Persistent COVID-19: Exploring potential economic implications

We see three main economic implications of a scenario of recurrent outbreaks: lasting border restrictions, repeated lockdowns and enduring effects on

This essay is part of a PIIE series on Economic Policy for a Pandemic Age: How the World Must Prepare for a Lasting Threat.

When the COVID-19 crisis spread in early 2020, many economists who stepped forward with projections of its impact assumed that a one-time shock would be followed eventually by a return close to the status quo. Views have differed since then regarding both the time it would take to produce vaccines and the extent of potential economic scarring, but, until the last few months, few outside the public health community seriously contemplated the possibility that the pandemic could persist on a significant scale.

The emergence of new variants of SARS-CoV-2, the virus that causes COVID-19, has made this assumption questionable. While not the most likely outcome, worse scenarios can no longer be excluded. (For various adverse scenarios along these lines, see, for example, figure 3 in Bosetti et al. 2021.) As our colleagues Chad P. Bown, Monica de Bolle, and Maurice Obstfeld explain in a recent post, the periodic emergence of new, potentially dangerous variants will remain a serious threat so long as parts of the world lack access to effective vaccines.

If COVID-19 persists and keeps threatening lives, two scenarios then seem possible. The first is recurrent waves of infection, leading governments to oscillate between imposing and lifting sanitary measures in response to the ups and downs of the disease. The second is a “zero COVID” scenario: sharp and sustained containment policies at the start, followed by milder sanitary measures combined with systematic tracing and testing to maintain a very low infection level thereafter. While the evidence suggests that this second scenario would lead to lower long-term human and economic costs, geographic, human, and political realities within and across countries make it less likely to happen, at least in the case of densely populated, open, tightly integrated economies such as those of Europe. For this reason, this blog focuses on the implications of the first scenario.

We see three main economic implications of a scenario of recurrent outbreaks. The first is lasting border restrictions, as countries try to protect themselves from infections elsewhere. The second is the likelihood of repeated lockdowns. The third is enduring effects on the composition of both supply and demand. We now explore each of these implications in turn. (A later blog will draw lessons for economic policy.)

- Lasting border closures

Cross-border air transportation of passengers declined by more than 90 percent in April-May 2020 and was still 64 percent below the normal level in December, according to the International Civil Aviation Organisation (ICAO), a specialised UN agency. In January 2021, further border closures were announced, especially in Europe. The United Kingdom, for example, has banned entry from more than 30 countries and imposes a 10-day self-isolation period on anyone arriving from any country other than Ireland.

Suppose these travel restrictions persist. How costly, in economic terms, are they likely to be?

Some effects (on foreign tourism, airline companies) are obvious and substantial. International tourism, which raked in $1.7 trillion in 2019, or 1.9 percent of world GDP, dropped by 74 percent in 2020. This does not translate one for one into a loss of economic activity, as nationals, now forced to stay at home, may offset some of the hit, but only in part (French nationals may not want to visit the Eiffel Tower again). Consequences are likely to be very bad in places like the Maldives or the Bahamas, where the tourism sector accounts for more than 50 percent of GDP, and severe in countries such as Greece, Italy, or Spain where it accounts for more than 10 percent of GDP and employment (and where foreign tourism declined by 70 to 80 percent in 2020). But, even for a highly diversified country like France, foreign tourism accounts, directly and indirectly, for about 3 percent of GDP.[1]

[1] In France, tourism accounts directly for 7 percent of GDP and indirectly for about 10 percent of GDP. Foreign tourism accounts for 30 percent of total tourism.

Restrictions on seasonal migrants, especially in agriculture, can also have a substantial effect. Travel restrictions will both disrupt crop harvesting (in host countries) and affect remittances (to home countries).

Some effects are more difficult to assess but may be deeper. One major issue is how travel restrictions would affect the organisation of global value chains, trade in goods, non-tourism services, and productivity.

By itself, the transportation of containers implies minimal in-person contacts. Once procurement or export contracts have been signed, the impact of air travel restrictions on people is minimal. But the mobility of persons does matter for the establishment of a value chain. More precisely, multinational production networks are subject to three types of frictions (Head and Mayer 2019): trade costs, marketing costs, and production coordination costs. Restrictions on travel do not affect the first one, but they do affect the other two. Delpeuch et al. (2020) develop and apply a model along these lines to the car industry and find that a 20 percent increase in all cross-border costs would typically reduce consumer real income by about 4 percent.

Some evidence on the economic impact of decreased passenger travel can also be gathered from various natural experiments. Bernard, Moxnes, and Saito (2019) have shown that the opening in 2004 of a passengers-only high-speed train line to southern Japan broadened the available set of suppliers and sourcing locations, producing significant effects on firm-level performance.

This suggests that face-to-face interaction between individuals matters for productivity. Umana-Dajud (2019) uses another natural experiment: the introduction by the Schengen area of visa requirements for citizens of Ecuador (in 2003) and Bolivia (in 2007). He finds in both cases a significantly large negative effect on trade with Spain (the country most affected by the change in visa status), especially in differentiated products.[2] These findings are echoed by Coscia, Neffke, and Hausmann (2020), who look at the impact of business travel on the dissemination of what they call tacit knowledge (the kind of knowledge that is difficult to transfer to another person by writing it down or verbalising it). They suggest that, through this channel, lasting impediments to cross-border mobility would have detrimental effects on growth. Countries that depend more on foreign trade would be affected more, especially those exporting services.

[2] We are grateful to Thomas Chaney and Thierry Mayer for directing us to these papers.

Constraints on studying abroad—the suspension of the Erasmus program in Europe, for example, or the decrease in foreign students and faculty in US colleges and universities—would gradually reduce cross-border cooperation in research. Universities and colleges that cater largely to foreign students might not survive. More fuzzily, but importantly, students would lose precious knowledge of other cultures.[3]

[3] For an estimate of some of the costs of a related measure, see PIIE Working Paper 20- “Short- and Long-Term Costs to the United States of the Trump Administration’s Attempt to Deport Foreign Students,” by Sherman Robinson, Marcus Noland, Egor Gornostay, and Soyoung Han.

Can one put a number on these costs? Not easily. Restrictions lasting a year or two might not have much effect. Longer-lasting impediments could, however, have a substantial effect on global value chains, trade, and overall efficiency.

- Recurring lockdowns

Under a scenario of recurrent outbreaks, governments are likely to implement stop-and-go measures, with lockdowns of varying intensity followed by relaxation. How costly, in terms of economic activity, might these measures be?

Several factors should make future lockdowns less costly than the initial set of lockdowns in the spring of 2020. There has been learning: Shortages of masks and protective equipment have largely disappeared, production sites have been restructured to contain contamination, working from home is better organised, and click-and-collect retail sales have developed. Governments have a better, although still surprisingly limited, sense of the specific channels of transmission among different groups and can do more surgical interventions and closures.

At the same time, however, there have been clear signs of lockdown fatigue, leading people to be less respectful of rules and less careful about their behaviour.

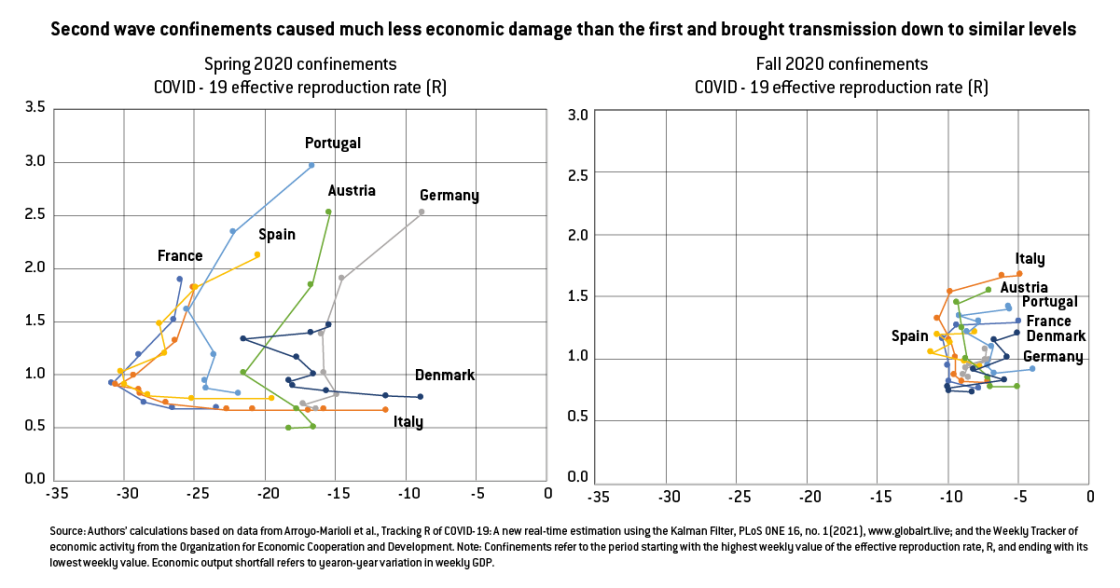

To get a sense of whether there was progress, we focused on seven European countries that had two clear lockdowns in 2020, one in the spring and the other in the fall. The countries are Austria, Denmark, France, Germany, Italy, Portugal, and Spain.

For each of the two lockdowns, we looked at the period starting with the highest value of the COVID-19 effective reproduction rate, R, and ending with its lowest value.[4] This period typically coincided closely (differing by a couple of weeks at most) with the official lockdown period and with a sharp increase in the Blavatnik stringency index, an index aimed at measuring the intensity of lockdown measures. The period lasted between six and nine weeks across episodes and countries.

[4] Explanation of the time course of an epidemic can be partly achieved by estimating the effective reproduction number, R(t), defined as the actual average number of secondary cases per primary case at calendar time t (for t >0). R(t) shows time-dependent variation due to the decline in susceptible individuals (intrinsic factors) and the implementation of control measures (extrinsic factors). If R(t)<1, it suggests that the epidemic is in decline and may be regarded as being under control at time t (vice versa if R(t)>1).

As a measure of the effect on infection, we looked at the change in R, as constructed by Arroyo-Marioli et al. (2021).[5] As is well known, a value of R above 1 means an increase in infections, and a value below 1 means a decrease in infections. Not surprisingly, all episodes started with a value of R above 1 and ended with a value below 1.[6]

[5] Alternatively, we have used changes in hospitalisations as a lagged indicator of R. Results are qualitatively similar.

[6] We converted the R data into a weekly series, so that the frequency matches that of the data from OECD’s Weekly GDP Tracker.

As a measure of the effect on the economy’s output, Y, we used the Weekly Tracker of economic activity constructed by the Organisation for Economic Cooperation and Development (OECD).[7] Given the definition of the tracker, a value of 0 in the graph means that the estimate of GDP in a given week is equal to its value for the corresponding week a year earlier (thus eliminating issues of seasonality). A negative value means that the estimate of GDP is lower than the value for the corresponding week a year earlier.

[7] The GDP tracker gives the estimated value of weekly output relative to the same value a year earlier, implicitly taking the earlier value as the normal level of output. It can be thought of as eliminating issues of seasonality.

The evolution of R and Y for each country and each of the two episodes is shown in the two panels of the figure. The left panel shows the outcome in the first episode, the right panel the outcome in the second episode. In each case, the movement is counter-clockwise, starting from the top. Summary statistics are given in the table.

The figure and the table suggest the following conclusions:

- The movements in R and Y were substantially larger in the first than in the second lockdown. R started higher, and the output cost throughout the decline in R was much larger. The end value of R was also a bit higher in the second than in the first lockdown, suggesting that governments were under pressure to lift restrictions on social life before their public health objectives were fully achieved.

- The first lockdown was characterised by a large heterogeneity of outcomes across countries. Germany ended with the same low value of R as France but at roughly half of the output cost. The second lockdown, in contrast, was much more homogenous, with most countries ending with roughly similar values of R at roughly the same output cost.

- More important for our purposes, the output cost associated with reaching the same value for R was substantially smaller during the second lockdown, between 1/2 and 1/3 of the cost during the first lockdown. Looking at it another way—by comparing the corresponding trajectories of R from, for example, 1.5 to 0.7 in both panels—the output cost per week was far smaller in the second lockdown, roughly 7 to 10 percent of weekly GDP.

This is clearly only a rough first pass at the data. The evidence, however, is clear that these countries were able to contain contagion at a lower output cost during the second lockdown. As more is learned and policies can be better targeted, an even better trade-off may be achieved if new lockdowns are needed. But for now, the economic cost of the second rather than the first lockdown should be taken as a starting point.

- Changes in both demand and supply

Under a scenario of recurrent outbreaks, people are likely to change behaviour even outside of formal lockdown episodes. The notion of a post-COVID-19 world where we can ignore the virus and go back to the way life was will no longer be a given. The perceived risk of infection, even if one has been vaccinated, infected in the past, or both, will remain. People will continue to be reluctant to go to restaurants, theatres, stadiums, and other public places regardless of formal lockdown policies—as they were in spring 2020 when some US states decided to reopen nonessential businesses amid the pandemic wave.[8] These contact-intensive sectors will suffer all year long, whether or not they are subject to legal restrictions.

[8] Chetty et al. (2020) provide compelling evidence that state-ordered reopenings had modest effects on consumer spending and economic activity.

In France, for example, highly affected companies (ie, companies whose turnover was at least 50 percent below normal) accounted for 7.5 percent of private employment at the end of 2020, according to the ACEMO survey. They were heavily concentrated in a few sectors. In a persistent COVID-19 scenario, temporary support schemes may fail to provide a solution and many of these companies may end up closing, with severe consequences for employment. If so, significant labour reallocation and reskilling will have to take place.

Even if most companies adapt and survive, lasting restrictions on economic activity will result in significant damage. Evidence so far is that liquidity support has been effective and corporate bankruptcies, at least so far, have diminished. But as corporate debt increases, insolvency cases are bound to multiply. Part of the cost will be passed on to public finances, through write-offs, at a substantial budgetary cost.

Saving and investment may also be substantially affected. A common hypothesis has been that there might be an exuberant post-COVID-19 phase, with pent-up demand, reflecting the large accumulated excess savings together with the desire to make up for the tough pandemic episode. Buoyant growth would follow. This is less likely to occur if there is no clear post-COVID-19 phase. People may continue to save, as a precaution against an uncertain future. Many firms have been hit severely. With profits down and uncertainty still pervasive, they may be reluctant to invest and may keep hoarding liquidity in case times become tough again. This will be detrimental to both potential output and aggregate demand. The government may not only have to protect people and firms but also sustain demand to maintain the economy at (diminished) potential. This again may come at a substantial budgetary cost.

An old theme in macroeconomics is hysteresis: long-lasting effects of temporary shocks. The evidence from past recessions remains mixed (Blanchard 2018), but under a scenario in which COVID-19 remains prevalent for a few more years, lasting scarring effects become increasingly likely. Long-term unemployment ends up having psychological effects, even if the unemployed are financially compensated. The starkly unequal effects of lockdowns on the quality of education, be it for students in school or in college, have already been documented and they are sobering. For example, Chetty et al. (2020) found that six weeks after the spring 2020 US school closures, the number of completed lessons on an online math platform had dropped by more than 40 percent in schools with low-income students against less than 10 percent in schools with high-income students. These numbers are likely to be even worse if in-person teaching remains limited for an extended period.

Conclusion

It is too early to know the exact contours of the next COVID-19 phase, and how long it will last. Hopefully vaccines will get us back quickly to the life we knew before COVID-19. But if they do not, the initial policy strategy will need to be revisited and probably modified. This will be the subject of our next post.

The authors are grateful to Michael Kister for excellent research assistance, to Nicolas Woloszko for guidance on the OECD data and to Laurence Boone, Philippe Martin, Guntram Wolff, and PIIE colleagues for comments and criticisms on an earlier draft.

Recommended citation:

Blanchard, O. and J. Pisani-Ferry (2021) 'Persistent COVID-19: Exploring potential economic implications', Bruegel blog, 12 March

About the authors

Related content

Coordination for EU Competitiveness

The economic implications of climate action

Bringing the reform of European Union fiscal rules to a successful close

EU fiscal rules must not unnecessarily restrict green investment.

Income inequality hardly changed during the COVID-19 pandemic

Contrary to expectations, there was no widespread increase in either within-country or global income inequality during the pandemic