The Greek banking system: a tragedy in the making?

As the ECB has decided to discontinue allowing Greek government bonds to be used as collateral in normal ECB refinancing operations, attention is fully back on the Greek banking system.[1] One can criticize the ECB’s decision for aggravating the crisis but one can also argue that the ECB had no choice but to act as it did given the self-proclaimed insolvency of the Greek state.

In any case, this decision raises the question about how the Greek banking system looks at this point in time. Furthermore, it raises the question as to whether the new single supervisor, the ECB’s SSM, needs to act and ask banks to raise new capital, or whether this is purely a liquidity crisis.

Supposedly, the reference by the new finance minister Varoufakis is to the quality of sovereign debt and sovereign guarantees. The correct response to this is moving the liquidity provisioning against government papers to the Central Bank of Greece with ELA (Emergency Liquidity Assistance) operations. A more fundamental question is about the solvency of Greek banks and what conclusions the SSM should be drawing.

In this blog, we aim to provide an overview of the state of the Greek banking system. We focus on the four largest Greek banks that are directly supervised by the ECB. Their assets represent 88 percent of the Greek banking system or €346.4 billion. The book value of the four banks taken together amounts to 35.0 billion in 2014Q3, the latest date for which SNL provides the respective balance sheet data. From the end of 2013 (the time of the Asset Quality Review, AQR) to 2014Q3, the four banks increased their equity by 5.7 billion, up from 29.3 billion.

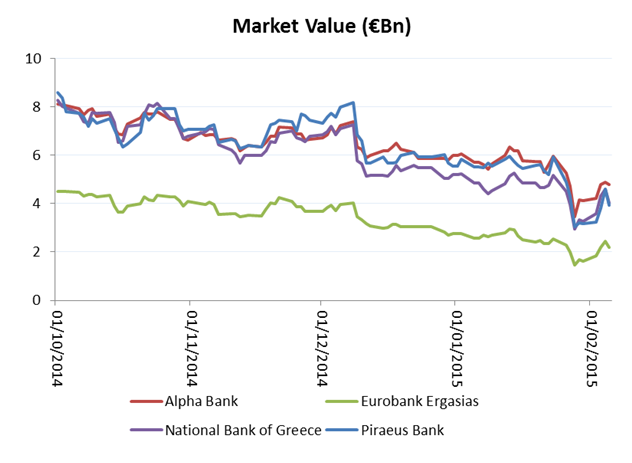

The market value of the four major banks has since plummeted: The chart below shows that in the last week especially, after the election, the market value has literally collapsed and it is now 15.2 billion or only 43 percent of the book value of 2014Q3.

Source: Thomson Reuters Datastream, most recent data 05/02/2015

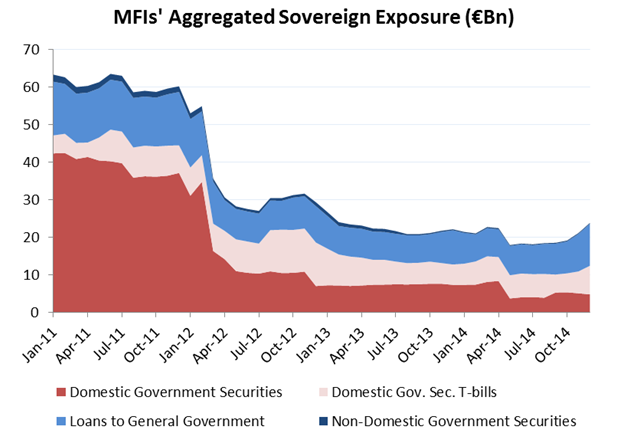

So what do we know about the underlying health of the major Greek banks and the risks on their balance sheets? For obvious reasons, the sovereign exposure has received a lot of attention recently, for example by Karl Whelan.

Below we show the total holdings of sovereign debt in the Greek banking system. The current total exposure amounts to 13.1 billion, 94 percent (12.4 billion) of these holdings are domestic. Breaking this down further, 7.6 billion is in domestic T-bills. Finally, loans from the Greek banking sector to the General Government sector amount to 11.2 billion in December 2014.

Note: Aggregated Balance Sheet of Monetary Financial Institutions (MFIs) excluding Bank of Greece (BoG). Aggregated MFI balance sheet, European Central Bank, Securities excluding shares and derivatives, General Government

Sources: Bank of Greece, ECB, Bruegel calculations

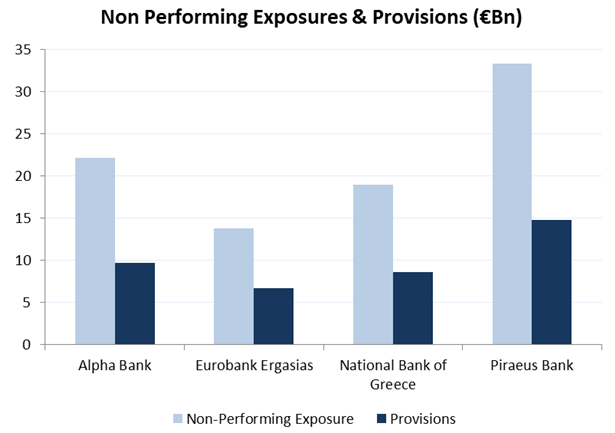

Furthermore, the recent comprehensive assessment and stress test by the ECB provide detailed information on the non-performing exposure (NPE) of the four banks. The chart below shows the NPEs in billions of euros and the provisioning that has been made to cover for these exposures.

Note: graph shows total non-performing exposure and the amount for provision for it.

Source: European Central Bank, End of 2013, Bruegel calculations

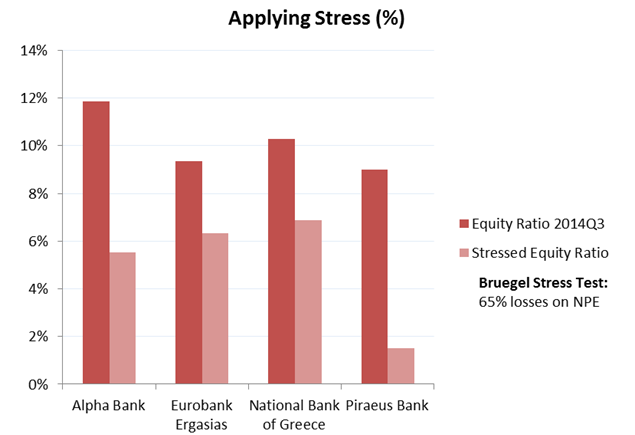

What does this graph tell us about the vulnerability of the banks to stress? Obviously, the greater the economic shock resulting from the current stress and the greater the fall in GDP, the more non-performing loans could end up in the books of the banks in Greece. At the same time, the loss on the existing non-performing exposures could increase. To get a sense of the potential risks, we performed a very simple stress test on the existing and reported NPEs. This is not necessarily our prediction of what will happen but it does give a sense of potential vulnerability to macroeconomic stress. Our stress test is based on a simple, and arguably large loss of 65 percent on NPEs. From this, we derive an implied loss beyond what has been provisioned for already.

The result is depicted in the chart below. It indicates that the existing book equity would be significantly reduced in all four banks. Interestingly, the resulting book value if those hypothetical book losses were realised would be relatively close to the current market value of these four banks – hypothetical capital after stress of 17.8 billion compared to 15.2 billion market valuation at present.

Note: This chart is calculated by subtracting 65 percent of NPEs, less provisions, from Equity. We make the simplifying assumption that provisions are fungible across loan types. A given Euro of provision is assumed to be able to cover NPE on any type of loan granted. Furthermore, we are taking the NPE rates as of 2013Q4 and applying them to Equity as of 2014Q3. NPEs are calculated as a percentage of Total Assets, not Risk Weighted Assets as used in the typical AQR results. NPEs may have deteriorated further, and in reality provisioning may not be so flexible.

Source: SNL Financial, European Central Bank, Bruegel calculations

Overall, our graphs show that the Greek banking system is currently under severe stress following the market turbulences caused by political uncertainty. If these turbulences lead to additional declines in GDP, higher losses on non-performing loans and further increases in non-performing loans due to a contraction of GDP, the capital base of the Greek banking system could be severely affected. This highlights how important it is to quickly come to a cooperative solution ending financial and macroeconomic stress.

[1] The European Central Bank’s Governing Council has lifted the waiver of minimum credit rating requirements for Greek government bonds which, until yesterday, had allowed banks to use them in normal ECB refinancing operations despite the fact that they did not fulfil minimum credit rating requirements.

Data sources: Bank of Greece and ECB

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

After the ESM programme: Options for Greek bank restructuring

With the end of the Greece support programme, authorities now have scope to focus on the legacy of NPLs and excess private-sector debt. Two wide-rangi

ΕΥΡΩΕΚΛΟΓΕΣ ΚΑΙ ΤΟ ΜΕΛΛΟΝ ΤΗΣ ΕΥΡΩΠΗΣ

Είναι γεγονός ότι οι τωρινές εκλογές λόγω της ανάπτυξης των κομμάτων του λαϊκισμού είναι κάπως διαφορετικές από τις προηγούμενες. Αλλά πιστεύω ότι όλε

A new statistical system for the European Union

Quality statistics are essential to economic policy. In this essay, Andreas Georgiou demonstrates the existence of fundamental risks inherent in the E