Blogs review: The new proposed IMF lending framework

If introduced, the new framework would most likely eliminate the systemic risk waiver, which allowed the Fund to lend large amounts to countries whose

What’s at stake: As many authors worry about the consequences of the peculiar interpretation of the pari passu clause in the Argentina saga, a relatively unnoticed proposal, which was discussed on June 13 2014 by the Executive Board of the IMF to reform its lending framework, could also have large implications in the context of sovereign debt vulnerabilities. If introduced, the new framework would most likely eliminate the systemic risk waiver, which allowed the Fund to lend large amounts to countries whose debt didn’t qualify as sustainable with high probability and would instead introduce the possibility of maturity extensions as a policy tool.

The need for a new system

Joseph Stiglitz writes that in the 1980s, when sovereign debts were mainly held by banks, restructurings could be done relatively smoothly. But with the growth of capital markets, these matters have become more difficult, as we have repeatedly witnessed. And with the growth of credit-default swaps and derivatives, they have become still worse. The experience of the recent eurozone crisis stands in sharp contrast to the Latin American debt crisis in the 1980s, when banks were not allowed to exit precipitously from their loans.

Kenneth Rogoff writes that Argentina’s latest debt trauma shows that the global system for sovereign-debt workouts remains badly in need of repair. With emerging-market growth slowing, and external debt rising, new legal interpretations that make debt future write-downs and reschedulings more difficult do not augur well for global financial stability. Back in 2003, partly in response to the 2001 Argentine crisis, the IMF proposed a new framework for adjudicating sovereign debts. But the proposal faced sharp opposition not only from creditors who feared that the IMF would be too friendly to problem debtors, but also from emerging markets that foresaw no near-term risk to their perceived creditworthiness. The healthy borrowers worried that creditors would demand higher rates if the penalties for default softened.

The 2002 Exceptional Access Framework and its 2010 reform

The IMF writes that prior to 2002, the exceptional access policy was designed to be very flexible—and was implemented that way. In circumstances where a member sought financing in excess of the established limits, the Fund had a policy of waiving the limits on the basis of “exceptional circumstances”—with no criteria as to what these circumstances were and why they should be considered particularly exceptional. The Fund found itself invoking the exceptional access policy with greater frequency as capital account crises arrived with greater frequency during the 1990s. The Fund’s decision to lend to Argentina in 2001, and the subsequent default of the country’s debt, served as the final catalyst for a broad review of the Fund’s exceptional access policy. This review culminated in the 2002 reform.

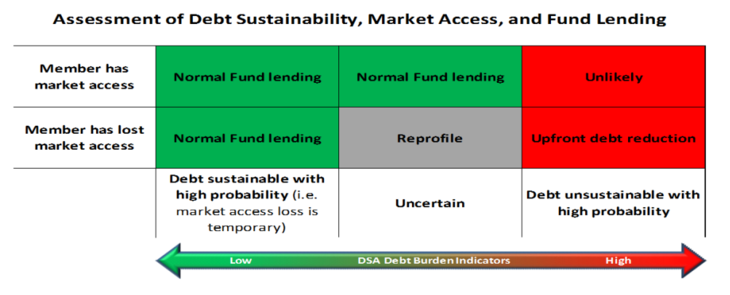

The IMF writes that under the “2002 framework” (the Exceptional Access Framework) the Fund may provide large scale financing without the need for a debt restructuring if the Fund determines that the member’s debt is sustainable with high probability. The problem with that approach came to the fore during the Fund’s experience with the euro area programs. While the DSAs produced did not conclude that debt was unsustainable, they were also not able to conclude that the debt was sustainable with a high probability. Under the terms of the 2002 policy, the only choice for the Fund would have been to condition Fund support on the implementation of a debt restructuring operation that was of sufficient depth to enable the Fund to conclude that, post restructuring, the member’s indebtedness would be sustainable with high probability. Out of concern that an upfront debt restructuring operation would have potentially systemic effects, the Fund opted to amend the framework in 2010 to allow the requirement of determining debt sustainability with “high probability” to be waived in circumstances where there is a “high risk of international systemic spillovers.”

Brett House writes that many IMF member countries have argued, however, that this change was both ad hoc and unfair: ad hoc because a major policy change was made in the same meeting that approved a loan; unfair because small countries outside a rich economic club such as the euro zone will never qualify for this special treatment.

Reprofiling instead of restructuring

Brett House writes that the IMF is considering a big shift in its lending rules. Eager to avoid a repeat of the massive loans it provided to the hopeless case that was Greece in 2010 – and Argentina in 2003 – the Fund has just released a staff paper that proposes major changes in its policy framework. The paper argues that the Fund should explicitly recognize that some sovereign crises fall in a messy middle—neither clear-cut insolvency, nor a temporary balance-of-payments problem. This gray zone calls for a new approach to crisis management. Rather than stretching credibility by certifying such cases as sustainable with “high probability,” or invoking the systemic exemption the proposed new policy would allow the Fund to lend in situations where the outcomes look less certain. Creditors would be asked to defer or “reprofile” their debt-service payments for a number of years.

Miranda Xafa writes that the IMF now proposes eliminating the systemic exemption and replacing it with a new framework that would make IMF support conditional on a debt “re-profiling” operation in exceptional access arrangements, in cases where the country has lost market access and there is uncertainty regarding debt sustainability, in order to avoid using Fund resources to bail out private creditors in such cases. Specifically, when these conditions are met, the IMF proposes maturity extensions of privately held debt for around three years through a voluntary debt operation, as a condition for providing exceptional access to IMF resources.

Source: IMF

The IMF writes that this would introduce greater flexibility into the 2002 framework by providing the Fund with a broader range of potential policy responses. Specifically, in circumstances where a member has lost market access and debt is considered sustainable, but not with high probability, the Fund would be able to provide exceptional access on the basis of a debt operation that involves an extension of maturities (normally without any reduction of principal or interest).

With the introduction of reprofiling as an additional tool, if the Board so decides, several Executive Directors favored removing the systemic exemption to the exceptional access framework, which had raised concerns about inequity and moral hazard associated with a large scale bail-out. Some others preferred to retain the systemic exemption, which in their view is a pragmatic way to safeguard financial stability in an increasingly integrated world and to avoid the perception of lack of evenhandedness. A few Directors focused noted that there could be operational difficulty in judging if both conditions for reprofiling have been met and the risk that the reprofiling expectation could trigger market volatility.