ECB Quantitative Easing on track

On 9 March 2015 the ECB began purchasing European sovereign and agency bonds and supranational debt securities under the Public Sector Purchase Progra

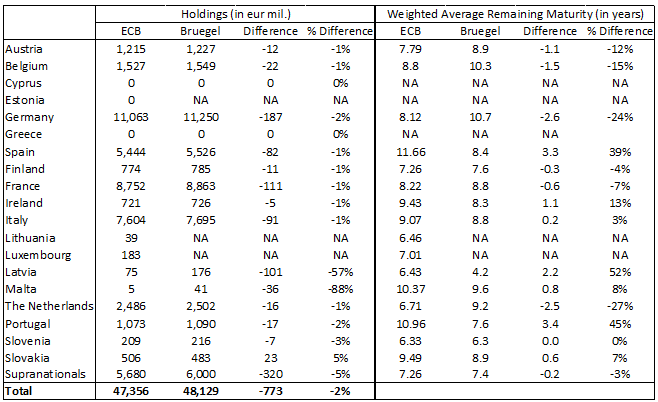

On 9 March 2015 the ECB began purchasing European sovereign and agency bonds and supranational debt securities under the Public Sector Purchase Programme (PSPP). In our policy contribution published on 11 March 2015, we explained that the ECB would purchase sovereign debt according to the capital keys and according to the maturity distribution of outstanding debt while taking into consideration the self-imposed 2-30 year remaining maturity range and the 25% and 33% issue and issuer limits. Today, the ECB published its PSPP holdings and the corresponding weighted average remaining maturities for each member state and the supranational institutions after the first month of purchases. The table below compares our calculations with the actual purchases.

Note: We did not provide values for Estonia, Luxembourg and Lithuania because their debt level is so small and data is scarce.

For the time being, the Eurosystem is perfectly on track with its commitments in terms of total volume of sovereign bonds purchased and also in terms of country allocation. Indeed, its actual purchases are roughly in line with our previous calculations. During the first month of the programme, the Eurosystem purchased €41.7 billion in sovereign debt instead of the expected €42.6 billion (i.e. €44 billon minus what should be allocated to Greece and Cyprus as they are not currently eligible for the reasons detailed in our policy contribution). The only notable difference with our predictions comes from Latvia and Malta for which it purchased much less debt than what we expected. This could be due to the small size of the markets or maybe because it anticipated that the 25% issuer limit will be reached quickly, and therefore chose to space the purchases out over the length of the program.

In terms of the maturity structure of the purchases, the weighted average maturities published today correspond only very broadly to our estimates, which were calculated from the actual maturity distribution of each country’s outstanding 2-30 year debt before QE started, thus ensuring market neutrality of the purchases. For instance, significant differences can be noted for Germany, Spain, Portugal and the Netherlands. Interestingly, in Germany, the average maturity of the bonds purchased is shorter than the one of the overall observed distribution, despite negative rates on the shorter end of the yield curve. However, the weighted average maturities of the purchases are both above and below our estimates depending on the countries. It is therefore difficult to conclude yet that these discrepancies indicate that the Eurosystem significantly and purposefully deviates from purchasing according to the current outstanding distribution. Indeed, the ECB itself notes that "deviations could reflect (...) the issue share limits taking into account holdings in other Eurosystem portfolios as well as the availability and liquidity conditions in the market during the implementation period"

About the authors

Related content

Inflation inequality in the European Union and its drivers

What will it cost the European Union to pay its economic recovery debt?

Servicing the EU debt until 2058 seems feasible, despite increased borrowing costs, but member countries must make choices about budget funding

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.