The limits of a purely intra-euro rebalancing strategy

The need to rebalance the debts of several Eurozone members is a major root of the current crisis. This column argues that a purely intra-euro reb

The need to rebalance the debts of several Eurozone members is a major root of the current crisis. This column argues that a purely intra-euro rebalancing strategy has its limits and that a weaker euro would help. It urges the European Central Bank to adopt looser monetary policy, which is anyway justified in a highly recessionary environment.

The perceived failure of Greece, Portugal, and Spain to achieve sustainable external positions and economic growth inside the Eurozone is a major factor behind the current crisis. Their trade deficits should be turned to sizeable surpluses in which real exchange rate developments should play a role. Some adjustments, both in trade balances and real exchange rates, have already taken place in the past few years. Is the remaining adjustment a purely intra-Eurozone issue or does the external value of the euro play a role?

Calls for a weaker euro

Some authors have already called for a weaker euro. For example, Charles Wyplosz (2012) concluded that since both monetary and fiscal policies are constrained in the Eurozone, the only possibility to stop the economic recession is a rise in exports, which should be helped by a weaker euro. Bernard Delbecque (2012) similarly called for a weaker euro to boost economic growth, and also to achieve higher inflation in order to allow for larger inflation differentials between surplus countries (especially Germany) and deficit countries (especially Spain).

However, the case for a weaker euro may not be that straightforward for three reasons:

- First, Eurozone members had a close to balanced aggregate current-account position, while before the crisis e.g. Germany’s intra-euro real exchange rate has depreciated significantly and the German current account turned to a sizeable surplus. The opposite happened in Spain. This may suggest that a reversal of these pre-crisis intra-euro trends could correct intra-euro current-account imbalances without resorting to a weaker euro.

- Second, the ECB’s single mandate is price stability and therefore it cannot allow higher aggregate Eurozone inflation.

- And third, monetary easing by the European Central Bank (ECB) to weaken the euro may be seen a ‘beggar-thy-neighbour’ policy and may push the Eurozone into a sizeable current account surplus, which would be difficult to absorb by the rest of the world.

The limits of intra-euro rebalancing

Focusing on the first issue highlighted above, in a recent paper (Darvas 2012b), I assess the potential of intra-euro rebalancing and concluded that it has limits, for six reasons.

- First, the share of intra-euro trade is not high and even declined during the first decade of the euro. For example, in 2011 the share of the initial 12 Eurozone members in German exports was 38% and 43% in German imports. The same figures for Spain are 53% and 47%, respectively, and for Greece 29% and 41%, respectively.

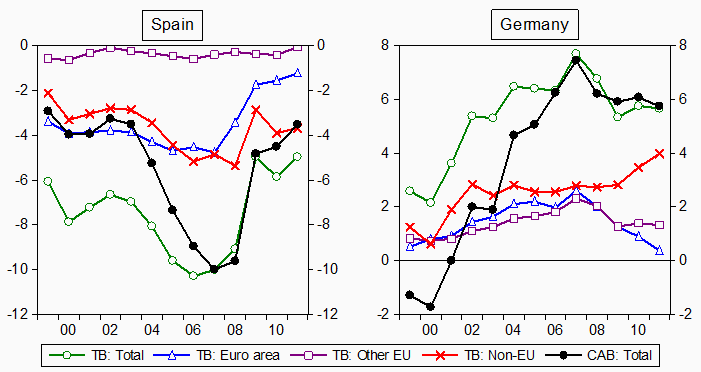

- Second, intra-euro trade balances of goods have already adjusted to a great extent. Figure 1 shows that Spain’s deficit and Germany’s surplus with the rest of the Eurozone have declined substantially toward zero. Yet Spain’s overall trade deficit remained sizeable, about 5% of GDP. It is also interesting to observe that Germany was able to increase its surplus with non-EU countries, partly compensating for the reduction of the surplus with EU countries. As a consequence, in 2011, 70% of the German trade surplus came from extra-EU trade, 23% from non-euro EU members, and less than 7% from Eurozone members.

Figure 1. Trade balance of goods with different regions, and the current account balance (% GDP), 1999-2011

Note: TB = trade balance of goods; CAB = current account balance. Source: author’s calculation using Eurostat’s External Trade database; see Darvas (2012b) for details.

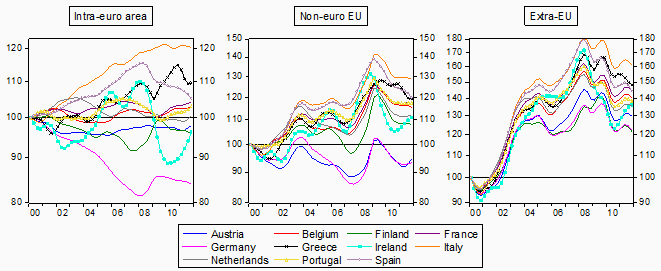

- Third, the intra-euro real effective exchange rates (REERs) of the three southern euro members whose external sustainability is at risk (Greece, Portugal, and Spain) have also either already adjusted or do not indicate significant appreciations since 2000. The left panel of Figure 2 shows that Spain’s intra-euro REER has almost corrected the pre-crisis increase; the increase was not at all high in Portugal (3% cumulative increase from 2000Q1 to 2011Q4); and we also cannot say that Greece’s REER has overly appreciated compared to the rest of the Eurozone (10% cumulative increase form 2000Q1 to 2011Q4). But the middle and right hand panels of Figure 2 show that the non-euro EU and the extra-EU REERs are still much higher than in 2000, even though some depreciation, fuelled by the depreciation of the euro, can be observed in all countries during the past few years.1

Figure 2. Unit labour cost (ULC) based real effective exchange rate (2000Q1=100), 2000Q1-2011Q4

Source: Darvas (2012a).

Note: Business sectors excluding agriculture, construction and real estate activities are considered, and the REERs were calculated with constant sectoral weights to minimise the compositional effect. Therefore, these indicators differ (somewhat) from the indicators available at Eurostat, which consider the whole economy (including the public sector) and do not control for the effects of sectoral changes in the economy. We show the Hodrick-Prescott filtered values calculated with smoothing parameter 1, a very low value, to get rid of the short term noise only.

- Fourth, by 2011 there were only two main current-account surplus countries, Germany and the Netherlands (apart from the small Luxembourg). Austria’s surplus fell below 2% of GDP, while Belgium and Finland recorded current-account deficits.

- Fifth, since the above points imply that the pool of external surpluses of northern Eurozone members and, in particular, their surpluses with southern Eurozone members, have diminished and intra-euro real exchange rates of Greece, Portugal, and Spain are not that high, a purely intra-euro rebalancing strategy would require an ‘overcompensation’ from the German and Dutch side so that, for example, the intra-euro trade surplus of Spain is to compensate for her extra-euro trade deficit.2 But much faster German and Dutch wage and price increases would be resisted. Also, as Wolff (2012) lucidly argued, if the ECB keeps the 2% inflation target and price developments sooner or later follow wage developments, then the much faster wage increases in northern Europe would require an ever more significant wage deflation in southern Europe, which does not seem to be feasible given the downward wage rigidity observed in high-unemployment countries (Darvas 2012a).

- And sixth, the close-to-balanced aggregate current-account position of the Eurozone does not necessarily imply that the euro was in an equilibrium position. Available estimates suggest that the euro was significantly overvalued before the crisis. Due to intra-euro divergences in real exchange rates and the other determinants of the current account, before the crisis there were a significant transition from a current-account deficit to a surplus in Austria and Germany, an increased surplus in the Netherlands, a broadly stable surplus in Luxembourg, while in the other eight of the initial 12 Eurozone members the current-account balance has gradually deteriorated.

What to do?

Intra-euro rebalancing through unit labour cost (ULC) declines in southern Europe and ULC increases in northern Europe should continue, but it has limits. Merler and Pisani-Ferry (2012) demonstrate that the REER adjustment of the southern members would be facilitated by a reduced pace of fiscal adjustment in the northern members of the Eurozone, which unfortunately is not on the agenda. Structural reforms to make wages more responsive to unemployment in southern Europe should also be pursued, but at best it will take a long time to take effect. A weaker euro is also needed to support the extra-euro trade of southern Eurozone members, which would also boost exports, growth, inflation and wage increases in Germany, thereby helping further intra-euro adjustment and the survival of the euro.

The ECB could and should play a role in weakening the euro. Yet on 6 September 2012 the Governing Council of the ECB will probably announce a new sovereign bond purchasing programme which could push up the euro. The ECB should therefore also consider supplementary policies to achieve a weaker euro by a more accommodative monetary policy stance, which in any case would be justified in a highly recessionary environment. More interest rate cuts, especially if accompanied by a commitment to keep the rates low for a longer period as the Federal Reserve announced, and quantitative easing should also be considered.

Further monetary easing by the ECB should not be viewed as a ‘beggar-thy-neighbour’ policy, since the ECB would do what other central banks, such the Federal Reserve, the Bank of England, and the Bank of Japan, have already done. True, a weaker euro would probably result in an external surplus. For example, a 4% of GDP Eurozone surplus would be about 0.8% of GDP of the rest of the world – a large number and would fall disproportionally on the main trading partners of the Eurozone, but may not be infeasible. The US, China, and other major players, which all have brighter economic outlooks than the Eurozone, should recognise that the euro was overvalued for several years in the second half of the 2000s. The best they can do to help the resolution of the Eurozone crisis is not to lend more money, but to allow the euro to become undervalued for some years. Helping the resolution of the Eurozone crisis is in their interests as well.

A version of this column was originally published in VOX

References

Darvas, Zsolt (2012a), “Compositional effects on productivity, labour cost and export adjustment”, Bruegel Policy Contribution 2011/11, June.

Darvas, Zsolt (2012b), “Intra-euro rebalancing is inevitable, but insufficient”, Bruegel Policy Contribution 2012/15, August.

Delbecque, Bernard (2012), “Saving the euro requires restoring Spain’s competitiveness”, VoxEU.org, 30 July.

Merler, Silvia and Jean Pisani-Ferry (2012), “The simple macroeconomics of North and South in EMU”, Bruegel Working Paper 2012/12.

Wolff, Guntram B (2012), “Arithmetic is absolute: euro area adjustment”, Bruegel Policy Contribution 2012/09, May.

Wyplosz, Charles (2012), “End of game? Don’t bet on it”, VoxEU.org, 25 July.

1 It is interesting to observe that the intra-euro real exchange rate of Germany has not adjusted much (Figure 2), while her intra-euro trade balance has adjusted (Figure 1). This can be the result of demand compression and the consequent forced reduction in imports in suffering southern European members, which effect may disappear once the economy has returned to normal (which unfortunately seems still to be far away in southern Europe). Therefore, more genuine improvements in the price and non-price dimension of competitiveness of southern European euro members are needed. While the impact of demand compression on imports depends on the product structure as well, which differs somewhat considering intra-euro and extra-euro imports, the different pattern of the Spanish trade deficit across the main geographical dimensions is striking.

2 There would be secondary effects of a purely intra-euro rebalancing strategy. e.g. fast wage increases in Germany and stable or even declining wages in Spain, would make Spain more competitive with respect to all trading partners, not just with Germany, and the Spanish position relative to Germany could improve in other markets too. But these effects can be small, and at best time consuming.

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

The EU needs a methodology for including reform impacts in fiscal trajectories

Such a methodology, and a governance mechanism for managing associated risks, must be in place before the new fiscal framework kickstarts in September

Real effective exchange rates for 178 countries: a new database

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries