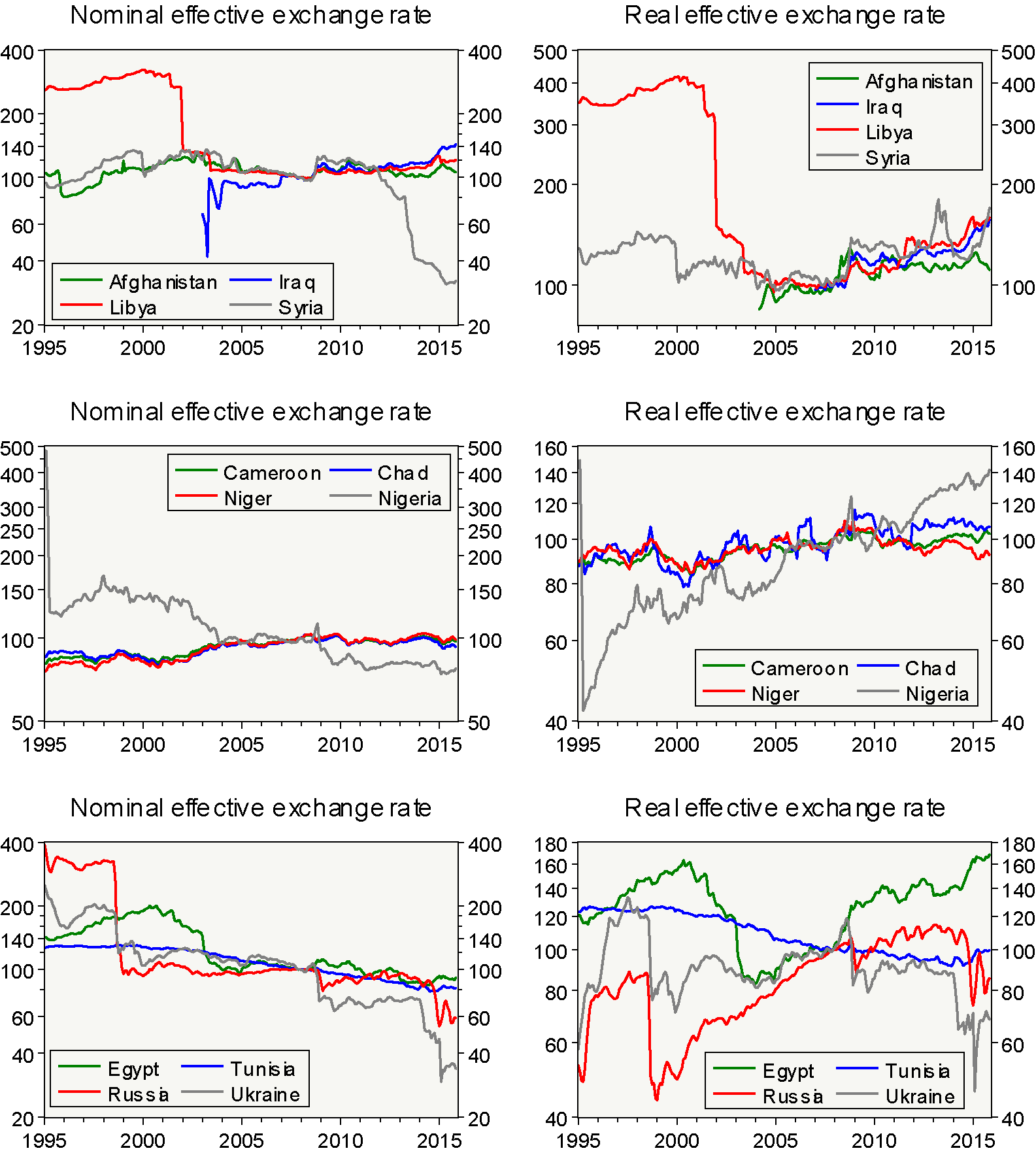

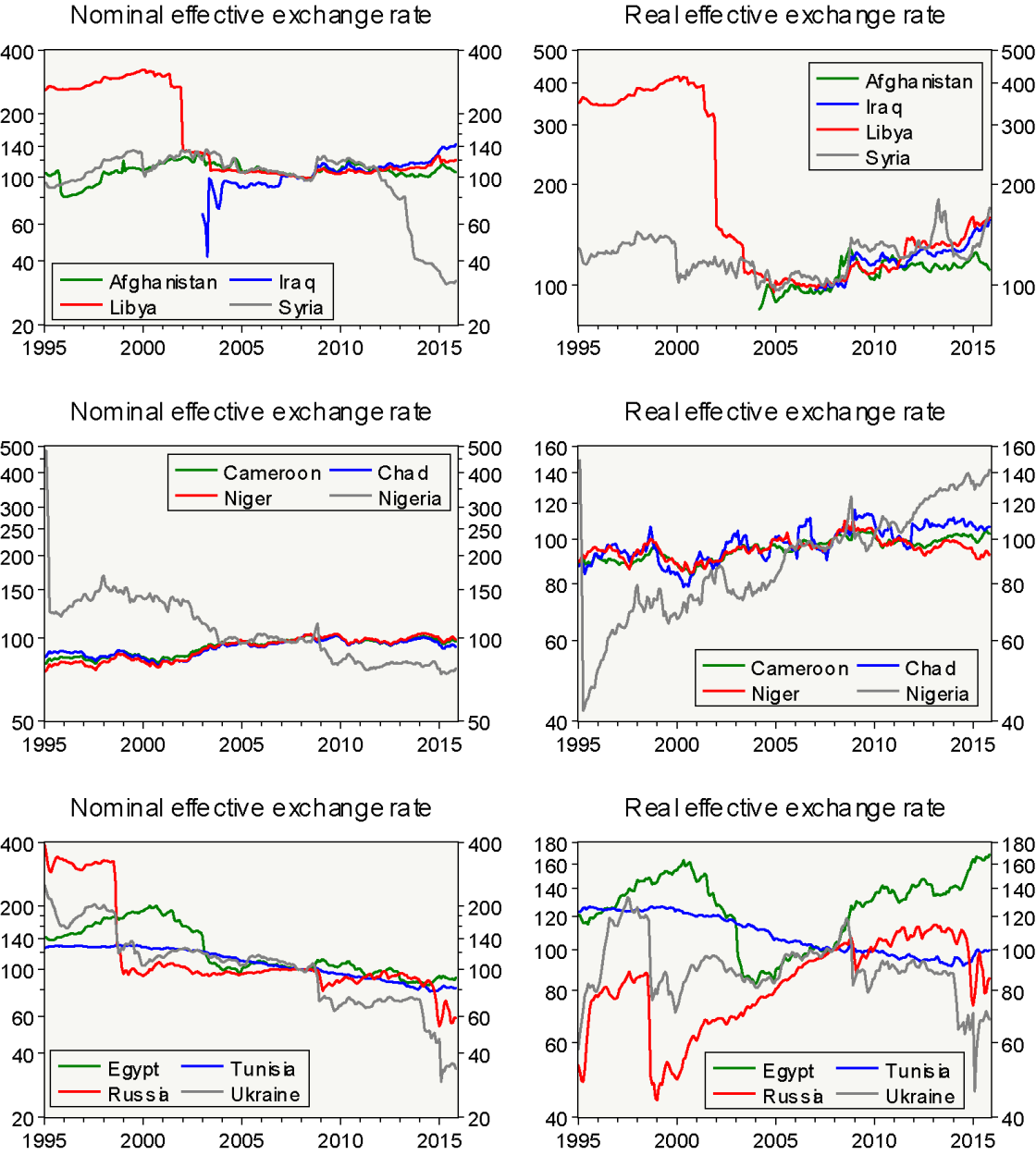

Real exchange rates in conflict zones

Several countries experiencing conflict have been able to maintain a stable nominal exchange rate and thereby their real exchange rates were either st

We have updated our monthly real effective exchange rate dataset up to November 2015. We have also added some new countries, including various countries experiencing conflict. I therefore thought it would be interesting to post a chart showing the evolution of nominal and real effective exchange rates in a selection of countries experiencing conflict.

Some of these countries were able to maintain a relatively stable nominal effective exchange rate, supported by tight capital control measures, as indicated by the index of Menzie Chinn and Hiro Ito *. As a consequence, real effective exchange rates were primarily driven by the inflation differential with respect to trading partners. In several of these conflict-ridden countries the real effective exchange rate remained broadly stable or even appreciated.

Among the twelve countries included on the chart, only Syria, Russia and Ukraine have recently experienced major nominal currency depreciations.

In Syria, high recent high inflation has even led to a real appreciation of the Syrian Pound, despite the fall in the nominal value of the currency. (Note that the latest Syrian inflation data is for May 2015 as reported here. For calculating the real exchange rate until November, we assumed that the 12-month inflation rate remained unchanged in June-November 2015. Therefore, our Syrian real exchange rate data for June-November 2015 is preliminary.)

High inflation also counteracted some of the impacts of nominal depreciation on the real exchange rate in Russia and Ukraine. In fact, while the current Russian real exchange rate is well below its 2013 value, it does not differ much from the historical average of the past two decades. In Ukraine, on the other hand, the current real rate is well below its historical average.

* According to the Chinn-Ito index, only Russia had a reasonable degree of financial openness among the 12 countries in 2013 (the latest available data). Egypt was even more open financially in most of the 2000s, but major restrictions were introduced from 2008-2013.

Nominal and real effective exchange rate (December 2007=100), January 1995 – November 2015

{kind=link}

Source: Bruegel dataset

.

About the authors

Related content

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

The EU needs a methodology for including reform impacts in fiscal trajectories

Such a methodology, and a governance mechanism for managing associated risks, must be in place before the new fiscal framework kickstarts in September

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition