Greece – the three essential elements for a deal

This blog argues that a deal for Greece requires three elements: lower primary surpluses than the creditors are currently asking for; little action on

This blog argues that a deal for Greece requires three elements: lower primary surpluses than the creditors are currently asking for; little action on debt except for agreeing to delay IMF repayment (similarly to how European Financial Stability Facility repayments have been delayed); and serious institutional reforms and trust building measures by the Greek government to re-establish confidence, Greece’s most scarce resource .

Stances on both sides in the Greek negotiations have hardened, and creditors and debtor still seem far away from each other. In this blog, I charter the three elements that are crucial for a deal. They concern the primary surplus, how to deal with the debt and, most importantly, confidence and trust in a monetary union.

First, on the fiscal target debate, the creditors are requesting a primary budget surplus (revenues less expenses without interest rate payments) of 1 % of GDP this year, 2 % next year, and 3 % in 2017, rising to 3.5% by 2018. Syriza, in contrast, is asking for a more modest adjustment of up to 0.75% this year, 1.75% in 2016 and 2.5% in 2017. Accumulating these fiscal paths over 2015-18, the difference between the two amounts to 1.0% more of GDP requested from the creditors. By any metrics, this difference is substantial regarding its impact on GDP, but rather irrelevant compared to the overall debt burden. In fact, the literature is rather clear that in a recessionary environment, a fiscal adjustment of 1% of GDP per year will lead to GDP losses of even more than 1%. After a decline in GDP of more than 25%, Greece has a point in calling for lower primary surpluses.

The second issue concerns the level of public debt. International commentators and academics (see here and here) have been calling for debt relief to Greece. A number of interrelated aspects need consideration in this regard.

Very high primary surpluses rarely occur for an extended period of time and come with high political and economic costs.

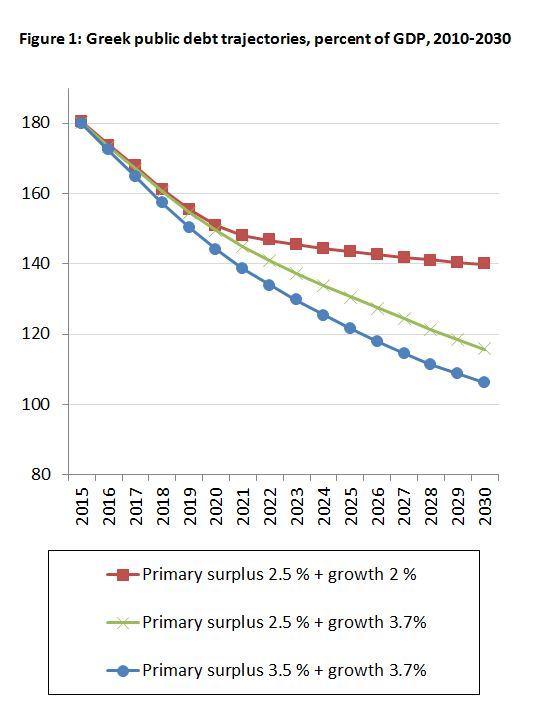

- Do high debt levels demand high primary surpluses, which in turn hurt growth and are politically unachievable? Syriza and the creditors seem to agree on a primary surplus of 3.5% from 2018 onwards. However, we know from Eichengreen and Panizzathat such high primary surpluses rarely occur for an extended period of time and come with high political and economic costs. Arguably, such high primary surpluses are not really necessary. Take for instance a significantly lower primary surplus of only 2.5% and different assumptions as regards inflation and growth (base scenario: 3.7% nominal growth, pessimistic scenario: 2% nominal growth, the average interest rate is set at 3.7% and derived from forward rates, for details see Darvas and Hüttl). Even in the pessimistic scenario that only assumes 2% nominal growth, the Greek debt to GDP ratio would still fall, although at a slower pace (see figure). A slower reduction in the debt to GDP ratio requires either access to the market so that Greece can pay its official creditors on time, or delayed re-payments of official creditor loans, which would de facto amount to some debt relief. Since Greece almost regained market access last year, arguably it will be able to start EU re-payments with access to markets as of 2020. And certainly, a debt-to-GDP ratio in 2030 of 115% could be compatible with market access just as well as a debt-to-GDP ratio of 105%.

Source: Bruegel calculations, for details, see Darvas and Hüttl (2014).

- The focus is often on headline debt-to-GDP numbers instead of on the actual burden of public debt on the Greek economy. One metric by which to measure the burden of debt on the economy is interest payments. In the period 2015-2020, Greece will not pay more than 2.6% of GDP in annual interest. In fact, the European official creditors have waived interest payments until 2020 and debt repayment is stretched over more than 30 years. As a consequence, the Greek interest burden is about the level of interest that France pays.

- Others, again, would argue that the empirical literature spearheaded by Reinhart and Rogoff shows that debt levels above 90% of GDP are negatively correlated with growth. This evidence was, however, prominently challenged by Thomas Herndon, Michael Ash, and Robert Pollin. Overall, it is not clear at what level debt has a strong negative impact on growth. Certainly, there is little evidence that a 10 or 20 percentage point difference of debt – as would be achieved by higher primary surpluses – would substantially change growth performance going forward.

- A corollary to the postponed debt repayment of Greece and the low interest burden is what economists call the low net present value of Greek debt. Hugo Dixon has proposed to make this more easily visible with some financial engineering. Such ideas are worth exploring further, but they certainly require Greece to re-gain market access, a point I will discuss below.

- The final, and perhaps most contentious issue concerns the repayment schedule of the IMF. The Eurogroup already made substantial concessions back in November 2012 , by agreeing to extend the maturities of EFSF and bilateral loans by 15 years (and repayments will only start in 2023). The IMF, in contrast, has until now refused to ease Greece’s debt burden. A logical step would be to ask the IMF to change strategy. It has still 30 billion euros at stake, all of which should be repaid by 2021. Following the example of the EFSF loans, both the grace period as well as the interest payments to the IMF could be deferred. The IMF was brought in by the Troika to ensure an objectively designed and robust programme. It should now share responsibility for its failings. Referring back to the November 2012 agreement, as has been done recently, is rather unconvincing. A shared programme should mean shared responsibility.

- Greece has repayment obligations to the ECB of some 27 billion euros over the next few years. The July payment especially cannot be done with market borrowing. Instead, a European Stability Mechanism (ESM) programme appears indispensable in order to replace the ECB as a creditor.

- If GDP growth remains below expectations, the option of swapping current loans to GDP-indexed loans could also be discussed, so as to provide insurance against unexpected negative shocks to GDP.

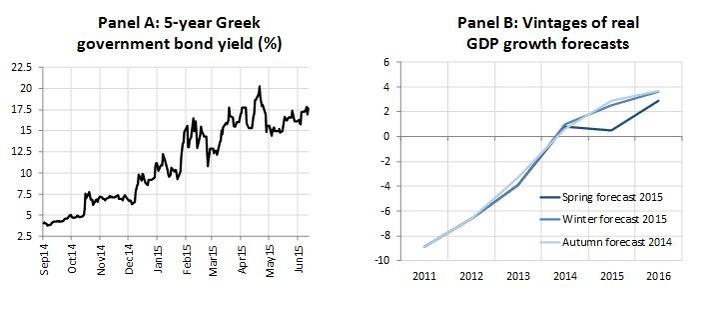

The third and most important issue concerns confidence and trust. Perhaps the biggest lesson of the recent turmoil is that an economy cannot grow if there is no confidence in that economy. Since the Syriza government came to power and started confrontational negotiations for a new debt deal, a dramatic decline in confidence has occured. In particular, sovereign yields have increased significantly over recent months. At the same time, the European Commission has revised its real GDP growth forecastsdownwards – despite a substantial reduction in austerity and the neutral fiscal stance implemented by Syriza. Without being hard evidence, this suggests that a country like Greece needs confidence above all. Confidence is a result of political action and building trust with European partners.

Sources: Panel A: EC country forecasts; Panel B: Datastream Thomson-Reuters

Structural reforms are an important building block in the re-establishment of trust and improving growth prospects (the OECD has identified more than 320 competition-distorting rules and provisions in the Greek service and product markets). IMF research finds that structural reforms can have positive and statistically significant effects on total factor productivity. The OECD concurs: countries with good institutions, low corruption, adequate levels of competition and better education systems typically perform better than countries without such features (seeOECD report on inclusive growth).

How realistic is it to call for such things? The track-record of imposing reforms from the outside in IMF programmes is rather mixed. Yet, being in a monetary union is not the same as a simple IMF programme in Latin America. Greece – like all countries of the union – agreed to share sovereignty on economic policies when it signed the Lisbon treaty (Article 121). Granting tax relief to the richest 6000 people, while asking for debt relief from the European creditors was certainly a hostile act. Refusing to reform pensions and introducing early retirement schemes when the pension system is unsustainable, while asking for debt relief, amounts to asking others to pay for Greek pensions. Slowing down the ongoing institutional transformation (that my colleague Zsolt Darvas has shown to be substantial) as the Syriza government seems to be doing, is not acceptable in a monetary union based on shared sovereignty.

To sum up, both sides still have some mileage to go. A sensible deal would consist of

- lower primary surplus targets, perhaps as little as 0.75% this year and 1.25% next year and a medium term primary surplus of 2.5%

- a delay in the debt repayment schedule to the IMF, but no further additional debt relief. Commitment to debt relief is growth severely disappoints.

- implementing concrete steps towards a further institutional transformation of Greece that is suitable in re-establishing trust, confidence and above all market access.Growth prospects are not so bad if good policies and confidence return.

It is in the interests of both Greece and its creditors to find a comprehensive agreement. Such an agreement requires Greece to implement strong reforms and return to a collaborative political approach, which is essential in a monetary union based on shared sovereignty. It requires the creditors to be less demanding on fiscal austerity in the next years. The euro area can avoid default and exit, but only if collaboration and trust are re-established.

I thank Pia Hüttl for excellent research assistance and Zsolt Darvas and Silvia Merler for comments.

Read more:

A shorter version of this piece was also published in Expansión.

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

ΕΥΡΩΕΚΛΟΓΕΣ ΚΑΙ ΤΟ ΜΕΛΛΟΝ ΤΗΣ ΕΥΡΩΠΗΣ

Είναι γεγονός ότι οι τωρινές εκλογές λόγω της ανάπτυξης των κομμάτων του λαϊκισμού είναι κάπως διαφορετικές από τις προηγούμενες. Αλλά πιστεύω ότι όλε

After the ESM programme: Options for Greek bank restructuring

With the end of the Greece support programme, authorities now have scope to focus on the legacy of NPLs and excess private-sector debt. Two wide-rangi

A new statistical system for the European Union

Quality statistics are essential to economic policy. In this essay, Andreas Georgiou demonstrates the existence of fundamental risks inherent in the E