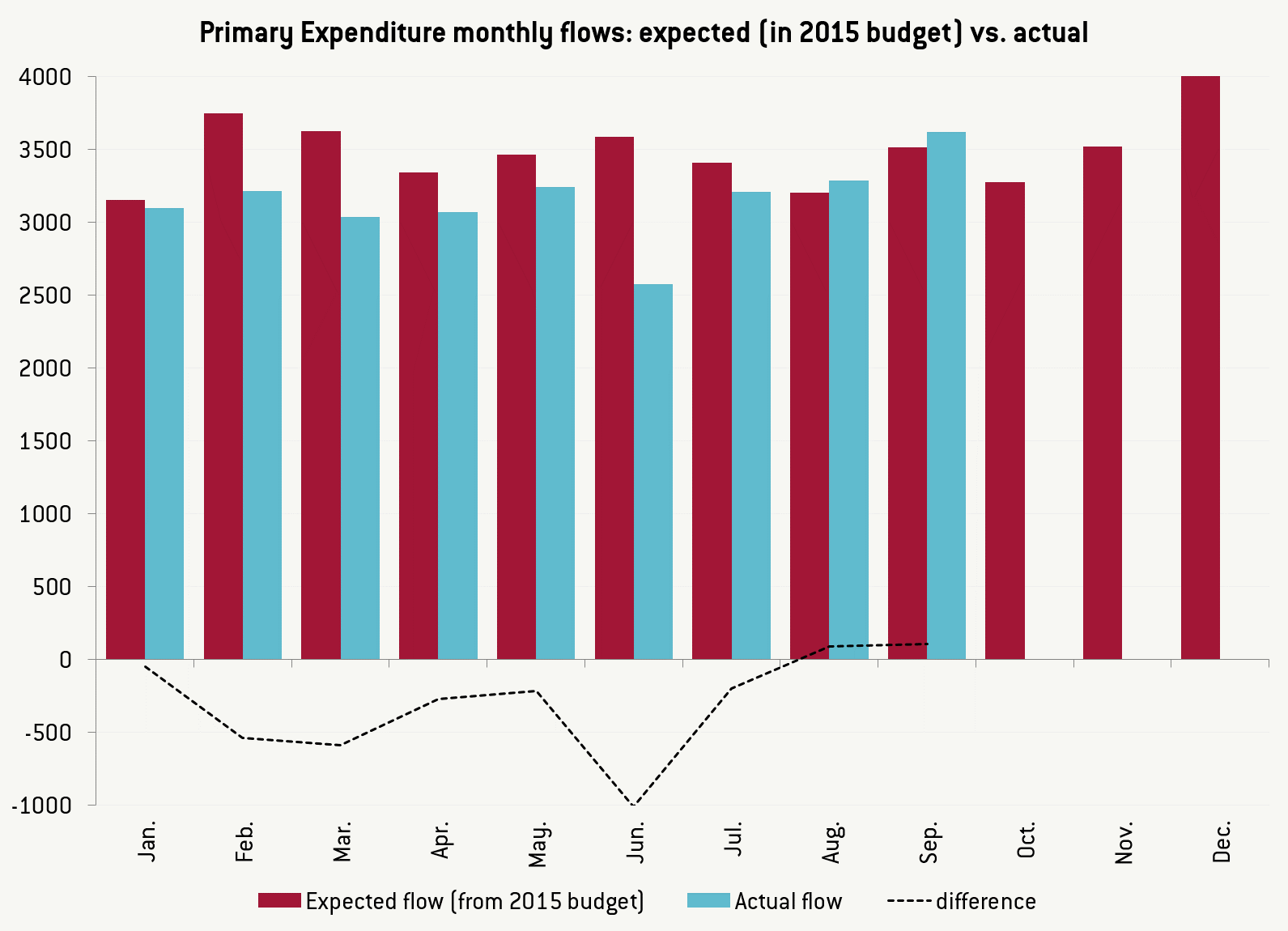

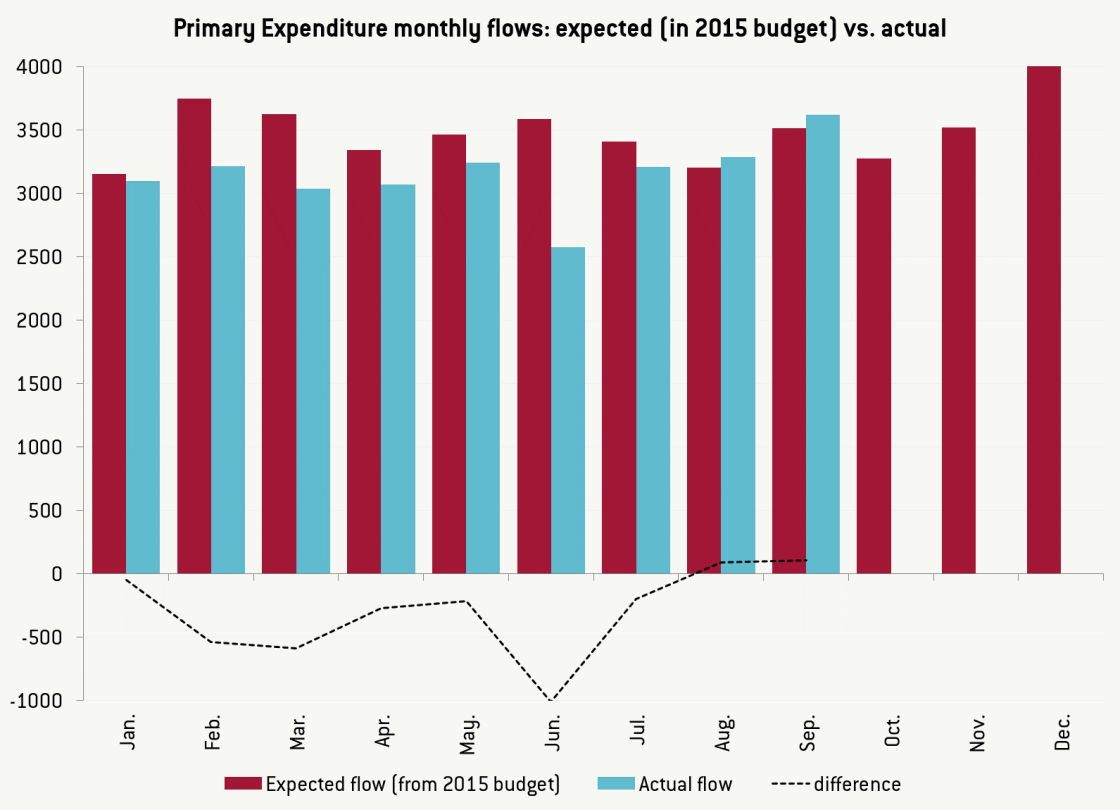

On the expenditure side, state budget expenditures for September amounted to 4.3 billion euros, 362 million higher than the monthly target (figure 2). This is the first time since the beginning of the year that total expenditures have exceeded their target, as until now the government had kept the primary surplus above target by drastically cutting expenditures. As a result, from January to September 2015, cumulative state budget expenditures amounted to 36.2 billion euros, 4.4 billion lower than the target. This development in monthly expenditures confirms the change that we highlighted last month, when primary expenditure had increased and slightly exceeded its target for the first time in months. In September, primary expenditure was again slightly above its monthly target (104 million). This translated into total expenditure overshooting for the first time since the beginning of the year (figure 3).

{kind=link}

Source: Ministry of Economy and Finance, Greece

The underperformance of revenues and relaxation of expenditure control, which we started to see last month, put pressure on the Greek budget in September. For the first time since February, the primary surplus has underperformed against the target. It needs to be stressed, however, that the targets against which the Ministry of finance evaluate the monthly budget execution are still those in the 2015 budget, but they will soon be updated with the new targets set in the recently discussed 2016 budget document. Whether those targets will prove to be more feasible remains to be seen.

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

ΕΥΡΩΕΚΛΟΓΕΣ ΚΑΙ ΤΟ ΜΕΛΛΟΝ ΤΗΣ ΕΥΡΩΠΗΣ

Είναι γεγονός ότι οι τωρινές εκλογές λόγω της ανάπτυξης των κομμάτων του λαϊκισμού είναι κάπως διαφορετικές από τις προηγούμενες. Αλλά πιστεύω ότι όλε

After the ESM programme: Options for Greek bank restructuring

With the end of the Greece support programme, authorities now have scope to focus on the legacy of NPLs and excess private-sector debt. Two wide-rangi

A new statistical system for the European Union

Quality statistics are essential to economic policy. In this essay, Andreas Georgiou demonstrates the existence of fundamental risks inherent in the E