Abenomics: Is Shinzo aiming in the right directions?

Japan’s stock markets have seen an unusual fluctuation these weeks. The Nikkei 225 has dropped by 20% after it hit this year’s highest on 23 May.

Japan’s stock markets have seen an unusual fluctuation these weeks. The Nikkei 225 has dropped by 20% after it hit this year’s highest on 23 May. This could be the result either of the adjustment after a sharp stock price rise or of markets’ sceptical reaction to the “three arrows” of “Abenomics” after a first frenzy. Still, the direction of these three arrows deserves a deeper attention.

The first arrow – extraordinary quantitative and qualitative monetary easing – signalled the strong will of the Bank of Japan to end 15-year-long deflation. It has been launched towards the right direction to reach this aim. But, as the benchmark bond yield rose above 1%, concerns about its side effects (e.g. an asset price bubble, a sharp decline of bond prices, and difficulties in exiting from extraordinary monetary easing) started to rise. Indeed, these concerns are rooted, to a greater extent, from a sceptical view on the second and third arrows which are comprehensively described in Prime Minister Abe’s “Basic Policies for Economic and Fiscal Management and Reform” released today.

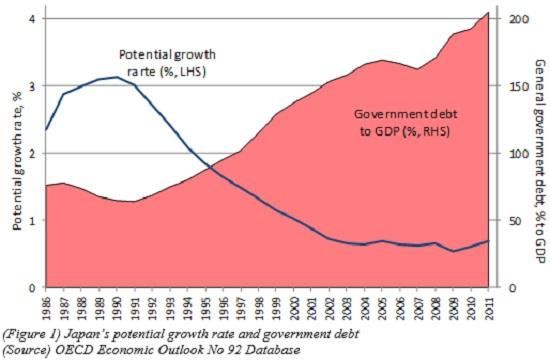

In order to realise sustained economic growth, the government priorities should be first to reduce its debt and to raise its growth potential, taking into account the current miserable situation (figure 1). The second arrow – increased spending on public investment – has already been launched at the wrong direction. Last January, the government decided the bigger-than-ever supplementary budget, and it has speeded up the amount of spending to support the economy. Now, Japan’s economy recorded 1.0% growth (quarter-to-quarter) in the first quarter this year and is expected to grow by 2.5% in FY2013. Those figures confirm that fiscal measures are not necessary to stimulate Japanese growth.

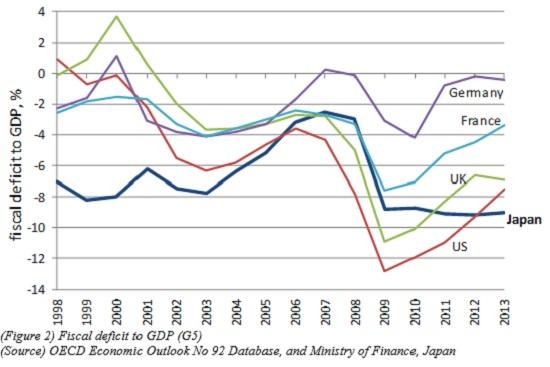

The target of the second arrow should have been the fiscal reform. Current fiscal situation in Japan is not sustainable, and this view has been shared by a number of papers. According to the simulation by Hoshi and Ito, the debt level will exceed private sector saving by 2024. This means that the government would run out of room to sell more bonds domestically in 2024 at the latest. Their simulation also clarifies that, even if interest rates are favourable throughout the projection period, the government should increase its tax burden ratio by 1% each year form 33% in 2016 to 46% in 2029 and keep that ratio until 2070. In the early 2000s, the LDP government made efforts for fiscal consolidation by setting the ceiling of its new bond issuance at 30 trillion yen and the amount of debt began declining after 2005. However, after the Lehman Shock occurred and the DPJ became in office, the ceiling was set at 44 trillion yen in 2010 and Abe government took over it. Most advanced countries now try to shrink their budget deficit which expanded during the crisis period, but only Japan kept it crisis level (figure 2).

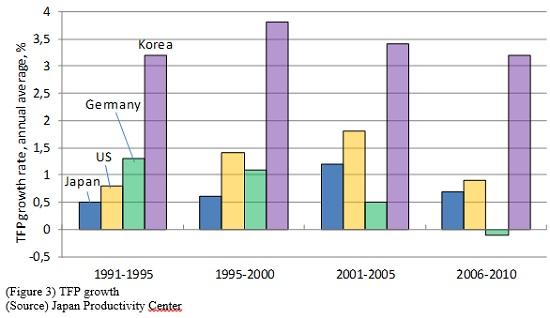

Japan has no choice but raises its total factor productivity (TFP) growth, stuck on low levels for the last 20 years (except the period of so-called Koizumi reform between 2001-06; figure 3) by facilitating regulatory reforms and openness of the country in order to ensure its long-term sustained growth without accumulating the amount of debt. For the third arrow – a growth strategy –, the Council for Regulatory Reform submitted its recommendation to the government early this month, which was incorporated into the growth strategy, together with public projects and investments. In addition, according to the Basic Policies the proportion of the volume of trade with using FTA should be increased from current 19% to 70% within five years. The growth strategy sees agriculture and healthcare industries as an example of promising industries as well as knowledge-based industries. Therefore it will promote public projects for these industries.

The growth strategy, however, does not include some crucial structural reforms which attract investment in Japan, such as reduction of corporate tax rates and deregulation on dismissal of workers. For promising industries, reforming some regulations which promote new entries to or raise competitiveness, such as further deregulation on entries of private enterprises and public insurance reforms, are pigeonholed partly due to the leading party’s anxiety that it might lose supports by relevant interest groups at the election.

The expression “three arrows” derives from a maxim by a “busho” (warrior) of the warring states period in Japan, Motonari Mouri. He preached the importance of getting united to his vassals, saying that even if a single person (arrow) is weak, a group of people is always stronger(a bundle of three arrows). With Abenomics the story is different. Every arrow should be sufficiently strong alone and all the three measures should be addressed to the same direction. An early stage exit from monetary easing would give the fiscal side a heavier burden to bridge its output gap. Ill-coordinated fiscal expenditures would not contribute to sustained growth. The failure of either fiscal reform or growth strategy would postpone the exit from extraordinary monetary easing even after the target of 2% inflation rate is achieved, which might cause greater side effects to the economy such as an increase in the interest rate. A vicious circle may appear. The right direction is to seek a moderate, sustained and productivity-driven growth. That way the word “Abenomics” will represent a model of a fiscal and monetary policy mix, with a solid growth strategy implementation.

Reference;

Hoshi, T., and T. Ito (2012), Defying Gravity: How Long Will Japanese Government Bond Prices Remain High?, NBER Working Paper 18287.

Related content

Zooming in US-China tech rivalry

A comparative exploration of US-China innovation frontiers

China’s ‘new productive forces’ risk overcapacity bubble

India's economy can overtake China's if it can stay on track