Recent euro-area house price increases are dissimilar to earlier housing booms

Current housing markets relative to those pre-crisis seem to be far less driven by mortgage credit, and the size of the construction sector has not in

Rapid house price increases are good for homeowners and bad for people wishing to buy. They could also be bad for the economy as a whole if there are rapid house price corrections which typically lead to severe social and economic problems.

Notable examples of housing bubbles in recent European history are the pre-2008 developments in Ireland and Spain. In both countries, the euphoria and the low-interest rates caused by the introduction of the euro in 1999 led to rapid growth in mortgage credit, which in turn boosted house prices and a further expansion of credit. During credit booms, the risks generally rise because banks become willing to lend to less creditworthy customers.

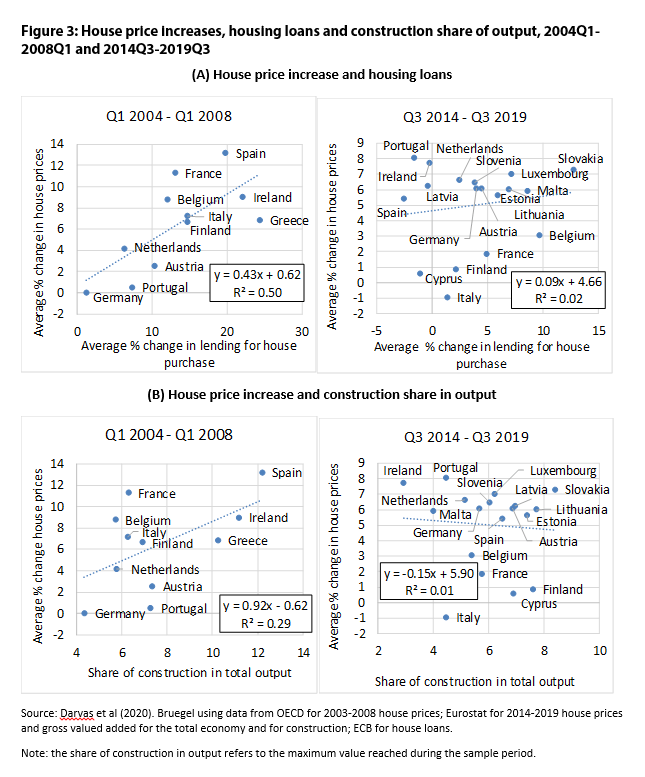

However, not all rapid house price increases turn out to lead to rapid price corrections. Figure 1 shows that pre-crisis house price growth was similar in France than in Ireland and Spain. Yet while Irish house prices collapsed from their peak pre-crisis values by 54% and Spanish prices fell by 36%, the decline in French housing prices was modest, at 9%, and short-lived.

There were two main differences between France and the other two countries. First, in Ireland and Spain rapid increase in credit was the main engine of house price growth. The second is that in Ireland and Spain more and more economic resources were diverted to the construction sector (Figure 2). In Ireland, the share of construction in total output almost doubled from 6% to 11%, while in Spain construction’s share increased from 9% to 12%. In contrast, in France, the construction share hardly increased, from 5% to 6%.

The large pre-crisis increases in construction’s share of output in Ireland and Spain also resulted in a large increase in the employment share of this sector, as well as a growing number of suppliers from other industries that made their fortunes from this sector. Tax revenues from the construction sector and associated industries became sizeable in Ireland and Spain.

Back then, when the house price boomed turned to a bust, fortunes changes, financial institutions ran into crisis and many jobs were lost. Major fiscal problems ensued, due to loss of tax revenues from construction-related activities and more spending on unemployment and bank rescue. But do current property price increases predict a similar fate? Will we see more major defaults on mortgages and mass unemployment in the construction sector?

House prices increased in the euro area in the past five years. But there are two major reasons why we think it is unlikely that the 2008/10 bust will be repeated and why we think the consequences of house price corrections will be more benign.

First, before 2008 credit growth and house-price increases were highly correlated as credit growth fuelled house-price growth and vice versa. But this has not been the case in the past five years. Certainly, there were and are some exceptions, such as in France in the pre-crisis period, where house prices increased very rapidly but credit growth was limited, as we have already highlighted above. Slovakia is an exception in the past five years since fast house-price increases there have coincided with rapid credit growth (even as the ECB’s latest Financial Stability Review does not consider the Slovakian residential real estate market to be overvalued). But the big picture in most euro-area countries remains that the correlation between mortgage credit growth and house-price increases in the past five years is modest. This is good news for financial stability as an eventual house-price correction will affect fewer borrowers and lead to fewer mortgage defaults and less impact bank profitability less.

Second, in the past five years, construction has not expanded much even in those countries that are experiencing relatively fast house prices increases. An eventual housing bust would, therefore, be less disruptive than it was in Greece, Ireland and Spain after 2008 as less employment and economic activity will be at stage.

A final point relates to different macro-prudential measures introduced after the crisis. These can be helpful but in our paper, we also argue that their use looks quite unsystematic across countries of the EU.

To sum up, from a financial stability perspective vigilance about house prices increases is needed especially in those countries, such as Slovakia, that simultaneously face a rapid credit growth. But in most of the euro area, the risks in the housing market should be more nuanced, because current housing markets, relative to those pre-crisis, seem to be far less driven by mortgage credit, and the size of the construction sector has not increased.

About the authors

Related content

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up

Climate change, the next big financial threat

A warming planet poses new risks to European sovereign debt. How can the continent protect itself?

Next steps for the European Anti-Money Laundering Authority

At this invitation-only event Raluca Pruna discussed the state of the legislation to create an EU Anti-Money Laundering Authority