Regulating big tech: the Digital Markets Act

The European Union’s proposed Digital Markets Act will attempt to control online gatekeepers by subjecting them to a wider range of upfront constraint

Digital market forces drive huge efficiency gains. But they also create winner-take-all dynamics that can, left unchecked, lead to monopolistic markets and hurt consumers in the long-run. Slow-moving competition policy tools are ill-equipped to fully address these digital concerns.

(1) The DMA was proposed alongside the Digital Services Act (DSA) which targets illegal goods, services and content, abuse of platforms, advertising and algorithmic transparency. The DSA concerns most online businesses.

In December 2020 the European Commission proposed the Digital Markets Act (DMA) to regulate the gatekeepers of the digital world by imposing direct restrictions on the behaviour of tech giants (1). While the Commission has not named any companies, it has proposed criteria that are sure to catch Google, Facebook, Amazon, Apple, Microsoft and SAP, among others.

This blog unpacks the different provisions of the DMA and explains why the Commission chose to regulate big tech.

What is a digital gatekeeper?

A gatekeeper is a company that acts as an important nexus between two or more groups of users – say buyers and sellers. When they attract a large share of users on one side of the platform (say buyers) gatekeepers can become unavoidable tolls on routes to certain markets or customers. Users on the other side of the platform (say sellers) may have little choice but to use the gatekeepers’ infrastructure.

The EU has thought in terms of ‘digital gatekeeper’ for as long as Google has existed. In the DMA, it defines a gatekeeper as a platform that operates in one (or more) of the digital world’s eight core services (including search, social networking, advertising and marketplaces) in at least three EU countries and:

- Has a significant impact on the internal market (defined quantitatively as an annual turnover of €6.5 billion or a market capitalisation of €65 billion);

- Serves as an important gateway for business users to reach end-users (user base larger than 45 million monthly end-users and 10,000 business users yearly); and

- Enjoys an entrenched and durable position or is likely to continue to enjoy such a position (meets the first and second criteria over three consecutive years).

A platform that meets these quantitative thresholds is labelled a gatekeeper. However, the Commission would retain the right to remove (or confer) ‘gatekeeper’ status by qualitative assessment. The Commission would also be empowered to alter the thresholds as technologies change, and to conduct market investigations to look for new gatekeepers.

Why big tech is big

Digital hubs are a time drain. In December 2019 (pre-COVID-19), the average Italian spent 45 hours a month on Facebook, and 24 hours on Google. The same may be true for physical marketplaces and social venues, but online, the hubs are controlled by only a handful of global players. British internet users spend 40% of their online time on sites owned by just two providers (Google and Facebook). These same two providers are frequented by 96% and 87% of British users each month. A third of Germans that book their holidays online do so through just one site (Booking.com).

For a long time, policymakers were not especially worried about high concentration in digital markets. They assumed digital champions faced competition ‘for the market’, that is, competition from outside players keen on becoming tomorrow’s winners. After all, Facebook outcompeted MySpace. Google overtook AltaVista. Nokia once looked unassailable.

But the competitive dynamics of the early days of the internet no longer seem to apply. While the primacy of AltaVista lasted one year (and Myspace three years), a decade of that of Google and Facebook has now passed. The persistence of today’s digital leaders has become concerning: have they found a way out of the competitive race?

There are several explanations for the unusual persistence of digital leadership. For one, digital markets feature characteristics of ‘tipping markets’, or markets in which there is room for only a few players. These characteristics are the combination of:

- Consumer inertia (why bother shop for a new email provider when the current one works just fine?);

- Increasing returns to scale (recommendation algorithms become better with more users);

- Low marginal costs (it costs close to nothing to distribute one extra app);

- Strong direct and indirect network effects (the more users frequent a social media site, the more attractive it becomes to other users and to advertisers).

To illustrate, consider the market for mobile operating systems (OS). OS with more end-users are naturally more attractive to app developers than OS with fewer end-users. Developers thus tend to prioritise the largest OS (an example of indirect network effects). Over time, the gap in what larger and smaller OS can offer grows. The large OS gather more user data which helps them improve the quality of their recommendations. The small OS become even less attractive, until they go bust and the winners take all. One of the reasons Microsoft abandoned the mobile market in 2017 is that it could not attract enough app makers to its OS.

Masses of data, cheap machine learning technologies and the refining of ecosystem business models have further entrenched leading positions, conferring incredible bargaining power to set commercial conditions and terms unilaterally (eg to expel, charge high fees, manipulate rankings and control reputations). Such power leaves platform users vulnerable to abuse.

Online gatekeepers are a source of concern

Success is by no means illegal. But practices that lock it in might well become unlawful. The DMA would constrain gatekeepers’ behaviour while forcing them to proactively open up to more competition. Those in breach of the rules face penalties of up to 10% of their yearly turnover and repeat offenders face being broken-up. The DMA addresses two problems: high barriers to entry and anticompetitive practices by gatekeepers. The objective is to make digital markets both contestable and fair for existing and future rivals.

To illustrate, consider the DMA’s prohibition on combining end-user data from different sources without consent. Combining data from multiple sources can give gatekeepers a significant advantage over smaller rivals. Indeed, data gleaned from one source, say online searches, can be used to predict users’ preferences in other market, say music streaming. A gatekeeper that knows the web browsing history of a user is much better positioned to predict her musical tastes than a data-poor rival. Restricting the combination of data from multiple sources, therefore, restricts the ability of gatekeepers to leverage their market power from one market to another to the detriment of small players.

Other prominent rules include:

- No self-preferencing: a prohibition on ranking their own products over others;

- Data portability: an obligation to facilitate the portability of continuous and real-time data;

- No ‘spying’: a prohibition on gatekeepers on using the data of their business users to compete with them;

- Interoperability of ancillary services: an obligation to allow third-party ancillary service providers (eg payment providers) to run on their platforms;

- Open software: an obligation to permit third-party app stores and software to operate on their OS.

The proposal also includes a requirement that gatekeepers inform the regulator of all mergers and acquisitions, even when the target is too small to be subject to merger control. It does not include any powers to intervene to block these mergers however (unlike the equivalent UK proposal).

As with the definition of ‘gatekeeper’, the DMA’s list of obligations is a balancing act between enforceability and flexibility. Indeed, while seven rules apply equally to all gatekeepers, the majority (eleven rules) will be tailored to each.

The practical consequences of unconstrained power

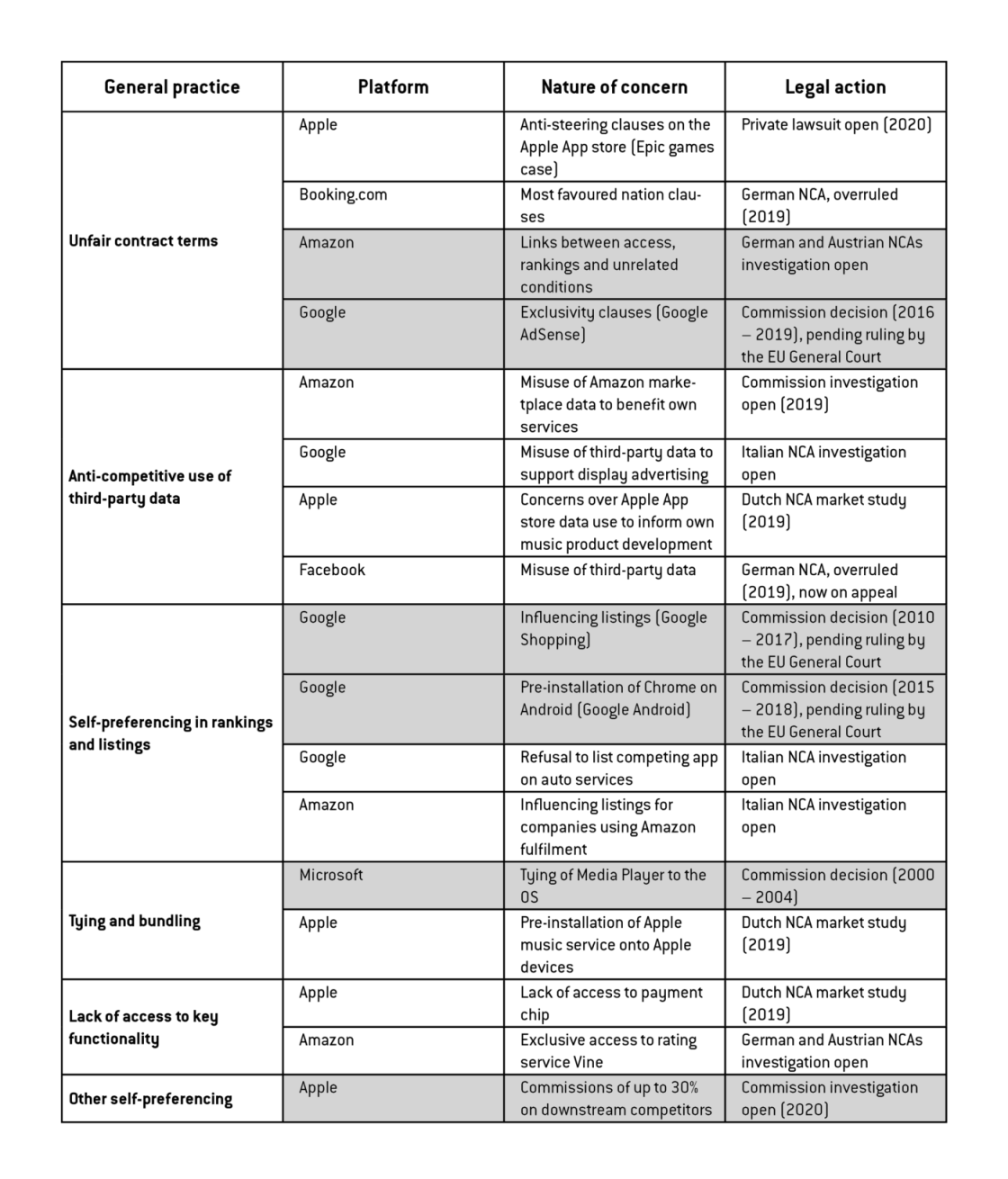

In the last few years, numerous studies (twenty-two of which are summarised here) and antitrust investigations have suggested that some gatekeepers adopted questionable practices from a competition standpoint (Table 1).

In setting the DMA list of obligations, the Commission drew on the knowledge it acquired through the various antitrust investigations: the DMA rulebook targets most of the unfair practices listed in Table 1. Take the Amazon case for example. The Commission suspects the e-retailer of gathering data on the activities of third-party sellers in order to outcompete them. One DMA obligation – for gatekeepers not to use the data of business users to compete with them – would clearly addresses the problematic practice.

Table 1: Alleged unfair practices by large digital platforms investigated by EU or national competition authorities (NCA)

Source: Bruegel based on European Commission’s DMA Impact Assessment (2020). Note: Cases investigated by the European Commission are highlighted in grey.

Stepping-up with ex-ante regulation

The DMA takes a diametrically opposite approach to antitrust enforcement (which is currently the United States’ favoured approach). It is an ex-ante set of rules that constrains operators before any bad behaviour can materialise, as opposed to antitrust which kicks in after an infringement (ex-post).

Antitrust (ex-post) enforcement has a number of advantages: by proceeding on a case-by-case basis it can be applied to a variety of business models, avoiding the imprecision of regulation. However examples like the Google shopping case, now in its tenth year, show that this approach isn’t fit for digital markets. Google's business model has changed considerably over the past decade, aside from the fact that for the competitors hurt by Google’s conduct in 2010, the damage has been done. In fast-moving markets prone to tipping, ten years is a lifetime. On average, successful start-ups that reach a valuation of $1 billion do so in one year less than it takes the Commission to run an investigation into large digital platforms (Figure 1).

The analytical pillars of antitrust cases are: market definition (eg the market for music streaming) and assessment of market dominance (ie how much power the investigated firm has in said market). As highlighted in the DMA’s impact assessment, both are notoriously difficult to establish in multisided digital markets: what may amount to a market on one side of the platform (eg the side of music streamers) may not clearly extend as a market on the other (eg the side of music publishers). The fact that many digital goods are provided for free also challenges traditional methods for assessing market power. The EU’s competition authority’s resources are already stretched: this can only exacerbate the great asymmetries in technology and knowledge between the authorities and market players.

Even if competition enforcement could somehow be sped up in digital cases, it would fail to adequately address the systemic failures that stem from the behaviour of digital users, for example the tendency to stick to the default option. Online platforms have developed sophisticated tools to monitor users’ behaviour in real-time and are uniquely positioned to leverage behavioural biases to solidify their market positions. Consider, for instance, that on a smartphone where Google is the default search browser, 97% of searches are made on Google versus 86% on desktops where Bing is the default, according to a CMA report. Forcing one platform to change its default setting will do little to prevent every other digital player from doing the same.

Regulation can address some of these limitations: by setting out clear rules from the outset, regulators would be empowered to act quickly when these rules are violated. The creation of a digital market centre of knowledge and expertise would ensure speedy detection. Regulation is also more far-reaching: it concerns all gatekeepers, all of the time.

True, regulation is more prone to capture by industry than competition policy. Over-enforcement is also a concern as rules could fail to account for consumer benefits from seemingly anti-competitive behaviour. In a very dynamic environment, regulation can be rendered useless.

These are risks EU policymakers are willing to take after what they have judged to be years of underenforcement. And the proposed DMA offers more flexibility than the stereotypically-rigid regulatory approach. As described above, the terms of the DMA would evolve alongside markets and adapt to individual business models. More fundamentally, the aim of the DMA is to protect the competitive process, not to prescribe specific outcomes. The Commission does not propose to regulate big tech as natural monopolists, but rather to make sure it never has to.

Recommended citation:

Anderson, J. and M. Mariniello (2021) ‘Regulating big tech: the Digital Markets Act’, Bruegel Blog, 16 February

About the authors

Related content

Which platforms will be caught by the Digital Markets Act? The ‘gatekeeper’ dilemma

The scope of the Digital Markets Act has emerged as one of the most contentious issues in the regulatory discussion. Here, we assess which companies c

An inclusive European Union must boost gig workers’ rights

A European initiative strengthening rights for gig workers is welcome. A digitised economy should also be inclusive.

Biometric technologies at work: a proposed use-based taxonomy

We define biometric technologies as AI technologies that rely on biometric data to derive inferences about the individual whose data is collected.

For remote work to work, new ground rules are needed

The pandemic has shown workers and employers that another way to work is possible. The European Union should develop a framework to facilitate hybrid