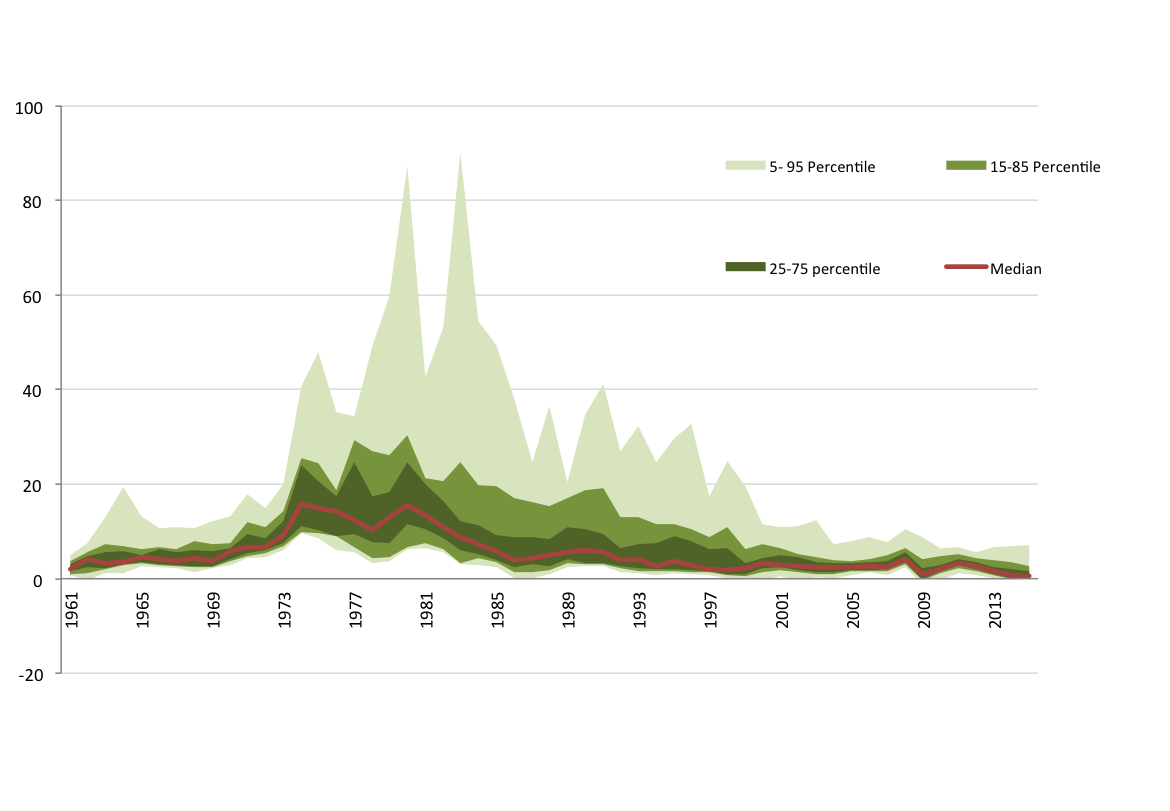

After soaring in the 1970s, inflation rates in advanced countries have declined significantly since the early 1980s, stabilized around 2% in the years before the global financial crisis, and are today at very low levels (see Figure 1). This movement coincided with the acceleration of globalisation, triggering a debate on whether globalisation could be one of the main drivers of the disinflation process, and whether the ability of central banks to control inflation could be undermined as a result.

Figure 1: Headline inflation percentile distributionacross the world

Notes: distribution of year-on-year inflation across an unbalanced panel of 50 countries.

Source: OECD Economic Outlook and Bruegel calculations.

In a recently published paper, we reviewed the potential effects of global integration on inflation dynamics, and discussed whether this could affect the ability of central banks to fulfil their mandates.

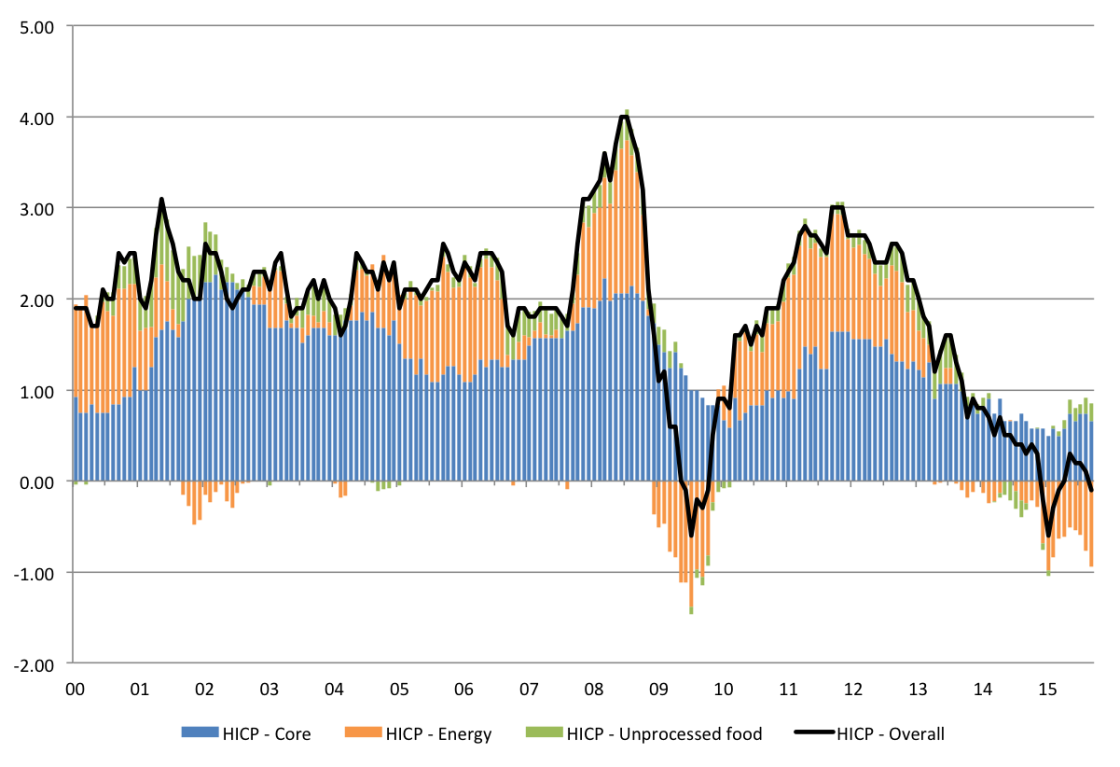

The recent acceleration in globalisation has mainly taken three forms that could affect inflation dynamics and monetary policy: trade integration, labour market integration and financial integration. Openness in terms of trade has led to a greater sensitivity of domestic price levels to external price shocks. Fluctuations in global prices can indeed have major temporary effects on domestic prices: as can be seen in Figure 2, energy prices are one of the major determinants of the short-term fluctuations of the euro-area headline inflation. More importantly, trade with low-cost countries has increased massively in the last two decades, which has logically resulted in a reduction in the price of imported goods. Global competition between firms might have also reduced the pricing power of domestic companies, while the integration of billions of workers into the global labour market has likely reduced the bargaining power of domestic workers. Overall, the empirical literature – Pain, Koske and Sollie (2006) – shows that the contribution of globalisation to the global disinflation movement since the 1990s has been positive, but rather limited for the moment.

Figure 2: Headline, core, energy and food inflation, Euro area (%)

Source: Eurostat.

A more important question in our view is whether these integration trends affect the transmission mechanisms of monetary policy and reduce the ability of central banks to fulfil their mandate. The transmission channels of monetary policy could potentially be affected at various levels. First, central banks could lose their ability to control inflation if inflation becomes a function of global slack instead of being a function of domestic slack. Second, central banks could lose control of short-term rates if rates become a function of global liquidity instead of the liquidity provided by the domestic central bank. And third, central banks could lose their hold over domestic inflation and economic activity if long-term interest rates depend only on the balance between savings and investment at the global level, and not at the domestic level.

It is true that the negative relationship between domestic slack and domestic inflation has changed and that that the slope of the so-called Phillips curve has flattened since the mid 1980s. In other words, the rate of unemployment triggering wage increases and inflation is lower today than in the past. However, empirical studies – Ihrig et al (2007) and Ball (2006) – have failed to demonstrate that globalisation had been one of the main drivers behind this trend. A more plausible explanation seems to lie in the monetary policy changes that have taken place since the mid 1980s, with the adoption of credible inflation-targeting regimes in many advanced countries. These policies, combined with the move away from indexation of wages, have made external price shocks much less persistent than in the 1970s thanks to the absence of the second-round effects. Indeed, figure 2 suggests a low pass-through of recent external price shocks (e.g. from oil prices) from the headline inflation rate to the core measure.

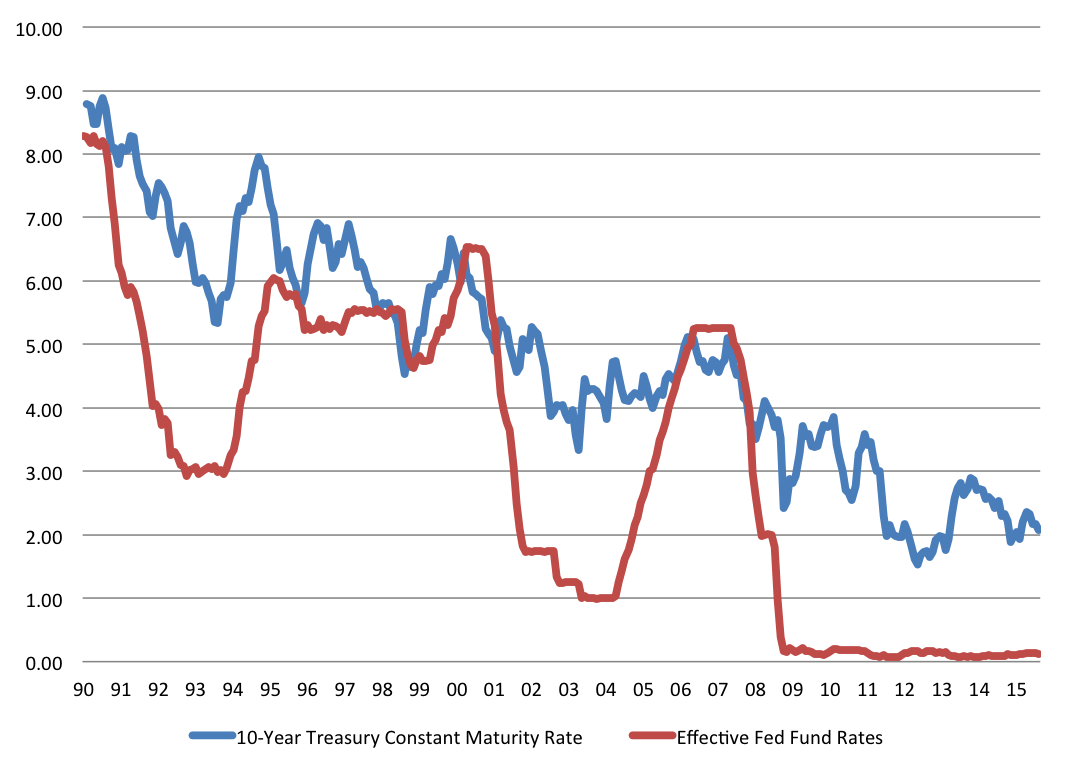

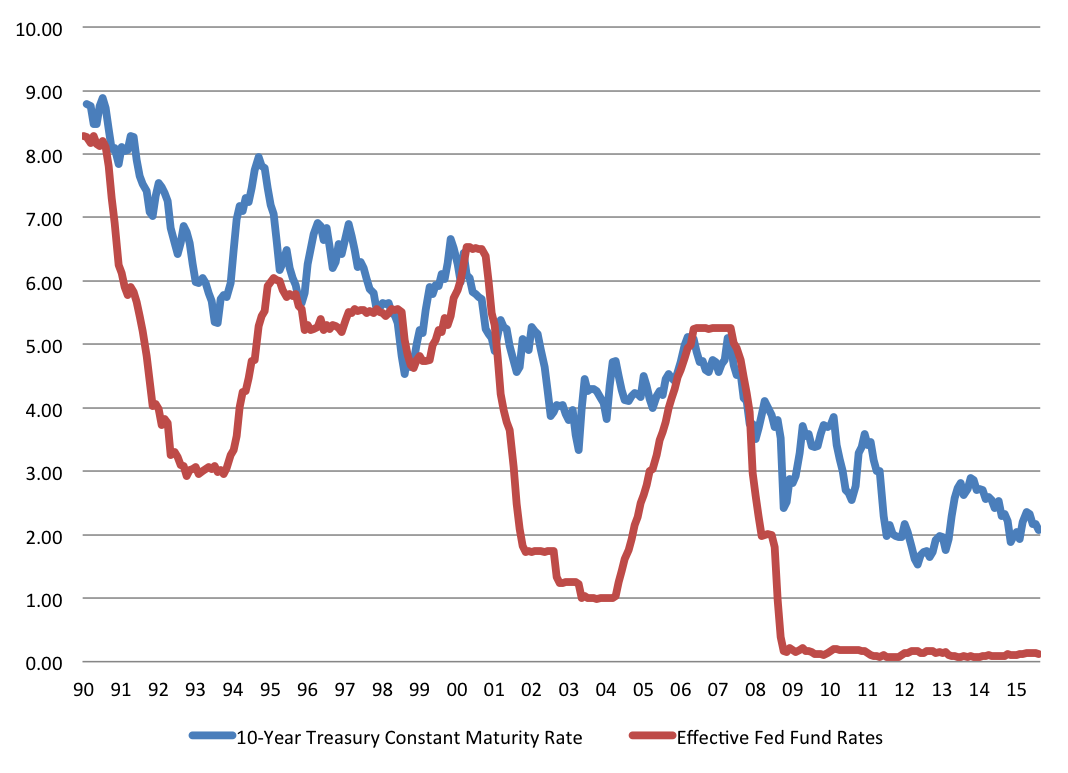

Concerning the control of central banks over the domestic yield curve, it is clear that as long as central banks retain some kind of domestic monopoly over the issuance of base money, they will be able to control the shorter end of the domestic yield curve. For long-term rates, this is less clear, however. The conundrum episode of 2004-06 in the US (see Figure 3) suggests that long-term rates can become less sensitive to short-term rates and that external factors can affect them significantly. Since the beginning of the crisis, central banks also showed that they were willing to use less conventional monetary tools in order to influence the whole yield curve, in particular when they are constrained at the short end of the curve by the zero lower bound.

Figure 3: US short and long term interest rates

Source: FRED (Saint Louis Fed)

In any case, even if financial integration could result in a reduction of the role of the long-term interest rate channel, for countries accepting flexible rates globalisation should at the same time increase the role of the exchange rate as a transmission mechanism. Indeed, the disappearance of capital controls and the reduction in the portfolio home bias in many advanced countries mean that financial markets are much more integrated than a few decades ago and that the demand for domestic and foreign assets is more sensitive to differences in interest rates, thus enhancing the influence of monetary policy on the exchange rate.

Given the potentially greater effects of external price shocks on more open economies and the potential alteration of monetary policy transmission channels in more integrated financial markets, globalisation forces central banks to take external developments into account in their monetary policy decisions. In particular, central banks need to have a medium-term policy goal orientation instead of trying to manage yearly inflation rates that are driven by global shocks. Overall, we think that, as long as they adopt flexible exchange rates, central banks retain their ability to stabilise inflation at the targeted level in the medium term, even though globalisation does not facilitate their task, which is already quite difficult because of the zero lower bound.

Guntram Wolff is a Senior fellow at Bruegel. He is also a Professor of Public Policy and Economics at the Willy Brandt School of Public Policy. From 2022-2024, he was the Director and CEO of the German Council on Foreign Relations (DGAP) and from 2013-22 the director of Bruegel. Over his career, he has contributed to research on European political economy, climate policy, geoeconomics, macroeconomics and foreign affairs. His work was published in academic journals such as Nature, Science, Research Policy, Energy Policy, Climate Policy, Journal of European Public Policy, Journal of Banking and Finance. His co-authored book “The macroeconomics of decarbonization” is published in Cambridge University Press.

An experienced public adviser, he has been testifying twice a year since 2013 to the informal European finance ministers’ and central bank governors’ ECOFIN Council meeting on a large variety of topics. He also regularly testifies to the European Parliament, the Bundestag and speaks to corporate boards. In 2020, Business Insider ranked him one of the 28 most influential “power players” in Europe. From 2012-16, he was a member of the French prime minister’s Conseil d’Analyse Economique. In 2018, then IMF managing director Christine Lagarde appointed him to the external advisory group on surveillance to review the Fund’s priorities. In 2021, he was appointed member and co-director to the G20 High level independent panel on pandemic prevention, preparedness and response under the co-chairs Tharman Shanmugaratnam, Lawrence H. Summers and Ngozi Okonjo-Iweala. From 2013-22, he was an advisor to the Mastercard Centre for Inclusive Growth. He is a member of the Bulgarian Council of Economic Analysis, the European Council on Foreign Affairs and advisory board of Elcano.

Guntram joined Bruegel from the European Commission, where he worked on the macroeconomics of the euro area and the reform of euro area governance. Prior to joining the Commission, he worked in the research department at the Bundesbank, which he joined after completing his PhD in economics at the University of Bonn. He also worked as an external adviser to the International Monetary Fund. He is fluent in German, English, and French. His work is regularly published and cited in leading media.

Grégory Claeys, a French and Spanish citizen, joined Bruegel as a research fellow in February 2014, before being appointed senior fellow in April 2020.

Grégory Claeys is currently on leave for public service, serving as Director of the Economics Department of France Stratégie, the think tank and policy planning institution of the French government, since November 2023.

Grégory’s research interests include international macroeconomics and finance, central banking and European governance. From 2006 to 2009 Grégory worked as a macroeconomist in the Economic Research Department of the French bank Crédit Agricole. Prior to joining Bruegel he also conducted research in several capacities, including as a visiting researcher in the Financial Research Department of the Central Bank of Chile in Santiago, and in the Economic Department of the French Embassy in Chicago. Grégory is also an Associate Professor at the Conservatoire National des Arts et Métiers in Paris where he is teaching macroeconomics in the Master of Finance. He previously taught undergraduate macroeconomics at Sciences Po in Paris.

He holds a PhD in Economics from the European University Institute (Florence), an MSc in economics from Paris X University and an MSc in management from HEC (Paris).

{kind=link}

{kind=link}