Relocating production from China to Central Europe? Not so fast!

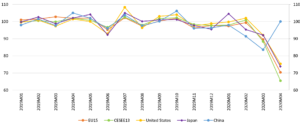

Western European imports from central Europe have fallen dramatically, while imports from China fell much less, and had already recovered to pre-COVID

This article originally appeared in Eastern Focus.

The COVID crisis caused a major setback to global trade and disrupted the functioning of global production networks. From the perspective of Central, Eastern and South Eastern European (CESEE) countries, this has raised the hope that Western European manufacturers will bring their suppliers from East Asia closer, potentially boosting investment in CESEE.

The volume of merchandise trade is expected to drop by almost 20% in the second quarter of 2020 compared to the same quarter of the previous year, the steepest decline on record according to the World Trade Organisation. Almost half of global trade is composed of intermediate goods for production, and there were companies in Europe and elsewhere which did not receive essential intermediate inputs for production during the height of the COVID crisis. Such disruptions to global trade and global production networks, or global value chains (GVCs), can call the benefits of globalisation into question, and might prompt companies to bring their suppliers closer. For Western European producers, the CESEE region would be a natural place to relocate their suppliers due to its geographical closeness. Relocation would boost investment in CESEE, which in turn could speed up the recovery from the corona-recession and support medium-term growth and jobs.

Foreign trade facts disappoint relocation hopes

However, recent trade data paint a sobering picture of such hopes: the imports of the first fifteen European Union member countries (EU15) declined the most from the CESEE region, while imports from China had reverted back to their 2019 level by April 2020, the latest available data at the time of writing (Figure 1). Imports from CESEE declined by a shocking 35%, while within the EU15 imports (such as German import from France and French import from Germany) declined by 30% on average by April. EU15 imports from the United States and Japan declined by about a quarter. The decline of EU15 imports from China had already started in February 2020, earlier than from the rest of the world, given that COVID-19 hit China first. Yet even at the lowest point in March 2020, the EU15’s imports from China was ‘just’ 16% lower than on average in 2019, while in April 2020 it had returned to the same level as in 2019.

Figure 1: EU15 imports from different regions, euro billions at current prices, seasonally adjusted, 2019 average = 100

Source: author’s calculation, using bilateral trade data from the IMF’s Direction of Trade Statistics dataset (accessed on 6 August 2020), which includes US dollar values. Average euro/US dollar exchange rates from Eurostat were used to convert USD figures to euros. The euro values were seasonally adjusted using the X12 method.

Note: EU15: first 15 members of the European Union. CESEE13: the 13 countries that joined the EU in 2004-2013.

Among the 13 CESEE countries, Slovakia was hit the hardest by its exports to the EU15 almost halving. Romania was the second hardest hit, followed by Hungary and the Czech Republic with about 40% export losses. At the other end, Estonia, Latvia and Lithuania suffered from ‘just’ about 15% trade losses.

The composition of EU imports from China shows that some product categories saw major increases, while others declined; however, several intermediate goods categories gained or did not suffer much from April 2019 to April 2020. The highest increases in April 2020 compared with the same month last year were recorded for automatic data processing machines (+€884 million, +33%), articles of apparel of textile fabrics (+€129 million, +36%) and electronic tubes, valves and related articles (+€92 million, +12%). (Textile articles include COVID-19 related products, such as textile face masks, surgical masks, disposable face masks and single use drapes). The largest decreases in absolute terms were observed for imports of footwear (-€254 million, -52%), telecommunications equipment (-€232 million, -6%) and baby carriages, toys, games and sporting goods (-€225 million, -28%). Other intermediate production inputs such as pumps, compressors, fans, electric power machinery and parts, motor vehicle parts fell less.

What can we make of these developments?

First, the limited fall and the quick rebound of EU15 imports from China is really remarkable, given that the economic activity and total imports of the EU15 was much lower in April 2020 than on average in 2019. Perhaps imports from China in April 2020 partially replaced imports from other countries suffering from COVID-related lockdowns. The rebound of imports from China suggests that East Asian supplier problems were short-lived; and from the perspective of disrupted supply chains, there is not much justification to relocate suppliers from East Asia to Europe. The adverse public health situation due to COVID-19 was addressed quickly in China, allowing suspended production and shipments to restart – and faster than in Europe. Such rapid control of the epidemic in China might even reinforce the reliability of Chinese suppliers.

Second, while the CESEE countries are geographically close to consumer markets in the EU, they are still very far away for the value chains of some goods that are produced in China. For instance in ICT goods, the value chain is predominantly East Asian, so moving certain intermediate inputs from China to Europe would mean getting closer to the consumer but farther away from other suppliers. Replicating whole value chains in Europe seems to be a difficult and costly task.

Third, the lower decline of EU15 imports from the United States and Japan than from CESEE suggests that distance to Western Europe is not the primary determinant of trade flows, even in times of lockdowns and trade disruptions. The product composition of trade seems to be a more important factor. This again highlights that the geographic proximity of CESEE to Western Europe should not be overrated.

Fourth, the extent of trade losses depends on the sectoral and product composition of exports to EU15, including the mix of intermediate and final products. It seems that CESEE countries which are more integrated into Western European production networks, such as Slovakia, Romania and Hungary, suffered from larger declines in exports. Since the bulk of exports includes manufacturing products, export decline should coincide with industrial production decline. Indeed, industrial production fell the most (by about one third) from May 2019 to May 2020 in Slovakia, Hungary and Romania among EU member states, according to Eurostat. This suggests that greater participation in European value chains exposes an economy to greater variation in production, with associated consequences for employment and GDP growth.

Fifth, as industrial production recovers, so does trade. Eurostat data shows that industrial production started to recover from April to May 2020 since lockdowns were eased, and is expected to recover further in subsequent months. At the time of writing, the latest bilateral foreign trade data available is for April 2020. Hence the large drop in intra-EU trade by April is expected to correct itself, at least to some extent, over the coming months. It will be interesting to analyse whether intra-EU trade will recover as fast as EU15 imports from China, or whether it does so at a slower pace.

And sixth, GVC-related trade also suffered much more in the aftermath of the 2008 global financial crisis than traditional trade, but it also recovered faster after 2009 (see Figure 1 here).

Thus, greater participation in GVCs exposes trade and production to greater variation, which can have adverse consequences for output, employment, government budget balances and many other indicators in times of economic shocks. Such adverse variation should certainly make CESEE policymakers think about their industrial policy strategies, although shorter-run (or cyclical risks) and longer-run structural impacts should also be jointly analysed.

Global value chain participation has longer-term benefits

Participation in GVCs has a number of longer-term benefits. As Richard Baldwin argues, emerging and developing countries with less developed industrial structures and smaller domestic markets can join the supply chains of firms from high-tech nations, instead of building such supply chains as Korea and Taiwan had to do over a long period of time, since these countries developed themselves before the GVC era. Joining GVCs since the mid-1980s has allowed less developed countries to embark on a faster-track development, specialising in certain tasks.

A recent IMF study concludes that it is GVC-related trade, rather than conventional trade, which has a positive impact on income per capita and productivity, even though such gains appear more significant for upper-middle and high-income countries.

Such longer-term benefits have likely induced CESEE governments to attract as much foreign direct investment (FDI) as they can by offering the maximum amount of state aid which is possible in the EU, such as tax exemption for a decade, or financial support to train employees and reduce labour costs. FDI can foster participation in GVCs by local suppliers. The recent races between CESEE countries to attract prominent foreign manufacturers seem to suggests that this development strategy is set to continue.

Most CEESEs have not moved up in the value chain

An important aspect of development is whether companies participating in GVCs gradually move up in the value chain: that is, whether the initial contributions to low-wage sectors are gradually replaced by higher value-added and higher technological-level production. The IMF study mentioned above finds an unfavourable results for most CESEE countries, by analysing Germany’s auto supply chain: for the Czech Republic, Hungary, Poland, and Slovakia, the contributions of high and low technological-level sectors remained broadly the same between 2000 and 2013, suggesting there had been no moving up on the value chain. For Romania, in contrast, there has been a shift away from low-tech to more high-tech manufacturing. As regards non-EU countries, the study finds that China’s contribution to the German auto supply chain is showing a shift towards more high-tech services, while Russia’s contribution became more intensive in low-tech manufacturing due to the mining and quarrying sector.

Related indicators suggest similarly unsatisfactory progress for most CESEE countries. The European Union’s innovation scoreboard, which is measured using 27 performance indicators distinguishing between ten innovation dimensions in four main categories, concludes that with the sole exception of Estonia, CESEE countries rank well below the EU average in 2019. Moreover, the improvement in innovation performance from 2012 to 2019 in the Czech Republic, Hungary, Bulgaria and Slovakia was below the average improvement in the EU, and there was even a setback in innovation performance in Romania and Slovenia. CESEE countries do not rank highly in the World Economic Forum’s Innovation capability component of the Global Competitiveness Index either. Slovenia (28th), the Czech Republic (29th) and Estonia (34th) have the highest rankings in the CESEE out of 155 countries, while the lowest rankings in the CESEE region belong to Latvia (54th), Romania (55th) and Croatia (73rd).

Overall, it seems that while participation in global value chains has brought major benefits to CESEE countries in terms of growth and jobs, it has not been associated with improved technological and innovation capabilities. This is a key problem, because with continuing fast wage growth and a deteriorating demographic outlook, the region’s advantage as a low-wage supplier of western European manufacturing networks is gradually diminishing. Most CESEE countries rank disappointingly in the World Economic Forum’s Skills ranking, which considers various indicators related to the current and future workforce, suggesting that the workforce is not up to the challenge of moving away from low-wage activities.

Sustained convergence requires transition towards knowledge-intensive economic activities

Sustained convergence toward western European productivity and living standards will be possible by moving up the value chain towards more knowledge-intensive activities. This, first and foremost, requires better education and research, which in turn necessitates higher public spending.

For example, public expenditure on tertiary education is below 1% of gross national income in most CESEE countries, but around 1.5% or more in most northern and western European countries. In a forthcoming study we find a statistically significant correlation between public spending on universities and a number of educational result indicators. Primary and secondary education are equally important. As James Heckman argues, in disadvantaged families the highest rate of return in early childhood development comes from investing as early as possible, because skills beget skills in a complementary and dynamic way. There are many poor and disadvantaged families in CESEE. Secondary education, vocational training and lifelong learning are similarly crucial.

Given the relatively low public debts of CESEE countries and their prospectively faster economic growth than in Western Europe (which will help their fiscal sustainability), it is surprising that these countries do not devote more resources to education and research.

The COVID-19 economic shock and the associated collapse in trade should serve as a wake-up call for policymakers in CESEE countries. The existing economic model, which has fostered as much foreign direct investment as possible as well as greater participation in global value chains, has served its purpose, but it will soon run its course. Even a short-term boost cannot be expected from a hypothesised strategic reorganisation of suppliers from East Asia to CESEE. Instead, policies fostering upward movements on the values chain should be significantly stimulated.

Related content

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

Zooming in US-China tech rivalry

A comparative exploration of US-China innovation frontiers

China’s ‘new productive forces’ risk overcapacity bubble