Finland and asymmetric shocks

What’s at stake: Finland exemplifies the difficulty of dealing with asymmetric shocks within a Monetary Union as the Finnish economy has struggled to

Adjustment in the euro: Not a one-time problem

Paul Krugman writes that this is a reminder that the euro system creates huge problems for adjustment everywhere, that this isn’t a one-time problem. Adjustment can take place even with a single currency; but it’s a very slow and painful process. The single currency isn’t totally unworkable. It’s just extremely costly.

Paul Krugman writes that we’re increasingly seeing that the problems of the euro extend well beyond the troubles of southern European debtors. Economic performance has also been very bad in several northern nations with good credit ratings and low borrowing costs — Finland, Denmark (which isn’t on the euro but shadows it), the Netherlands. We’re seeing the classic problems of asymmetric shocks in a currency area that isn’t optimal. The problems of the euro, in other words, weren’t caused by an outbreak of fiscal irresponsibility that won’t recur if the Greeks can be brought to heel; they weren’t even, in a deep sense, the result of big capital flows that won’t come back again. The whole single currency project was flawed from the start, and will keep generating new crises even if Europe somehow gets through this one.

Lars Christensen writes that when the euro was set-up the general assumption was that asymmetrical supply shocks were rare and economically not important. However, the economic development in Finland over the past decade shows that asymmetrical supply shocks indeed can be very important economically.

Bad luck in Finland: Nokia, timber, Russia

Matt O’Brien writes that Finland has had some bad luck. It started when Apple made Nokia go from being synonymous with smartphones to being synonymous with old smartphones. As Finland found out, it isn't easy to replace a company that, at its peak, made up 4 percent of your economy. Obsolescence came for the timber companies next. There was nothing they could do to make people need as much paper, which until now had been a major export, in a post-paper world. And, on top of that, Finland has felt the effects of Russia, one of its biggest trading partners, staggering under the weight of low oil prices and Western sanctions.

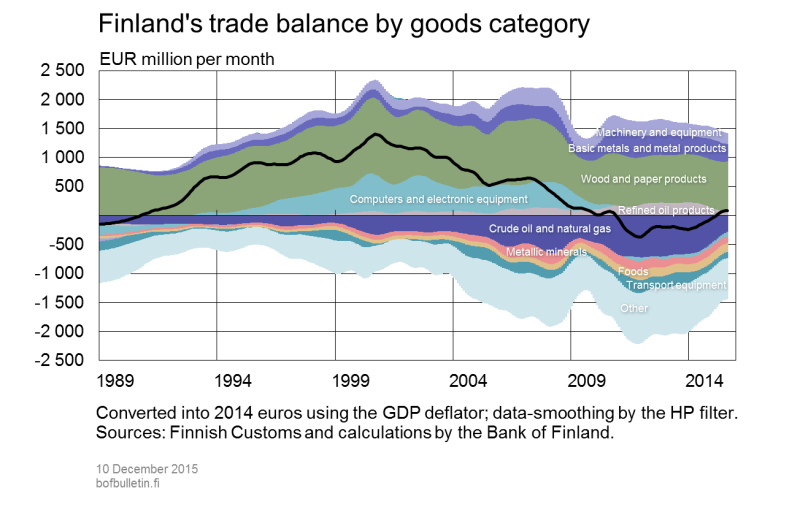

Source: Bank of Finland

Erkki Liikanen says that "four shocks" hit at the same time: the decline of Nokia and the country's paper industry, the retirement of a generation of baby boomers, high labor costs, which have made the economy uncompetitive, and the fallout from the Russian crisis. Simon Nixon writes that the cumulative result is that Finland’s export market share has shrunk by a third since 2008, wiping out what was a large current-account surplus and accounting for much of the decline in growth. Lars Christensen writes that for Finland there is indeed a “New Normal” – real GDP growth looks set to be permanently lower than it was in the 1990s and 2000s.

Three Finnish Depressions

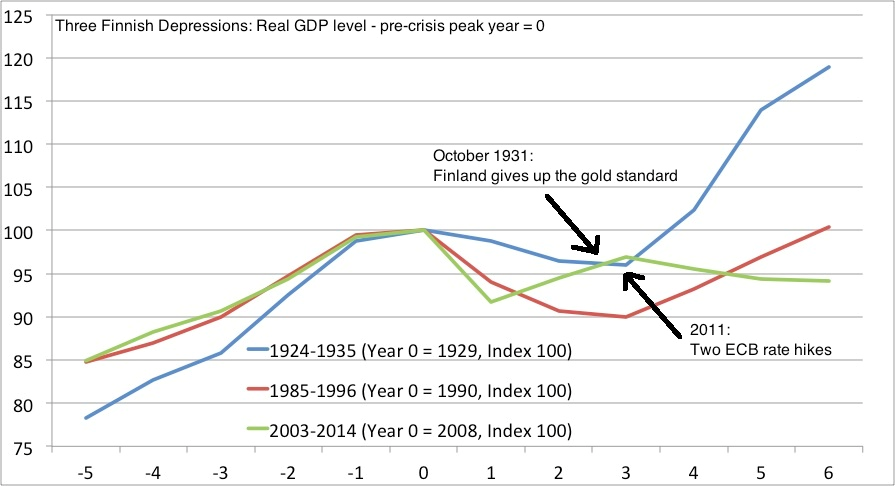

Marko Amnell writes that before it adopted the Euro Finland faced two severe recessions during its years of independence after 1917. The first was the Great Depression of the 1930s and the second was during the early 1990s (the causes of which included the collapse of the Soviet Union in 1991 and a banking crisis in the Nordic countries). Finland recovered from its economic downturns in the 1930s and the early 1990s, at least partially as a result of devaluing its currency, the Markka. Finland gave up the gold standard in October 1931, which was followed by a very strong economic recovery. Similarly, during the early 1990s, Finland followed a "strong Markka" policy of high interest rates, tying the Markka's exchange rate to the ECU currency basket (in the lead up to the launch of the Euro in 1999). This policy was abandoned in September 1992, allowing the Markka to float freely and devalue, which was followed by a strong economic recovery.

Source: Market Monetarist

{kind=link}

Simon Nixon writes that it is easy to exaggerate the role devaluation played in recoveries during the Great Recession. The U.K. recovery began only as its substantial post crisis devaluation started to reverse. In a world of increasingly open economies and interconnected supply chains, the benefits of devaluations aren’t clear-cut, potentially pushing up manufacturing costs and depressing consumer demand. Conversely, two of the fastest-growing economies in the EU now are Ireland and Spain, both of which are in the eurozone. It is also an open question what would have happened to Finland’s funding costs had it retained its own currency and tried to devalue and spend its way back to growth.

Erkki Liikanen writes that our challenges are based on structural facts. An adjustment of our currency would not make up for those challenges. If we had a little weaker Finnish markka, Nokia would still not beat iPhones and young people would not suddenly start to read printed books and newspapers and create demand for the products of Finnish paper mills.

About the authors

Related content

The fiscal stance puzzle

What’s at stake: In a low r-star environment, fiscal policy should be accommodative at the global level. Instead, even in countries with current accou

The state of macro redux

What’s at stake: In 2008, Olivier Blanchard argued in a paper called “the state of macro” that a largely shared vision of fluctuations and of methodol

Racial prejudice in police use of force

What’s at stake: This week was dominated by a new study by Roland Fryer exploring racial differences in police use of force. His counterintuitive resu

A tale of two treatises: the Werner and Delors Reports and the birth of the euro

Focusing on the Werner and Delors Reports, this essay aims to capture key ideas and debates, giving a chronological overview of the EMU process