The elimination of high denomination notes

What’s at stake: As high-denomination notes (HDNs) make it easier to transact crime, finance terrorism, and evade taxes, a number of commentators have

The case for killing HDNs

Peter Sands and Lawrence H. Summers writes that their advocacy for the elimination of high denomination notes is based on a judgment that any losses in commercial convenience are dwarfed by the gains in combatting criminal activity, not any desire to alter monetary policy or to create a cashless society. Peter Sands writes that getting rid of high denomination notes would not eliminate tax evasion, crime, terrorism, and corruption. But it would make life harder for those pursuing such activities, raising their costs and increasing the risks of detection. They would find substitutes – lower denomination notes, Bitcoin, disguising transactions through the banking system, even gold and diamonds. Yet each of these is, in one way or another, more costly, less convenient, and more prone to detection.

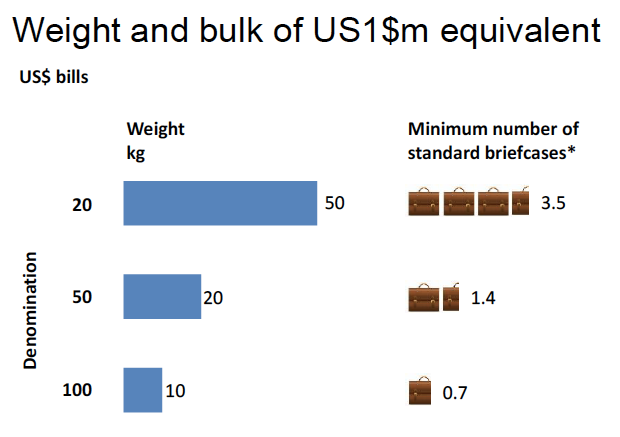

Peter Sands writes that the $100 bill and the €500 note are the payment instruments of choice for criminals across the world. Of course, the $100 bill is worth significantly less than the €500 note, but with over $1 trillion outstanding, the $100 bill is ubiquitous in criminal and corruption seizures all over the world. There are roughly thirty $100 bills for every US citizen, but only about 2% of American citizens have one in their wallet. Lawrence H. Summers writes that illicit activities are facilitated when a million dollars weighs 2.2 pounds as with the 500 euro note rather than more than 50 pounds as would be the case if the $20 bill was the high denomination note.

Lawrence H. Summers writes that when the euro was being designed in the late 1990s, he argued with my European G7 colleagues that skirmishing over seigniorage by issuing a 500 euro note was highly irresponsible and made clear that in the context of an international agreement, the U.S. would consider policy regarding the $100 bill. But because the Germans were committed to having a high denomination note, the issue was never seriously debated in international forums.

The moratorium idea

Lawrence H. Summers writes that the idea of removing existing notes is a step too far. But a moratorium on printing new high denomination notes would make the world a better place.

JP Koning writes that Summers' moratorium is an odd remedy. A moratorium simply means that the stock of $100 bills is fixed while their price is free to float. As population growth boosts the demand for the limited supply of $100 notes, their price will rise to a premium to face value, say to $120 or $150. In other words, the value of the stock of $100 bills will simply expand to meet criminals' demands. Another problem with a moratorium is that when a $100 bill is worth $150, it takes even less suitcases of cash to make large cocaine deals, making life easier—not harder—for criminals. To hurt criminals, the $100 needs to be withdrawn entirely from circulation, a classic demonetizaiton.

The case against killing HDNs

Colm McCarthy writes that there are lots of non-criminal users of large notes, not just horse dealers and bookmakers in Ireland but also wholesale traders in countries outside the Eurozone with dodgy currencies and unreliable money transmission systems. As much as half of all €500 notes is believed to circulate outside the Eurozone, especially in the Balkans, Turkey and Russia. Its predecessor was the German 1000 Deutschmark note, which circulated widely in these places, and the ECB version was consciously introduced so as to facilitate existing users.

JP Koning writes that the U.S. provides the world with a universal backup monetary system. Removing the $100 would reduce the effectiveness of this backup. The citizens of a dozen or so countries rely on it entirely, many more use it in a partial manner along with their domestic currency. The very real threat of dollarization has made the world a better place. Think of all the would-be Robert Mugabe's who were prevented from hurting their nations because of the ever present threat that if they did so, their citizens would turn to the dollar. Foreigners who are being subjected to high rates of domestic inflation will find it harder to get U.S dollar shelter if the $100 is killed off.

Ashok Rao writes that there is an information tradeoff. Imagine if criminals transacted only in $10,000 notes. It would be reasonably easy for intelligence agencies to sneak a traceable note to probe criminal networks. This would be close to impossible with a $20 note (not the least because this is a high velocity note used by normal people).

Ashok Rao writes that the demand for criminal service is likely many times more inelastic than supply; especially drugs. A tax would hurt poor consumers, not drug dealers. A more direct method might be to increase the expected penalty of criminal activity.