German business on the crisis, growing political rifts and UK exit fears

The crisis is not over! This is the opinion of a large part of top managers from German DAX corporations and ten German banks surveyed by&nb

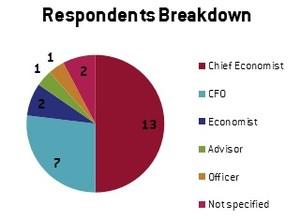

Bruegel and SWP surveyed German DAX corporations and ten German banks about their opinion as regards the situation in the euro area, the German economy and policies which the new German government should pursue. The results are presented in full in this blog and some of the results were presented in the policy brief 'Memo to Merkel: Post-election Germany and Europe'. Most respondents were either the chief economist or the CFO of the company (detailed methodology of survey below).

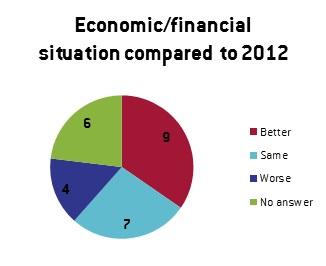

The crisis is not over! This is the opinion of a large part of the surveyed top managers. Only 9 of the 26 respondents indicated that the situation is better than one year ago. This is an astonishing number given that last summer many people feared a break-up of the euro area.

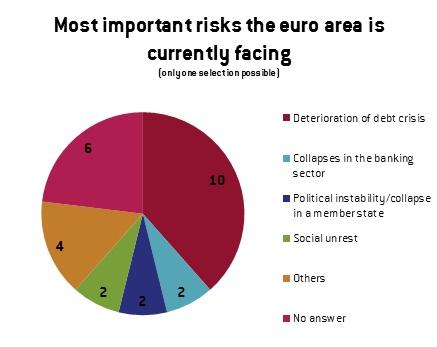

The deterioration of the debt crisis is clearly seen as the main risk but respondents also identify political instability, social unrest and collapses in the banking sector as risks.

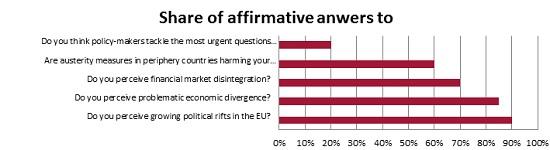

Ninety percent (90%) of the respondents see the growing political rift in Europe as a problem. More than 80% see problematic economic divergences, 70% see financial market disintegration and still 60% confirm that austerity measures in the periphery countries are harming their business.

What should Germany do?

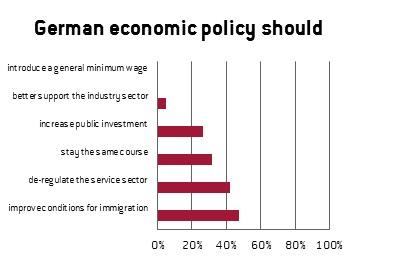

Business was asked what the German government should do. Domestically, the central points identified are conditions for immigration, service sector deregulation and public investment. Only around 30% of the respondents think that German economic policy should stay the same course.

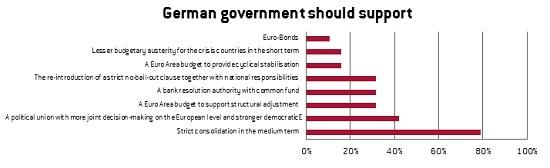

What policies for Europe?

Few of the currently discussed European policy discussion get high approval ratings by German business. Clearly, a strict fiscal consolidation in the medium run is shared as a good policy goal. Quite a number of respondents support a political union project, but bank resolution with a common fund or a euro area budget are not popular. Interestingly, a strict no-bail-out clause with a return to national responsibilities is likewise not seen as a right way by many. A “back to Maastricht” philosophy is thus not widely shared. Eurobonds receive no support.

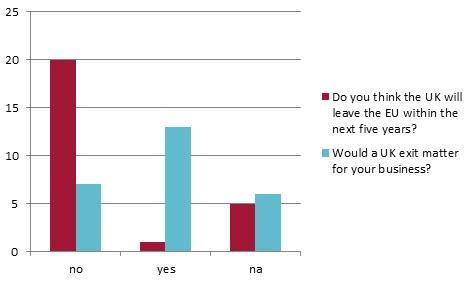

German business and the UK

An important issue is the recurring debate in the UK about repatriation of competences or even an exit of the UK from the EU. German business does not think that the UK will exit in the next 5 years. However, a large part of the respondents think that a UK exit would affect their business.

Bruegel and SWP also allowed for open answers and several business leaders gave comments, which are shown below in random order. Also the methodology of the survey is detailed below.

Background and methodology:

Bruegel and SWP surveyed the 30 German DAX corporations and 10 major German banks about their opinion of the situation in the euro area, the German economy and the policies that the new German government should pursue. Some of the answers were used in the policy contribution by Daniela Schwarzer and Guntram Wolff “Memo to Merkel” (Link)

The survey was conducted online on www.umfrageonline.com. A letter with the link was sent to the CFOs or the chief economists of the corporations and two reminders were sent. The first reply was submitted on the 16/07/2013, while the last reply dates 01/08/2013.

26 of the 40 people contacted opened the survey. 24 filled in answers. 23 finished the survey even though not all questions were answered.

Replies to open questions (in random order)

“Political rifts in the EU; economic divergence; financial market disintegration. Do these elements have repercussions for your business? The corporate sector more generally?” Comments on any of the three phenomena.

- “The impact is so far limited to sales growth, with clear signs of a bottoming out. The main risk is a protracted division in the Euro area between welfare enhancing states and those with stagnant or declining wealth. A healing of the Euro area depends on the stabilization of the banking sector. Long-term target has to be the renewed integration of the banking industry in the Euro area.”

- “Tax on Financial Transactions, i.e. Hedging, would lead to substantial damage, financially and from bureaucracy.”

- “The ongoing developments in the Eurozone affect business and the corporate sector generally for several reasons: Risks regarding the general stability of the economic, institutional und legal environment going forward; No ability to invest in peripheral Eurozone countries for risk of large investment devaluation through Euro-exit; Continuing distortions of asset allocation and investment allocation with risks of bubbles fed through loose monetary policy required to stabilize the Euro in absence of fiscal and political solutions”

- “Growing political rifts make international agreements on measures against debt crisis deterioration harder to achieve. Increasing political risk is hampering private sector risk appetite and thus prevents investments, especially in the peripheral countries (economic divergence). Without stronger capital spending (funded internationally) to lay the ground for future economic growth in the peripheral countries, they will face recessionary pressures for a long time and increasing solvency risks which would be a deterioration of the debt crisis, the greatest risk for the euro area.”

- “There will be divergence, but the politicians should allow for them and not try to stop them. This simply makes it worse over time.”

- “Fragmentation of Euro Banking market Is a Major Source of economic Disintegration in the EMU.”

- “The core of my business is not directly influenced by EU regulations/law.”

Which urgent questions are NOT tackled well by policy-makers?

- “Banking union, structural reforms and governance in the EU.”

- “Energy costs are the life blood of every economy. Europe always had a disadvantage vs. Middle East. Now the costs of the US are 1/3rd of European prices with growing impacts to the EU industry. Politicians talk and talk and wait.”

- “Banking Union design not appropriate to meet current and future challenges; Lack of EU-level strategy on fiscal and regulatory response to current situation."

- “The current strategy is one of pure austerity with some elements of structural reforms. The austerity has an adverse impact because it can only unfold its full potential in a system of flexible exchange rates; in a system of fixed rates it aggravates the debt problem by creating a spiral of reduced demand, shrinking GDP, shrinking tax base and revenues and increasing the debt burden. This dynamic reduces the public acceptance of structural reform measures and thus damages long term growth prospects as well. What is needed instead is a mechanism to stabilise demand without spending or taxation proliferation. This demand can only be fed through large scale privatisation in Europe in order to reduce debt and unlock efficiency potential in the public sector by reducing it and transferring parts of it into the private sector. None of this is happening.”

- “Incentivation of private sector foreign direct investment in the peripheral countries in order to boost their growth prospects. This would in turn help reduce the debt burden over the medium term (via a growth pick-up). Such incentivation could come through guarantees, rather than direct loans or subsidies that encourage banks and other financial institutions (insurance, private equity) to provide capital and loans for a restoration of the capital stock.”

- “Structural reforms, Debt crisis and Youth Unemployment.”

- “Big questions like: Energy, Protectionism, Currency imparities, Demographic Challenge, Environmental Challenge, Cut of National Spending to accelerate investments. Instead taxes are further increased, while governmental spending are not reduced.”

- “Comprehensive Banking Union”

- “Economic divergence, balance between debt reduction and social issues.”

- "Long term sustainable debt/financial management, social/political divergence within EURO area, North/South drift and long term demographic changes.”

- “Banking union, Common fiscal policy and further political integration.”

- “The Banking Union is moving too slow. In addition, an independent and separate (from the ECB) authority would be more optimal.”

How should German economic policy change?

- “Increase demography resistance of social security system.”

- “German economic policy should be more constructive and supportive of EU policy coordination.”

- “Germany needs to formulate a European growth agenda.”

- “Incentivise private investment in peripheral countries.”

- “Germany should stop rolling back the agenda 2010 reforms.”

- “Subsidies should be reduced.”

Comments on the future government’s priorities/Germany’s future role in the euro area.

- “Germany must stop to refuse thinking strategically and to refuse providing leadership; Germany should continue to oppose Eurobonds, but should consider asset backed Eurobonds or an asset backed scheme of debt reduction similar to the one the "5 wise men" have proposed. This would mean to put in all debt above 60% of GDP for all Eurozone countries into one commonly guaranteed debt repayment fund, but at the same time create a European holding of State Assets serving as an asset backed facility for the communalized debt and use privatization proceeds for debt repayment.”

- “The German government needs to keep up the pressure on other governments to consolidate their public finances and reform their labour, product and services markets - coupled with initiatives to mitigate the immediate adverse cyclical and social effects. Democratically elected governments in the periphery will otherwise struggle to introduce the necessary reforms in their countries. To this end, Germany needs to continue to play "the bad boy" for other member countries or otherwise risk that the bill it will have to pay in the future, ie, guarantees, losses of the ECB, ERM etc., becomes bigger and bigger.”

- “Several points:

- The euro-zone economy has contracted for six consecutive quarters. Immediate growth creation must be the overriding public policy priority;

- Structural reforms - liberalizing product and labour markets - both in individual EU countries (including Germany) and at EU level must be implemented. Regulatory measures inhibiting growth should be discontinued unless they affect fundamental protections;

- Germany's gross investment as a percentage of GDP has been declining for two decades. Investment in infrastructure - especially in high-tech telecommunications infrastructure - needs to be boosted;

- High-tech industries are engines of growth. Information and communication technology (ICT) is particularly important, as it is a key enabler many other economic sectors. However, Germany and Europe are losing ground. EU institutions, European governments and high-tech players need to shore up Europe's position in the ICT sector.”

- “Fiscal consolidation in times of deleveraging in the private sector is an additional brake on growth. It is not possible to reduce Public Budget Deficits in a recession.”

- "Strict consolidation in the medium/long term."

About the authors

Related content

The European defence industrial strategy: important, but raising many questions

The European defence industrial strategy helps to focus thinking but has significant flaws

Exporte nach Russland wirksamer kontrollieren

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up